Risk management

Credit risk

The local authorities of the countries in which the Group operates initiated economic support measures in 2020, after the outbreak of the pandemic, including the granting of relief measures in terms of temporary payment deferrals for customers affected by the pandemic, as well as the granting of loans covered by public guarantees, especially to companies and SMEs.

These measures are supported by the rules issued by the authorities of the geographical areas where the Group operates as well by certain industry agreements and should help to ease the temporary liquidity needs of the customers. The classification of the customers’ credit quality and the calculation of the expected credit loss, once the credit quality of those customers have been reviewed under the new circumstances, will depend on the effectiveness of these relief measures. In any case, the incorporation of public guarantees is considered to be a mitigating factor in the estimation of the expected credit losses. The possibility of benefiting from this type of temporary deferral measures has expired in the main geographical areas where the Group is currently present.

Regarding the public guarantee programs, in Spain, following the publication of the RDL 5/2021 and the Code of Good Practices, to which BBVA has voluntarily adhered, term extensions could be requested until October 15, 2021, whereas in Peru, due to a new extension of the Plan Reactiva, it is allowed until December 31, 2021, as additional three months have been extended by the Royal Urgency Decree Nº 091-2021 of September 29.

For the purposes of classifying exposures based on their credit risk, the Group has maintained a rigorous application of IFRS 9 at the time of granting the moratoriums and has reinforced the procedures to monitor credit risk both during their validity and upon their maturity. In this respect, additional indicators have been introduced to identify the significant increase in risk that may have occurred in some operations or a set of them and, where appropriate, proceed to classify it in the corresponding risk stage.

Likewise, the indications provided by the European Banking Authority (EBA) have been taken into account, to not consider as refinancing the moratoriums that meet a series of requirements, without prejudice to keep the exposure classified in the corresponding risk stage or its consideration as refinancing if it was previously so classified.

In relation to the temporary payment deferrals for customers affected by the pandemic, since the beginning BBVA worked on an anticipation plan with the goal of mitigating as much as possible the impact of these measures in the Group, due to the high concentration of its maturities over time. As of September 30, 2021, the payment deferrals granted by the Group following EBA criteria amounted to €1,036m.

Calculation of expected losses due to credit risk

To respond to the circumstances generated by the COVID-19 pandemic in the macroeconomic environment, characterized by a high level of uncertainty regarding its intensity, duration and speed of recovery, forward-looking information has been updated in the IFRS 9 models to incorporate the best information available at the date of the publication of this report. The estimation of the expected losses has been calculated for the different geographical areas in which the Group operates, with the best information available for each of them, considering both the macroeconomic perspectives and the effects on specific portfolios, sectors or specific debtors. The scenarios used consider the various economic measures that have been announced by governments as well as monetary, supervisory and macroprudential authorities around the world. However, the final magnitude of the impact of this pandemic on the Group's business, financial situation and results, which could be material, will depend on future and uncertain events, including the intensity and persistence over time of the consequences derived from the pandemic in the different geographical areas in which the Group operates.

The expected losses calculated according to the methodology provided by the Group, including macroeconomic projections, have been supplemented with quantitative management adjustments in order to include issues that might imply a potential impairment which due to its nature is not included in the model and which will be assigned to specific operations in case this impairment materializes (e.g, sectors and collectives more affected by the crisis).

The classification of vulnerable activities to COVID-19 was established at the outbreak of the pandemic, in order to identify activities susceptible to further deterioration in the Group’s portfolio. Based on this classification, management measures were taken, with preventive rating adjustments and restrictive definition of risk appetite. Given the progress made during the course of the pandemic, which has led to the almost complete elimination of restrictions on mobility and the subsequent recovery from these restrictions, consideration is now being given to the specific characteristics of each client over and above their belonging to a particular sector. Therefore, maintaining this vulnerability classification is not considered necessary due to its low level of discrimination.

As of September 30, 2021, in order to incorporate those aspects not included in the impairment models, there are management adjustments to the expected losses amounting to €304m for the entire Group, €272m in Spain and €32m in Peru. As of June 30, 2021 this concept amounted to €348m in total, of which €315m were allocated to Spain and €32m to Peru. The variation in the quarter is therefore due to the use in Spain of €43m while the amount assigned to Peru remains unused.

BBVA Group's credit risk indicators

BBVA Group's main risk indicators have behaved as follows between January and September 2021, as a result, among other reasons, of the situation generated by the pandemic:

- Credit risk has increased by 0.4% (+0.4% at constant exchange rates). There was a slight increase at Group level in the quarter at constant rates, with Turkey leading growth along with Rest of Business. Spain recorded a slight decline while Mexico and South America remained practically flat, the latter with increases in almost all countries in the region. Compared to December, credit risk increased by 1.3% (+2.0% at constant exchange rates) with generalized growth except for Chile and Peru.

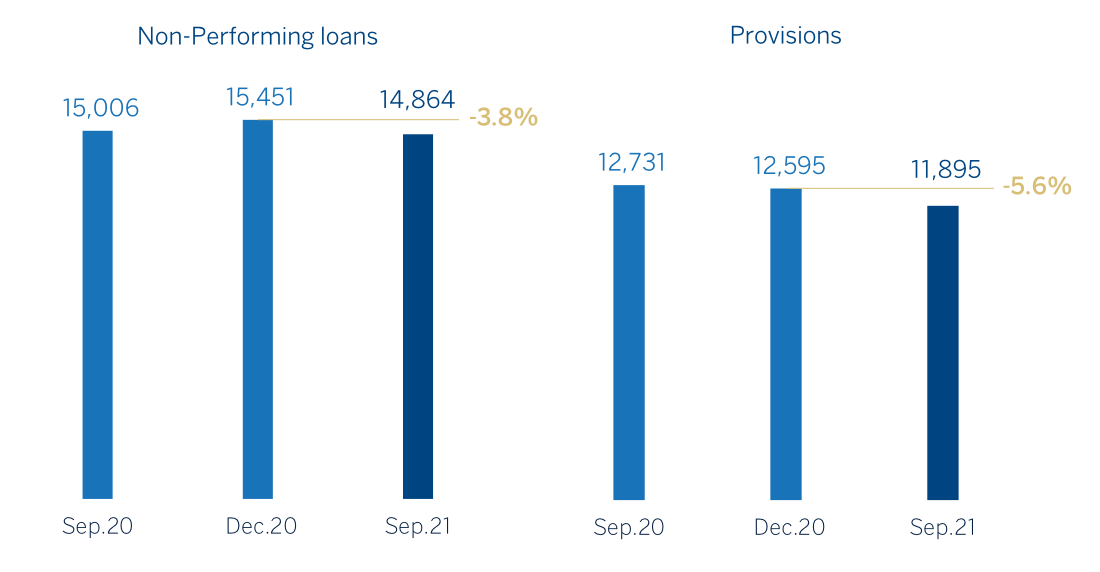

- The balance of non-performing loans decreased in the third quarter of the year (-5.2% both in current and constant terms) in the main geographical areas. Compared to the end of 2020, the balance decreased by 3.8% (-2.8% at constant exchange rates) overall due to the good performance of underlying flows, with controlled inflows and positive recoveries, in a more favorable economic environment than in previous quarters.

NON-PERFORMING LOANS(1) AND PROVISIONS(1) (MILLIONS OF EUROS)

(1) Excludes: BBVA USA and the rest of the Group's companies in the United States sold to PNC on June 1, 2021.

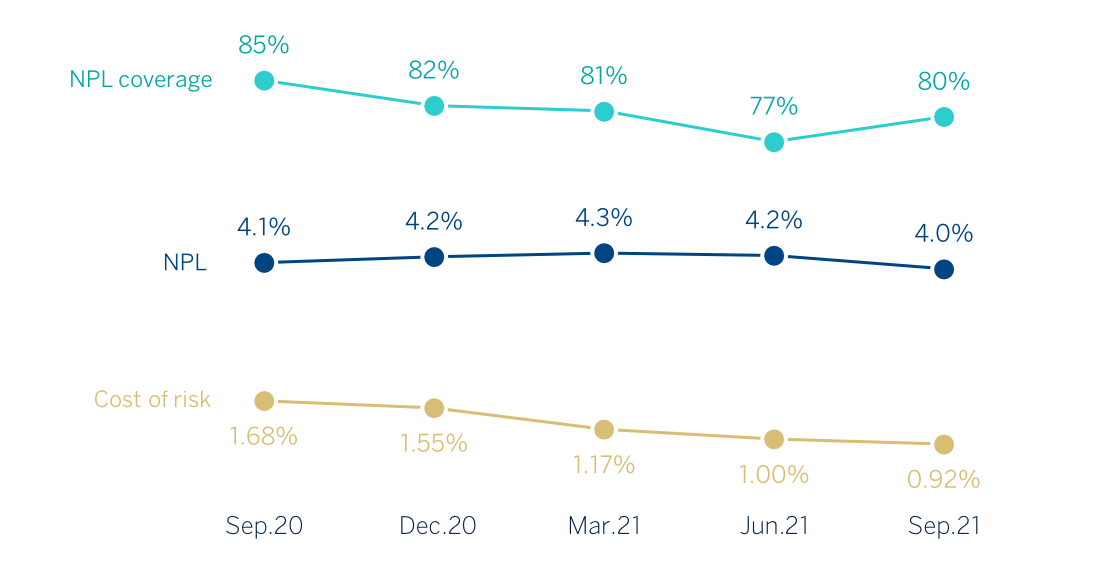

- The NPL ratio stood at 4.0% as of September 2021 (4.2% in June, 2021), 21 basis points below the figure recorded in December 2020.

- Loan-loss provisions decreased by 5.6% compared to December 2020 (-1.1% in the quarter) due to the positive evolution of the non-performing loans and an increase in write-offs during the year.

- The NPL coverage ratio amounted to 80%, -149 basis points compared to the end of 2020. Compared to the previous quarter, the NPL ratio improved by 327 basis points as a result of the aforementioned good performance of the nonperforming loans in the period.

- The cumulative cost of risk as of September 30, 2021 stood at 0.92% (-64 basis points below the end of 2020 and -9 basis points compared to June 2021). The loan-loss provisions carried out in the quarter were practically in line with those observed in the previous quarter, and were reflected in September in addition to the recurring flows of the month and the positive impact of the updated macroeconomic scenarios, partially mitigated by the effect of the annual recalibration on the Group’s provisioning models.

NPL(1) AND NPL COVERAGE(1) RATIOS AND COST OF RISK(1) (PERCENTAGE)

(1) Excluding BBVA USA and the rest of the Group's companies in the United States sold to PNC on June 1, 2021.

CREDIT RISK(1) (MILLIONS OF EUROS)

| 30-09-21 | 30-06-21 | 31-03-21 | 31-12-20 | 30-09-20 | |

|---|---|---|---|---|---|

| Credit risk | 371,708 | 370,348 | 365,292 | 366,883 | 365,127 |

| Non-performing loans | 14,864 | 15,676 | 15,613 | 15,451 | 15,006 |

| Provisions | 11,895 | 12,033 | 12,612 | 12,595 | 12,731 |

| NPL ratio (%) | 4.0 | 4.2 | 4.3 | 4.2 | 4.1 |

| NPL coverage ratio (%)(2) | 80 | 77 | 81 | 82 | 85 |

- General note: figures excluding BBVA USA and the rest of Group's companies in the United States sold to PNC on June 1, 2021, for the periods of 2021 and 2020, and the classification of BBVA Paraguay as non-current assets and liabilities held for sale for the periods of 2020.

- (1) Includes gross loans and advances to customers plus guarantees given.

- (2) The NPL coverage ratio includes the valuation adjustments for credit risk during the expected residual life of those financial instruments which have been acquired (mainly originated from the acquisition of Catalunya Banc, S.A.). Excluding these allowances, the NPL coverage ratio would stand at 78% as of September 30, 2021, 79% as of December 31, 2020 and 82% as of September 30, 2020.

NON-PERFORMING LOANS EVOLUTION (MILLIONS OF EUROS)

| 3Q21 (1) | 2Q21 | 1Q21 | 4Q20 | 3Q20 | |

|---|---|---|---|---|---|

| Beginning balance | 15,676 | 15,613 | 15,451 | 15,006 | 15,594 |

| Entries | 1,445 | 2,321 | 1,915 | 2,579 | 1,540 |

| Recoveries | (1,330) | (1,065) | (921) | (1,016) | (1,028) |

| Net variation | 115 | 1,256 | 994 | 1,563 | 512 |

| Write-offs | (848) | (1.138) | (796) | (1,149) | (510) |

| Exchange rate differences and other | (80) | (55) | (36) | 31 | (590) |

| Period-end balance | 14,864 | 15,676 | 15,613 | 15,451 | 15,006 |

| Memorandum item: | |||||

| Non-performing loans | 14,226 | 15,013 | 14,933 | 14,709 | 14,269 |

| Non performing guarantees given | 637 | 663 | 681 | 743 | 737 |

- General note: figures excluding BBVA USA and the rest of Group's companies in the United States included in the sale agreement signed with PNC as of 31-03-21 and the periods of 2020, and the classification of BBVA Paraguay as non-current assets and liabilities held for sale during the periods of 2020.

- (1) Preliminary data.

Structural risks

Liquidity and funding

Liquidity and funding management at BBVA aims to finance the recurring growth of the banking business at suitable maturities and costs, using a wide range of instruments that provide access to a large number of alternative sources of financing. In this context, it is important to notice that, given the nature of BBVA's business, the funding of lending activity is fundamentally carried out through the use of stable customer funds.

Due to its subsidiary-based management model, BBVA is one of the few major European banks that follows the Multiple Point of Entry (MPE) resolution strategy: the parent company sets the liquidity policies, but the subsidiaries are self-sufficient and responsible for managing their own liquidity and funding (taking deposits or accessing the market with their own rating), without fund transfers or financing occurring between either the parent company and the subsidiaries or between the different subsidiaries. This strategy limits the spread of a liquidity crisis among the Group's different areas, and ensures that the cost of liquidity and financing is correctly reflected in the price formation process.

In view of the initial uncertainty caused by the outbreak of COVID-19 in March 2020, the various different central banks provided a joint response through specific measures and programs, the extent of which, in some cases, has been extended until 2021 to facilitate the financing of the real economy and the provision of liquidity in the financial markets, increasing liquidity buffers in almost all geographical areas.

The BBVA Group maintains a solid liquidity position in every geographical area in which it operates, with liquidity ratios well above the minimum required:

- The BBVA Group's liquidity coverage ratio (LCR) remained comfortably above 100% throughout the first nine months of 2021, and stood at 170% as of September 30, 2021. For the calculation of this ratio, it is assumed that there is no transfer of liquidity among subsidiaries; i.e. no type of excess liquidity levels in foreign subsidiaries are considered in the calculation of the consolidated ratio. When considering these excess liquidity levels, the BBVA Group's LCR would stand at 209%.

- The net stable funding ratio (NSFR), defined as the ratio between the amount of stable funding available and the amount of stable funding required, demands banks to maintain a stable funding profile in relation to the composition of their assets and off-balance sheet activities. This ratio should be at least 100% at all times. The BBVA Group's NSFR ratio, calculated based on the criteria established in the Regulation (UE) 2019/876 of the European Parliament and the European Council, as of May 20, 2019; whose date of entry into force is June 2021, stood at 135% as of September 30, 2021.

The breakdown of these ratios in the main geographical areas in which the Group operates is shown below:

LCR AND NSFR RATIOS (PERCETANGE. 30-09-21)

| Eurozone (1) | Mexico | Turkey | South America | |

|---|---|---|---|---|

| LCR | 197 | 219 | 169 | All countries >100 |

| NSFR | 126 | 143 | 158 | All countries >100 |

- (1) Perimeter: Spain + the rest of the Eurozone where BBVA has presence.

One of the key elements in BBVA's Group liquidity and funding management is the maintenance of large high quality liquidity buffers in all business areas where the group operates. In this respect, the Group has maintained for the last 12 months an average volume of high quality liquid assets (HQLA) accounting to €143.5 billion, among which, 94% correspond to maximum quality assets (LCR Tier 1).

The most relevant aspects related to the main geographical areas are the following:

- In the Eurozone, BBVA has continued to maintain a sound position with a large high-quality liquidity buffer. During the first nine months of 2021, commercial activity has drawdown liquidity amounting to approximately €7 billion mainly explained by outflows during the first quarter of wholesale deposits that held very high balances at the end of December 2020. It should be noted that in the second quarter of 2021, the payment of the BBVA USA sale transaction was collected. In March 2021, BBVA S.A. took part in the TLTRO III liquidity window program to take advantage of the improved conditions announced by the European Central Bank (ECB) in December 2020, with an amount drawn of €3.5 billion, which when added together with the €34.9 billion available at the end of December 2020 it totaled €38.4 billion. In this regard, the ECB continues to support liquidity in the system through the measures it has implemented since the start of the pandemic, but it should be noted that it announced a slight slowdown in the pace of asset purchases under its PEPP program (Pandemic Emergency Purchase Programme) during the fourth quarter of 2021.

- In BBVA Mexico, commercial activity has provided liquidity between January and September 2021 in the amount of approximately 25 billion Mexican pesos, derived from a higher growth in customer funds compared with the increase in lending activity. This increased liquidity is expected to be reduced due to the recovery in lending activity, favored by the better growth trend in the country. This solid liquidity position is enabling an efficiency policy in the funding costs, in an environment of higher interest rates. Looking at wholesale issuances, a senior issue amounting to 3,500 million Mexican pesos was absorbed in September without needing to be refinanced, as it also happened with the subordinated issue amounting to USD 750m which was absorbed in March, 2021 and a senior issue amounting to 1,000 million Mexican pesos which was absorbed in April.

- The Central Bank of the Republic of Turkey (CBRT) lowered 100 basis points in September, leaving the benchmark rate at 18%, based on a reduction in core inflation. During the first nine months of 2021, the Bank's lending gap has widened in local currency, with a higher increase in loans than in deposits. Regarding foreign currency, both loans and deposits have decreased by a similar amount. Garanti BBVA continues to maintain a comfortable liquidity position.

- In South America, the liquidity situation remains adequate throughout the region, helped by the support of various central banks and governments which, in order to mitigate the impact of the COVID-19 crisis, have acted by implementing measures to stimulate economic activity and provide greater liquidity in financial systems. In Argentina, liquidity in the system continues to increase due to higher growth in deposits than in loans in local currency. A comfortable liquidity position has been maintained in Colombia following the adjustment for excess liquidity made in the last quarters. Despite a more stable political environment, Fitch downgraded the country's rating at the beginning of the quarter. BBVA Peru maintains solid levels of liquidity, despite the current uncertain environment, which has been reflected in a downgrading of Moody's rating. During the last quarter there has been an improvement in credit gap, especially in local currency.

The main transactions carried out in wholesale financing markets by the companies that form part of the BBVA Group during the first nine months of 2021 were:

- On September 1, 2021, BBVA S.A. issued a social preferred senior debt totaling €1 billion with a floating rate and a 2-year expiration date. This is the second issue made in 2021, following the issuance of senior preferred debt carried out in March, and is also the fifth issuance carried out by BBVA, meeting environmental, social and governance criteria (ESG). For more information on the transactions see the "Solvency" chapter in this report.

- In Turkey, there have been no issuances between January and September 2021. On June 2, BBVA Garanti renewed the 100% of a syndicated loan indexed to sustainability criteria, formed by two separate sections, amounting to USD 279m and €294m with a 1-year expiration date. Another €560m syndicated loan expires in November and is expected to be renewed.

- In South America, BBVA Uruguay issued the first sustainable bond on the Uruguayan financial market in February for USD 15m at an initial interest rate of 3.854%

Foreign exchange

Foreign exchange risk management of BBVA's long-term investments, principally stemming from its overseas franchises, aims to preserve the Group's capital adequacy ratio and ensure the stability of its income statement.

The U.S. dollar accumulated a 6.0% appreciation against the euro in the first nine months of 2021, thus reversing a large part of the depreciation which occurred last year. Among the emerging currencies, it is worth highlighting the good performance of the Mexican peso, which registered an appreciation of 2.8% against the euro since the end of 2020. The Turkish lira, which remained stable in the third quarter, accumulated a -11.5% depreciation against the euro in the first nine months of 2021. Political uncertainties have weighed down some South American currencies: Peruvian sol (-7.0%), Chilean peso (-6.2%) and Colombian peso (-5.1%). For its part, Argentine peso (-9.7%) continues with a moderate depreciation compared to previous years.

EXCHANGE RATES (EXPRESSED IN CURRENCY/EURO)

| Year-end exchange rates | Average exchange rates | ||||

|---|---|---|---|---|---|

30-09-21 |

∆% on 30-09-20 |

∆% on 31-12-20 |

Jan.-Sep.21 |

∆% on Jan.-Sep.20 |

|

| U.S. dollar | 1.1579 | 1.1 | 6.0 | 1.1961 | (6.0) |

| Mexican peso | 23.7439 | 10.3 | 2.8 | 24.0762 | 1.9 |

| Turkish lira | 10.2981 | (11.6) | (11.5) | 9.7098 | (21.8) |

| Peruvian sol | 4.7824 | (11.9) | (7.0) | 4.5826 | (15.1) |

| Argentine peso (1) | 114.29 | (22.0) | (9.7) | - | - |

| Chilean peso | 930.48 | (1.3) | (6.2) | 881.98 | 2.2 |

| Colombian peso | 4,440.18 | 2.3 | (5.1) | 4,424.44 | (5.8) |

- (1) According to IAS 29 "Financial information in hyperinflationary economies", the year-end exchange rate is used for the conversion of the Argentina income statement.

BBVA has maintained its policy of actively hedging its main investments in emerging markets, covering on average between 30% and 50% of annual earnings and around 70% of the CET1 capital ratio surplus. The closing of the sale of BBVA USA in June 2021 has modified the Group's CET1 fully-loaded ratio sensitivity to changes in the currencies. The most affected sensitivity by this change has been the U.S. dollar, which stands at around +18 basis points in the face of a 10% depreciation in the currency. The sensitivity of the Mexican peso is estimated at -5 basis points at the end of September 2021 and practically nil in the case of the Turkish lira, both currencies estimated against a depreciation of 10%. With regard to coverage levels of the expected results for 2021, these have remained stable this last quarter: 75% in Mexico and Turkey, and close to 100% in Peru and Colombia.

Interest rate

Interest rate risk management seeks to limit the impact that BBVA may suffer, both in terms of net interest income (short-term) and economic value (long-term), from adverse movements in the interest rate curves in the various currencies in which the Group operates. BBVA carries out this work through an internal procedure, pursuant to the guidelines established by the European Banking Authority (EBA), in order to analyze the potential impact that could derive from a range of scenarios on the Group's different balance sheets.

The model is based on assumptions intended to realistically mimic the behavior of the balance sheet. Of particular relevance are assumptions regarding the behavior of accounts with no explicit maturity and prepayment estimates. These assumptions are reviewed and adapted at least once a year to take into account any changes in behavior.

At the aggregate level, BBVA continues to maintain a moderate risk profile, in accordance with the established objective, showing positive sensitivity toward interest rate increases in the net interest income. The effective management of structural balance sheet risk has allowed it to mitigate the negative impact of the downward trend in interest rates and the volatility experienced as a result of the effects of COVID-19, and is reflected in the soundness and recurrence of net interest income.

At the market level, during the third quarter of 2021, there have been limited movements in the United States and European bond yield curves, generating a "U" movement, with rises starting in August due to the messages of the beginning of a gradual decrease in the extraordinary measures of expansionary monetary policy by both central banks. With regard to the emerging world, more virulent moves in bond yield curves due to the contagion effect of the latest rises in the U.S. yield curves, inflationary pressures and the continuation of the rate hike cycle (with the exception of Turkey, which dropped 100 basis points at September meeting). All of the above has had a limited impact on the generation of net interest income for the different units.

By area, the main features are:

-

Spain has a balance sheet characterized by a high proportion of variable-rate loans (basically mortgages and corporate lending) and liabilities composed mainly of customer deposits. The ALCO portfolio acts as a management lever and hedging for the bank's balance sheet, mitigating its sensitivity to interest rate fluctuations. The balance sheet´s profile has remained stable during the year, showing an interest net income sensitivity to 100 basis points increases by the interest rates around 20%.

On the other hand, the ECB held the marginal deposit facility rate unchanged at -0.50% and maintained the extraordinary support programs created after the outbreak of the COVID-19 crisis. This has created stability in European benchmark interest rates (Euribor) throughout the first nine months of 2021. In this matter, customer spread keeps pressured by the low interest rates environment.

- Mexico continues to show a balance between fixed and variable interest rates balances. In terms of assets that are most sensitive to interest rate fluctuations, the commercial portfolio stands out, while consumer loans and mortgages are mostly at a fixed rate. The ALCO portfolio is used to neutralize the longer duration of customer deposits. Net interest income sensitivity continues to be limited, registering a positive impact against 100 basis points increases in the Mexican peso which is around 2%. The monetary policy rate stands at 4.75%, higher that at the end of 2020 (4.25%), after a 25 basis points reduction during the first quarter of 2021 and a 25 basis points increase in June, August and September meetings. Regarding the consumer spread, a slight increase compared to first nine months of 2021 is appreciated, a trend which should continue due to the high interest rates environment.

- In Turkey, the sensitivity of loans, which are mostly fixed-rate but with relatively short maturities, and the ALCO portfolio balance the sensitivity of deposits on the liability side. The interest rate risk is thus limited, both in Turkish lira and in foreign currencies. With regard to base rates, there was an increase of 200 basis points in the first quarter compared to the level seen in December 2020; during the second quarter the base rates remained unchanged and in the third quarter there was a reduction of 100 basis points. The customer spread in Turkish lira improved from June onwards, benefiting from the refinancing of loans at higher rates. It is expected that it will continue to improve in an environment of lower interest rates.

- In South America, the risk profile for interest rates remains low as most countries in the area have a fixed/variable composition and maturities that are very similar for assets and liabilities, with a low net interest income sensitivity. In addition, in balance sheets with several currencies, interest-rate risk is managed for each of the currencies, showing a very low level of risk. Regarding the base rates of the central banks in Peru and Colombia, a rising trend in rates has begun, with increases in the last quarter of 75 and 25 basis points, respectively. In the first nine moths of 2021 there has been little change in customer spreads, which are expected to improve in an environment of higher interest rates.

INTEREST RATES (PERCENTAGE)

| 30-09-21 | 30-06-21 | 31-03-21 | 31-12-20 | 30-09-20 | 30-06-20 | 30-03-20 | |

|---|---|---|---|---|---|---|---|

| Official ECB rate | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Euribor 3 months (1) | (0.55) | (0.54) | (0.54) | (0.54) | (0.49) | (0.38) | (0.42) |

| Euribor 1 year (1) | (0.49) | (0.48) | (0.49) | (0.50) | (0.41) | (0.15) | (0.27) |

| USA Federal rates | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 |

| TIIE (Mexico) | 4.75 | 4.25 | 4.00 | 4.25 | 4.25 | 5.00 | 6.50 |

| CBRT (Turkey) | 18.00 | 19.00 | 19.00 | 17.00 | 10.25 | 8.25 | 9.75 |

- (1) Calculated as the month average.