Highlights

COVID-19 pandemic

- The appearance of the COVID-19 virus in China and its global expansion to a large number of countries, has caused the viral outbreak to be classified as a global pandemic by the World Health Organization since March 11, 2020. The global economy is being strongly affected by the pandemic, which is gradually affecting the economies of all the countries in which the BBVA Group is present, mainly due to confinement measures that restrict activity and a drop in confidence from consumers and businesses. Although the situation seems to have eased in many of the countries of East Asia and Europe, which have begun to revitalize their economies again, much of the American continent is still in a phase of viral expansion. The governments of the different countries in which the Group operates have adopted different measures that have conditioned the evolution of the first half of 2020 as explained later.

Results

- Growth in operating income of 7.6% in the first six months (up 19.2% at constant exchange rates) driven by the net trading income (NTI) and a significant reduction in operating expenses, as a result of containment plans and the lower expenses derived from the lockdown. The result of the above was a significant improvement in the efficiency ratio.

- Impairment on financial assets increased mainly due to the deterioration of the macroeconomic scenario, resulting mostly from the impacts of COVID-19.

- As a result of the valuation of the goodwill of its subsidiaries, the Group estimated that there was an impairment in the United States, which was recorded under the heading "Other results" of the consolidated income statement as of March 31, 2020. This impairment represented an impact of -€2,084m in the net attributable profit and is mainly due to the negative impact from the updating of the macroeconomic scenario affected by the COVID-19 pandemic. This impact does not affect the tangible net equity, capital, or liquidity of the BBVA Group.

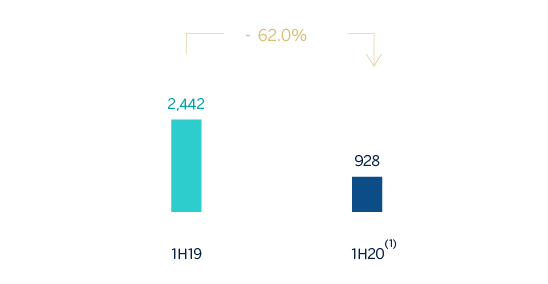

- Finally, the cumulative net attributable loss as of the close of June 2020 was -€1,157m. If the goodwill impairment in the United States is excluded from the year-on-year comparison, the Group's net attributable profit, compared to the same period of 2019, fell by 62.0% in the first half of 2020, to stand at €928m. In the second quarter of the year, net attributable profit, excluding the goodwill impairment in the United States, was €636m (up 118.0% quarter-on-quarter).

NET ATTRIBUTABLE PROFIT (MILLIONS OF EUROS)

(1) Excluding the goodwill impairment in the United States.

NET ATTRIBUTABLE PROFIT BREAKDOWN (1) (PERCENTAGE. 1H20)

(1) Excludes the Corporate Center.

Balance sheet and business activity

- The figure for loans and advances to customers (gross) was 1.5% higher compared to December 31, 2019, thanks to the government support programs to boost the financing of the real economy implemented in the different geographical areas.

- Customer funds grew by 2.2% in the half year, as a result of customers placing the larger liquidity provisions in the bank.

Liquidity

- The availability of substantial liquidity buffers in each of the geographical areas in which the BBVA Group operates and their management have allowed internal and regulatory ratios to be maintained well above the minimums required.

Solvency

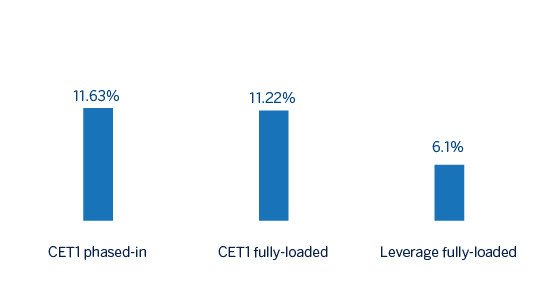

- The BBVA Group has set the objective to maintain a buffer on its fully-loaded CET1 ratio requirement (currently, at 8.59%) between 225 and 275 basis points. As of June 30, 2020, the CET1 fully-loaded ratio stood at 11.22%, in the upper part of the target management buffer.

CAPITAL AND LEVERAGE RATIOS AND COST OF RISK (Percentage as of 30-06-20)

Risk management

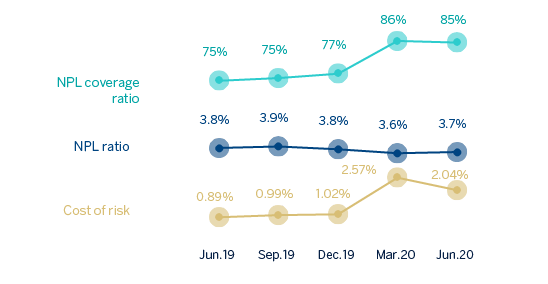

- The calculation of expected credit losses at the end of the first half of 2020 incorporates:

- The update of the forward looking information in the IFRS 9 models in order to reflect the circumstances created by the COVID-19 pandemic in the macroeconomic environment, which is characterized by a high degree of uncertainty regarding its intensity, duration and speed of recovery.

- The granting of relief measures in the form of temporary payment deferrals for customers affected by the pandemic, as well as the option to grant lending with a public guarantee facility.

NPL AND NPL COVERAGE RATIOS AND COST OF RISK (PERCENTAGE)

Purpose, values and strategy

BBVA's Purpose, to bring the age of opportunity to everyone, is more relevant than ever, as are our values: customer comes first, we think big and we are one team. This crisis has revealed the correct decision to opt for digitization, which has allowed the Bank to be closer to customers when they have needed it most, and reinforces our strategy. Therefore, our priorities remain unchanged; improve the financial health of customers, help them in the transition to a sustainable future, to grow in customers, seeking operational excellence and having the best and most committed team and the use of technology and data, will continue to be so the pillars on which the Group's strategy is based.

Security, business continuity and support measures taken by BBVA

From the outset, BBVA has adopted a series of measures to support its main stakeholders. The main business continuity measures taken are:

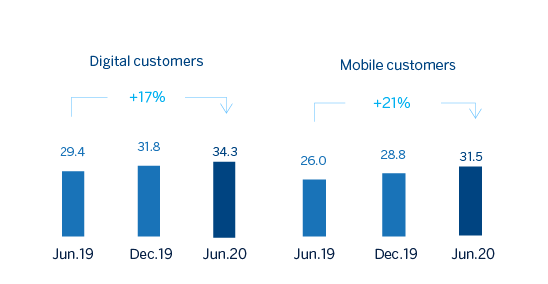

- In order to serve customers, and since financial services are legally considered an essential service in most of the countries in which the Group operates, the branch network remained operational, with dynamic management of the network and with information about branches and opening times on the website. In addition, the recommendation was for customers to operate through the digital channels and their remote agents, with the aim of minimizing the staff needed to serve customers in the branches, trying to reduce the risk of contagion and protect the health of its employees, customers and society in general. The data indicates that the COVID-19 crisis is accelerating digitization: At Group level, during the month of June 2020, digital sales (measured in units) rose sharply to 63.2% of the total, compared to 59.9% in February. Also at the end of June, BBVA's digital customers accounted for 60% of the total and customers operating with the bank through their cell phones accounted for 56% across the entire Group.

DIGITAL AND MOBILE CUSTOMERS (MILLIONS)

- With employees, the measures established by the health authorities have been implemented, including taking an early stance on promoting working from home. The priority in BBVA's return plan is the health and safety of its employees, their families and its customers, as well as ensuring business continuity, always following the recommendations of the health authorities. This return plan will be dynamic and adapted to the situation in each geographical area, and will be modulated on the basis of the data available at each moment on the evolution of the pandemic, the evolution of the business and the service to the customers.

Other support and responsibility measures taken are the following:

- The banks are a key part of the solution to the COVID-19 crisis. Specifically, BBVA has activated support initiatives with a focus on the most affected customers, regardless of whether they are companies, SMEs, self-employed workers or private individuals. The following are just some of those initiatives:

- In Spain, support for SMEs, the self-employed and companies through lines of credit and lines guaranteed by the ICO, advance payment of pensions and unemployment benefits to its customers, ICO-backed loans for rent payments, and the deferral of both insurance and credit card payments and grace periods on loans to affected individuals or companies;

- In the United States, flexibility in the repayment of loans for small business and for consumer finance, elimination of some fees and commissions for individual customers and the development of an online application that allowed companies benefiting from the Paycheck Protection Program (PPP) to apply for assistance just three days after the launch of the program;

- In Mexico, a repayment deferment on various credit products, fixed payment plan to reduce monthly credit card charges and suspension of Point of Sale (POS) fees to support retailers with lower turnover, as well as different support plans aimed at each situation for larger business customers;

- In Turkey, delay of loan repayments, interests and amortizations;

- In South America, some countries such as Argentina have given micro-SMEs and SMEs access to credit facilities to purchase teleworking equipment and funding facilities for the payment of salaries; Colombia has frozen the repayment of loans for individuals and companies for up to six months, and is offering a special working capital facility for companies; and in Peru, several measures were approved to support the SMEs and customers with consumer loans or credit cards.

- To support society in this fight against the COVID-19 pandemic, BBVA has donated €35m to purchase medical supplies, support vulnerable groups and promote research.

Pronouncements of regulatory bodies and supervisors

- With the aim of mitigating the impact of COVID-19, various European and international bodies have made pronouncements aimed at allowing greater flexibility in the implementation of the accounting and prudential frameworks. The BBVA Group has taken these pronouncements into consideration when preparing this report.

- With regard to the payment of dividends, on March 27 the European Central Bank recommended that, until at least October 1, 2020, credit institutions should refrain from distributing dividends or making irrevocable commitments to distribute them, and from repurchasing shares to remunerate shareholders. Consequently, the BBVA Board of Directors has agreed to amend, for the 2020 financial year, the Group's shareholder remuneration policy, which was announced by means of a material fact notification on February 1, 2017. The new policy for 2020 has been established as not making any dividend payments for the 2020 financial year until the uncertainties caused by COVID-19 disappear and, in any case, not before the end of the financial year.

- In terms of solvency, the European Parliament and the European Council adopted Regulation 2020/873 (known as the "CRR Quick Fix"), which amends both Regulation (EU) 575/2013 (Capital Requirement Regulation (CRR)) and Regulation 2019/876 (Capital Requirement Regulation 2 (CRR2)), which will apply from June 27, 2020. Its main impacts on the BBVA Group at the end of the first half involve the extension of the transitional treatment of IFRS 9 (only affects the phased-in ratios) and the bringing forward of the application of the SME and infrastructure support factor.