Other Non-financial Information Report

Law 11/2018 of December 28 came into effect at the end of 2018, modifying the Commercial Code, the revised text of the Capital Companies Law approved by Royal Legislative Decree 1/2010 of July 2, and Law 22/2015 of July 20 on Accounts Auditing, regarding non-financial information and diversity (hereinafter, Law 11/2018); the latter replaces Royal Decree Law 18/2017 of November 24, by which Directive 2014/95/EU of the European Parliament and of the Council was transposed into Spanish law, as regards disclosure of non-financial information and diversity information.

Pursuant to Law 11/2018, certain companies, such as BBVA, are required to prepare a non-financial statement. This must be included either in the management report or in a separate report for the same year that includes the same content and meets the all specified requirements, including, but not limited to: the information needed to understand the performance, results, and position of the Group, and the impact of its activity on environmental,social, respect for human rights, and the fight against corruption and bribery matters, as well as employee matters, and should include any measures taken to promote the principle of equal treatment and opportunities for women and men, non-discrimination and inclusion of people with disabilities and universal accessibility.

In this context, BBVA prepares the consolidated non-financial information report in the Group's Management Report, which is attached to the Consolidated Financial Statements for the 2018 fiscal year.

Calculation of the non-financial key performance indicators included (KPI) in this consolidated non-financial statement is performed using the GRI (Global Reporting Initiative) guide, an international reporting framework, and is covered in the new article 49.6.e) of the Commercial Code introduced by Law 11/2018.

In addition, for the preparation of the non-financial information contained in this Management Report, the Group has considered the Communication from the Commission of July 5, 2017 on Guidelines on non-financial reporting (methodology for reporting non-financial information, 2017/C 215/01).

The information included in the consolidated non-financial statement is verified by KPMG Asesores S.L., in its capacity as independent provider of verification services, in accordance with the new wording given by Law 11/2018 to article 49 of the Commercial Code.

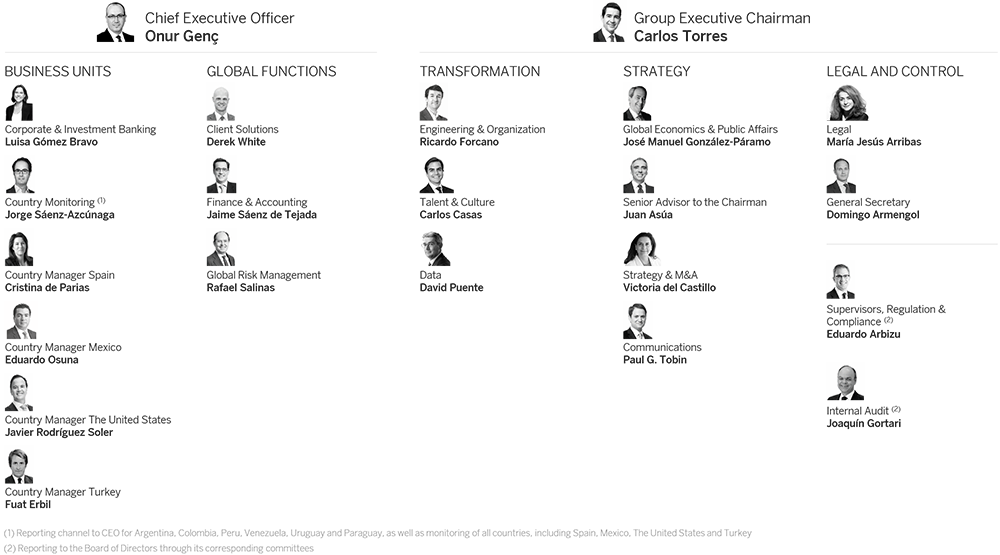

The Group’s organizational chart

At the end of 2018, the Board of Directors of BBVA approved a new organizational structure, aimed at fostering the Group’s transformation and businesses, while further specifying responsibilities for executive functions.

The main aspects of the new organizational structure are as follows:

- The Group Executive Chairman is responsible for the management and well-functioning of the Board of Directors, the supervision of the management of the Group, the institutional representation, and leading and boosting the Group’s strategy and its transformation process.

- The areas reporting directly to the executive chairman are those related to the transformation’s key levers: Engineering & Organization, Talent & Culture and Data; those related to the Group’s strategy: Global Economics & Public Affairs, Strategy & M&A, Communications and the new figure Senior Advisor to the Chairman; and the Legal-related and Board-related areas: Legal and General Secretary.

- The Chief Executive Officer (CEO) is in charge of the daily management of the Group’s businesses, reporting directly to BBVA’s Board of Directors.

- The areas reporting to the CEO are the Business Units in the different countries and Corporate & Investment Banking, as well as the following global functions: Client Solutions, Finance & Accounting, that integrates the functions of accounting and tax, and Global Risk Management.

Additionally, certain control areas strengthen their independence, establishing a direct reporting of their heads to the Board of Directors through the corresponding committees. These control areas are Internal Audit and the new Supervisors, Regulation & Compliance, area that is in charge of the relationship with regulators and supervisors, the monitoring and analysis of regulatory trends and the development of the Group’s regulatory agenda, and the management of compliance-related risks.

Environment

Macroeconomic environment

Global economic growth maintained robust throughout 2018 (approximately 3.6%), although it slowed more than expected in the second half of the year and the latest data on activity and confidence have generally given negative surprises. In particular, indicators linked to the industrial sector and international trade showed a clear deterioration, while those most closely linked to consumption and investment have resisted better. Poorer economic figures in Europe and China were accompanied by downwards trends in Asian countries and a certain cyclical deterioration in the United States that was new. The fear of a rapid global slowdown and the rise of protectionist risks also led to a sharp increase in the prices of refuge assets and capital outflows. Given this context of greater global uncertainty, and with inflation moderating as a result of lower oil prices, the main central banks, particularly the Federal Reserve (Fed), reacted with caution in their plans for normalization of monetary policy, which has been a key factor in the containment and partial reversal of tensions since the beginning of the year.

Global GDP growth and inflation in 2018 (Real percentage growth)

| GDP | Inflation | |

|---|---|---|

| World | 3.6 | 3.9 |

| Eurozone | 1.8 | 1.7 |

| Spain | 2.5 | 1.7 |

| The United States | 2.9 | 2.4 |

| Mexico | 2.2 | 4.9 |

| South America (1) | 1.3 | 8.4 |

| Turkey | 3.0 | 16.3 |

| China | 6.6 | 1.9 |

- Source: BBVA Research estimates.

- (1) It includes Argentina, Brasil, Chile, Colombia, Paraguay, Peru and Uruguay.

Digitalization and changing consumer behavior

Digital activity is outpacing growth in overall economic activity. Society is changing in line with the exponential growth in technology (internet, mobile devices, social networks, cloud, etc.). As a result, digitalization is therefore revolutionizing financial services worldwide. Consumers are altering their purchasing habits through use of digital technologies, which increase their ability to access financial products and services at any time and from anywhere. Greater availability of information is creating more demanding customers, who expect swift, easy and immediate responses to their needs. And digitalization is what enables the financial industry to meet these new customer demands.

Technology is the lever for change which allows the value proposition to be redefined to focus on customers' real needs. The use of mobile devices as the preferred and often only tool for customers' interactions with their financial institutions has changed the nature of this relationship and the way in which financial decisions are made. It is crucial to offer customers a simple, consistent and user-friendly experience, without jeopardizing security and making the most of technological resources.

Artificial intelligence (AI) and big data are two of the technologies that are currently driving the transformation of the financial industry. Their adoption by various entities translates into new services for clients that more accessible and agile, and a transformation in internal processes. AI allows, among other things, offering personalized products and recommendations to customers and make decisions more intelligently. These technologies are not only in the hands of traditional companies but Fintech also makes use of them.

Data are the cornerstone of the digital economy. Financial institutions must make the most of the opportunities offered by technology and innovation, analyzing customer behavior, needs and expectations in order to offer them personalized and value-added services, and help them in making decisions. The development of algorithms based on big data can lead to the development of new advisory tools for managing personal finances and access to products which until recently were only available to high-value segments.

The digital transformation of the financial industry is boosting efficiency through automation of internal processes, with the use of new technologies to remain relevant in the new environment, such as blockchain and the cloud; data exploitation; and new business models (platforms). Participation in digital ecosystems through alliances and investments provides a way to learn and take advantage of the opportunities emerging in the digital world.

The financial services market is also evolving with the arrival of new players: companies offering financial services to a specific segment or focused on a part of the value chain (payment, finance, etc.). These companies are digital natives, rely on data use and offer a good customer experience, sometimes exploiting a laxer regulatory framework than that for the banking sector.

Regulatory Environment

1. Banking package for the reduction and distribution of risks to finalize the banking union

The most important focus in the European regulatory agenda in 2018 was the negotiation of the banking package that includes the measures proposed by the Commission intended to reduce and share risks in the banking industry. In recent years, the construction of the banking union project has made significant progress but there are still elements pending development, which regulators have been adjusting at the technical level throughout the year.

a) Prudential measures

The prudential measures proposed are intended to implement internationally agreed reforms between the years of 2014 and 2016 (which do not correspond to the standards known as Basel IV). Additional requirements include the requirement of a net stable financing ratio, or a leverage ratio, and the review of the capital requirements of the financial liabilities held for trading (fundamental review of the trading book - FRTB). At the same time, 2018 was the first year in which the Single Resolution Mechanism (SRM) communicated the Minimum Required Eligible Liabilities (MREL) for each European bank on the basis of the Bank Recovery and Resolution Directive 1 (BRRD 1).

b) Non-Performing Loans

In the advances made in the package of measures for the adequate recognition and valuation of non-performing loans, two provision backstops stand out: the addendum to the Guide on NPLs (Non-Performing Loans) of the ECB, within the supervisory dialog ensconced in Pillar II, already in force, and the proposal of the European Commission, for mandatory compliance contained within Pillar I, still under discussion. Minimum coverage levels are established for these loans based on the time they have been classified as non-performing and based on whether or not they have applicable guarantees in effect. Any lack of provisions must be deducted from the CET1 capital.

c) Guarantee systems

On the one hand, an agreement was reached to begin political negotiations involving the European deposit insurance scheme (EDIS). On the other hand, it was agreed at the June Euro Summit that the European Stability Mechanism (ESM) will evolve into the backstop for the Single Resolution Fund (SRF), with a maximum provision of €60.0 billion.

d) Sovereign risk

At the global level, the work performed by the Basel Committee establishes not to modify the regulatory treatment of sovereign exposures in the short term.

At the European level, the discussion focused on the development of a new low-risk asset backed by a set of Eurozone sovereign bonds (sovereign bond-backed securities - SBBS). According to the European Commission, these assets could potentially contribute to the diversification of the sovereign portfolios of credit institutions, as well as to reduce financial fragmentation.

These measures were encouraged in order to get all Banking Union elements operational in 2019, and thus to create greater integration and diversification in the European financial sector and to build a stronger and more resilient economic and monetary union.

2. Culmination of the Capital Markets Union (CMU)

In 2018, the European Commission advanced a number of its pending action plans to complete the Capital Markets Union (CMU) in mid-2019. These include: i) review of the Directive and Regulation of mortgage-covered bonds and the Regulation of simple, transparent and standardized securitization (STS) to boost both markets with the goal of lowering the cost of financing for the real economy and SMEs; ii) measures to facilitate the cross-border distribution of mutual funds and securities and boost the growth of SME markets; iii) a pan-European venture capital fund program (VentureEU) intended to stimulate investment in emerging and expanding innovative companies throughout Europe; and iv) a sustainable finance action plan, consolidating the regulatory importance of integrating this type of finance into the EU financial system, as well as the inclusion of environmental, social and governance issues (ESG) in long-term investment decision-making.

3. Current situation on the banking union in Europe

The revision of interbank offering rates (IBORs) continues in order to adapt them to international principles and European regulations on indexes in terms of methodology, transparency, governance and others. In 2018, the ECB formed a working group with representatives of the financial industry (ERFR) with the goal of identifying and recommending alternative risk-free indices to those existing in the eurozone today.

- The ERFR recommended the Euro Short-Term Rate (ESTER) prepared by the ECB as the alternative index to EONIA. The transition from EONIA to ESTER will be carried out in 2019 according to the ERFR work plan.

- The hybrid methodology that combines real operations and expert judgment advances in accordance with the deadlines established and could be implemented in 2019. The Euribor supervisor, FSMA (Financial Services and Markets Authority), confirmed that the results of the parallel exercise, between the current methodology and the new hybrid methodology, carried out by its administrator, EMMI (European Money Markets Institute), would allow to approve the new methodology during the second quarter of 2019.

4. Global discussions focused on the implementation of capital and resolution measures

Upon completion of the Basel III framework in December 2017, which is set to come into force in January 2022 (although some of its elements will not be fully operational until 2027), the European Commission began its preparation work in 2018 by publishing a Call for Advice (CfA) to the EBA on the implementation of Basel III in European legislation. For this reason, the EBA launched an ad-hoc quantitative impact study (QIS) in August. This exercise was based on the Basel QIS exercise, in which BBVA also participated.

With regard to financial institutions' recovery and resolution framework, there are open discussions that revolve around the implementation of the bail-in tool and the need for liquidity in resolution. For this reason, the Financial Stability Board (FSB) published its final guidelines on resolution funding, as well as a review on the implementation of the total loss-absorbing capacity guidelines (TLAC), in addition to bank resolution plans.

5. Regulation in the field of the digital transformation of the financial sector

In 2018, the digital transformation of the financial sector was specified as a priority for the authorities. In Europe, the Commission and the European Banking Authority published action plans, and in Mexico, a Law to Regulate Financial Technology Institutions was enacted. At the global level, the regulatory debate that began in 2017 intensified, and calls for greater international cooperation in the definition of the new regulatory framework for digital financial services increased.

The authorities have agreed on their identification of priorities. They have highlighted: i) the identification of measures to favor the controlled development of new business models, and barriers to the adoption of innovative technologies in the financial sector; and ii) the implementation of schemes to facilitate innovation (regulatory sandboxes -scheme to enable firms to test, pursuant to a specific testing plan agreed and monitored by a dedicated function of the competent authority, innovative financial products, financial services or business models- and innovation hubs -point of contact for firms to raise enquiries with competent authorities on FinTech-related issues and to seek non-binding guidance on the conformity of innovative financial products, financial services or business models with licensing or registration requirements and regulatory and supervisory expectations-). A legislative proposal was presented in Spain in 2018 to create a regulatory sandbox, which will be operational in 2019.

Cybersecurity also remained among the top priorities of the financial sector and authorities. Increases in the frequency and sophistication of cyberattacks explain why work continued to improve harmonization and international cooperation throughout 2018. Cybersecurity took center stage in the agenda of the European Commission and the European Central Bank in 2018.

The new Payment Services Directive (PSD2) came into force in January 2018, and work continued on the process defining the technical details throughout the course of the year. This Directive seeks to encourage competition and strengthen the security of payments in Europe. To this end, it regulates access to customer payment accounts by third parties that may offer information-aggregation services and initiate payments.

Digitization makes it possible to store, process and exchange large volumes of data. This trend facilitates the adoption of technologies, such as big data or artificial intelligence, but also raises concerns about how to ensure the privacy and integrity of customer data. In Europe, this has materialized in the form of two regulations: the General Regulation of Data Protection (GDPR), which came into force in May 2018, and the e-Privacy Regulation, which is still under debate.

The recognition of data as a strategic asset in the digital economy increased in 2018, making it necessary to create attractive value propositions and strengthen customer confidence. In 2018, the approval of the new European regulation of free flow of non-personal data joined the open-banking regulations, such as the aforementioned PSD2 and GDPR, or the standards included under the Fintech law in Mexico, which regulate accessibility and the right to portability of data, was added in 2018.

In addition, the public debate on the role of large technology companies in the digital economy and financial sector intensified throughout the course of the year. In Europe, the Commission presented a proposal for regulations to delimit certain obligations in its role as a platform for the intermediation of online services, in the interest of transparency and equity. It is expected that this trend will continue throughout 2019.

Economic outlook

The global environment has deteriorated during the second half of 2018, with a more evident effect of the increase in protectionism in global trade and the industrial sector together with the signs of a slowdown in China, the Eurozone and the United States. Faced with this scenario of further global uncertainty, the main central banks have shown signs of caution in their normalization plans, and have been key to containing the sharp rise in financial tensions. The update of the BBVA Research scenario takes into account this new environment, and is based on the assumption that high financial volatility may continue during the first half of the year 2019, should some the uncertainties weighing on the global panorama not dissipate (an agreement between the United States and China to curb trade disputes and avoid a new tariff hike, a solution that avoids a no-deal Brexit, and confirmation of a more deliberate tone in the Fed's monetary policy). In consideration of this, BBVA Research's forecast is for a smooth deceleration of the global economy, from 3.6% in 2018 to 3.5% in 2019 and 3.4% in 2020.

In terms of countries, the moderation of growth will be more evident in developed economies. In the United States, the moderation observed in the second half of last year, linked to the poorer performance of domestic demand and the recent appreciation of the dollar, is likely to continue. The aforementioned, linked to the gradual disappearance of the effects of the fiscal stimuli introduced last year and without private investment taking over as an economic engine, this will lead to a projected slowdown in growth from 2.9% in 2018 to 2.5% in 2019 and 2% in 2020. The recovery in the Eurozone has already suffered from lower global demand and more moderate growth is expected, around 1.4% in the 2019-20 period, after the 1.8% estimated in 2018. This growth is based on the strength of domestic fundamentals and the support of an accommodative monetary and fiscal policy. This dynamic will also have an impact on Spain's growth, although it will still remain above the Eurozone average, with a gradual slowdown from 2.5% in 2018 to 2% in 2020.

Growth in the emerging economies will remain relatively stable, although it will hide a different pattern among countries. In general, a slowdown is expected in the Asian economies being negatively affected by lower growth in China, from 6.6% in 2018 to 6.0% in 2019 and 5.8% in 2020, while the recovery will gain traction in Latin American countries (1.6% in 2018, 2.1% in 2019 and 2.4% in 2020). Growth is set to remain relatively stable in Mexico and Peru in the 2018-20 period, while a gradual recovery is expected in Colombia and Brazil. In Argentina, the activity could contract again by around 1.0% in 2019 after the sharp decrease of 2.4% in 2018, due to the contractionary policies applied; however, these will be smoothed over time, which will allow growth of approximately 2.5% in 2020. In Turkey, the adjustment process of the economy continues after the tightening of monetary and fiscal policies to correct the imbalances generated in previous years, so that the slowdown in growth will persist in 2019 (1.0%) before starting to gain some degree of momentum in 2020 (2.5%).

The scenario continues to be that of a mild slowdown of the global economy, but remains increasingly uncertain due to risks as protectionism; the adjustment of activity, both in the United States as well as China; and the increasing uncertainty in Europe, mainly linked to the Brexit and other political factors.

Strategy and business model

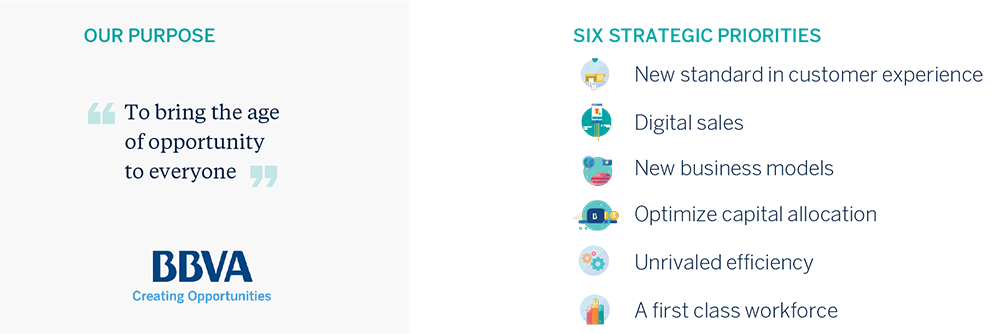

BBVA made significant progress in its transformation process during 2018, based on its Purpose, the six Strategic Priorities, and its Values, all of which are fundamental pillars of the Organization's overall strategy.

Vision and aspiration

BBVA is a transformation process that is necessary for adapting to the new environment in the financial industry, characterized by trends that confirm the Group's strategic vision, that is, a reconfiguration of the entire financial services industry is taking place. These trends are the following:

- A complex macroeconomic environment, characterized by strong regulatory pressure, low interest rates, high currency volatility, and geopolitical risks.

- A highly regulated banking industry, that is, traditional banking subject to a large number of legal regulations, both globally and locally.

- A shift in the needs and expectations of customers who demand higher value-added services that enable them to achieve their objectives, with a simple, transparent and immediate relationship model similar to the one they already enjoy with a number of other highly digitized industries.

- Certain data that is evolving into a strategic asset. Given the large amount of data stored within organizations, the ability to interpret and make value proposals to customers is considered to be critical, provided there is customer consent under all circumstances.

- Certain technological giants, with business models based on data that create ecosystems where the lines between different types of businesses are getting blurred.

- Greater competition as a result of the arrival of new players who focus on the most profitable aspects of the value chain.

In this context, the main objective of the Group's transformation strategy its aspiration is to strengthen the relationship with its customers.

New value proposition

Progress in BBVA´s transformation journey

BBVA advanced in fulfillment of its Purpose in 2018: To bring the age of opportunity to everyone, which is reflected in the tagline: Creating Opportunities. We want to help our customers make better financial decisions and attain their life goals; we want to be more than a bank, we want to be an engine of opportunities and have a positive impact on peoples’ lives and companies’ businesses.

In this respect, important steps were taken in the development of the six Strategic Priorities of the Group throughout the year in order to continue its advances in the transformation process. These advances were reflected in the results of key performance indicators (KPIs).

Strategic priorities

1. A new standard in customer experience

BBVA Group's main focus is based on providing a new standard in customer experience that stands out for its simplicity, transparency and swiftness, further empowering its customers while offering them personalized advice.

BBVA's business model is customer-oriented, with the goal of being a leader in customer satisfaction across its global footprint. In order to learn more about the degree of customer recommendation, and, in turn, their degree of satisfaction, the Group uses the Net Promoter Score (NPS) methodology, which recognizes BBVA as one of the most recommendable banking entities in every country where it operates.

Likewise, progress in customer satisfaction is reflected in the positive performance of strategic indicators such as the target customers (segment of customers which the Group wishes to grow and retain), as well as its corresponding client attrition rate. The digital customers base are more satisfied and this translate into digital clients attrition rate reduction (-47% vs non digital clients). In short, BBVA is making progress in its strategy, and succeeding in attracting a greater number of customers, who are also more satisfied and more loyal.

2. Digital sales

BBVA's relationship model is evolving to adapt to the growing multi-channel customer profile, which is why it is essential to foster digitalization. For this purpose, it is developing an important digital offering including products and services that let customers use the most convenient channel for them.

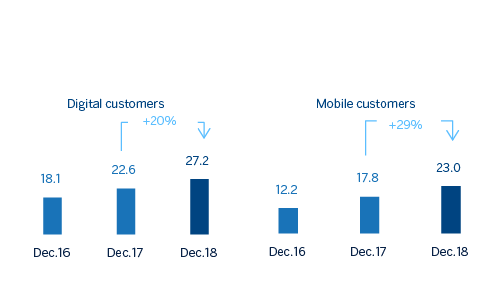

The number of digital and mobile customers of the Group grew considerably in 2018, reaching the tipping point of 50% in digital customers at the Group level and in six countries where BBVA operates: Spain, The United States, Turkey, Argentina, Colombia and Venezuela.

Digital and mobile customers (BBVA Group. Million)

Furthermore, a significant boost to digital channel sales is being made, which is having a very positive evolution across the global footprint. In 2018, 41% of sales were made through the Group's digital channels compared to 28% in the previous year.

3. New business models

Throughout 2018, BBVA continued to consolidate itself as one of the leading banks in terms of digital transformation and activity in the entrepreneurship ecosystem. The Group is actively participating in the disruption of the financial industry in order to incorporate key findings into the Bank's value proposition, both through the search for new digital business models as well as the leveraging of the FinTech ecosystem. This activity is being implemented in five key levers: i) exploring (Open Talent y Open Summit); ii) constructing (Upturn and Azlo); iii) partnering (Alipay); iv) acquiring and investing (Solaris and the increase of participation in Atom); and v) venture capital (Sinovation and Propel).

4. Optimize capital allocation

The objective of this priority is to improve the profitability and sustainability of the business while simplifying and focusing it on the most relevant activities. Throughout 2018, efforts continued to promote the correct allocation of capital and this is allowing the Group to continue improving in terms of solvency. Thus, the fully-loaded CET1 capital ratio stood at 11,3% at the end of the year, up 26 basis points on the close of 2017.

CET1 fully-loaded (Percentage)

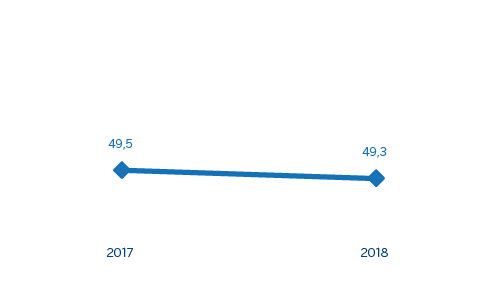

5. Unrivaled efficiency

In an environment of lower profitability for the financial industry, efficiency has become an essential priority in BBVA's transformation plan. This priority is based on building a new organizational model that is as agile, simple and automated as possible. In 2018, the Group's efficiency ratio stood at 49,3%, which is lower than the previous year (49,5%).

Efficiency ratio (Percentage)

6. A first-class workforce

BBVA Group’s most important asset is its people; therefore, a first class workforce is one of the six Strategic Priorities, which entails attracting, selecting, training, developing and retaining top-class talent.

BBVA Group has developed new people management models and new ways of working which have enabled the Bank to keep transforming its operational model, but have also promoted cultural transformation and have favored the ability to become a purpose-driven company, or, in other words, a company where staff guide their actions according to the Values, and are genuinely inspired and motivated by the same Purpose.

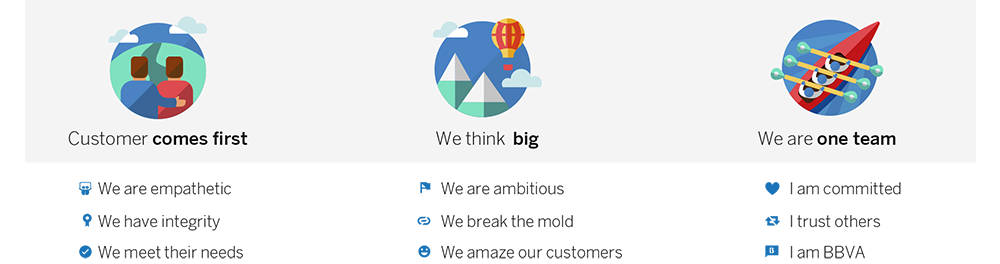

Our Values

BBVA is engaged in an open process to identify the Group's Values, which took on board the opinion of employees from across the global footprint and units of the Group. These Values define our identity and are the pillars for making our Purpose a reality:

1. Customer comes first

BBVA has always been customer-focused, but the customer now comes first before everything else. The Bank aspires to take a holistic customer vision, not just financial. This means working in a way which is empathetic, agile and with integrity, among other things.

- We are empathetic: we take the customer's viewpoint into account from the outset, putting ourselves in their shoes to better understand their needs.

- We have integrity: everything we do is legal, publishable and morally acceptable to society. We always put customer interests' first.

- We meet their needs: we seek excellence in everything we do in order to amaze our customers, creating unique experiences and solutions which exceed their expectations.

2. We think big

It is not about innovating for its own sake but instead to have a significant impact on the lives of people, enhancing their opportunities. BBVA Group is ambitious, constantly seeking to improve, not settling for doing things reasonably well, but instead seeking excellence as standard.

- We are ambitious: we set ourselves ambitious and aspirational challenges to have a real impact on people's lives.

- We break the mold: we question everything we do to discover new ways of doing things, innovating and testing new ideas which enables us to learn.

- We amaze our customers: we question everything we do to discover new ways of doing things, innovating and testing new ideas which enables us to learn.

3. We are one team

People are what matters most to the Group. All employees are owners and share responsibility in this endeavor. We tear down silos and trust in others as we do ourselves. We are BBVA.

- I am committed: I am committed to my role and my objectives and I feel empowered and fully responsible for delivering them, working with passion and enthusiasm.

- I trust others: I trust others from the outset and work generously, collaborating and breaking down silos between areas and hierarchical barriers.

- I am BBVA: I feel ownership of BBVA. The Bank's objectives are my own and I do everything in my power to achieve them and make our Purpose a reality.

The Values are reflected in the daily life of all BBVA Group employees, influencing every decision.

The implementation and adoption of these Values is supported by the entire Organization, including senior management, launching local and global initiatives which ensure these Values are adopted uniformly throughout the Group. Thus, in 2018 the core values were present in the various people management levers (recruitment, training, development, etc.), as well as in agile and budget management processes. Within the people management levers, a new people assessment model was launched, in which the cultural skills of 97% of employees were evaluated. In the global report it has been verified that the best rated value (4.66 out of 5) and, therefore, the most focused-on principle for the Entity is the concept of Customer comes first.

In addition, in July 2018, BBVA held its first global Values Day, an event that took place across its global footprint, with the objective that employees reflect on the implications of values and propose actions for their effective implementation. The main activity at this global event was workshops organized to identify improvement projects and determine opportunities has for implementing its values in the Group. In these workshops:

- more than 23,000 employees (nearly 20% of the total) from different countries and areas participated;

- they took place both at corporate headquarters around the world, as well as through activities in the branch network;

- Mexico was the country with the highest participation in the workshops, with a total of 11,475 participants (31%);

- Customer comes first value was the most cited value at a global level, 47% of the participants focused on this value, and one in four employees focused on We meet their needs behavior;

- the online and individual version of the workshop that was made available to all employees through an ad-hoc web app for this event had participation levels of 63%.

In short, Values Day helped to create listening mechanisms and transform employees' feedback into data through machine-learning algorithms; thus becoming an event specific to a data-driven organization.

In addition, in 2018 BBVA shared Our Values with other stakeholders: with customers through the actions carried out in branches during the Values Day; with shareholders in the framework of the General Shareholders' Meeting; and with society in general, with the publication of articles specialized in media of different countries. More than 500 local initiatives have also been launched to consolidate the relationship with customers, promote the transforming vocation of teams and collaborative work schemes and encourage the feeling of belonging to BBVA.

Materiality

BBVA performs a materiality analysis in order to become aware of and prioritize the most relevant issues, both for its key stakeholders and for its overall strategy. In other words, it is an analysis that contributes to the development of the business strategy in line with what is expected of the Group, as well as a way to determine what information should be reported.

In 2018, in addition to the data-based analysis already in use in recent years, there has been participation from the Strategy & M&A area, and the collaboration of different stakeholder teams (Client Solutions, Talent & Culture, Investor Relations, Supervisory Relations, Legal Services, and Responsible Business). This has improved the process of identifying relevant issues and led to a deeper debate on the relationship between the priorities of the stakeholders and business strategies.

The materiality analysis phases were as follows:

- 1. Identification of relevant issues for each of the stakeholders based on interviews with the teams they interact with. These, in turn, relied on information that was obtained from the usual listening and dialog tools.

- 2. Agregation into a single list, based on all issues identified for each of the stakeholders. BBVA made a list of twelve issues.

- 3. Prioritization of issues according to their importance to the stakeholders. BBVA carried out a series of surveys and interviews with various stakeholders, as well as an analysis of social media and networks. In order to complete the prioritization, an analysis on trends and sectoral data was made, based on data from Datamaran, from which the issues most relevant to their peers were obtained.

- 4. Subjects were prioritized according to their impact on BBVA's strategy. The strategy team assessed how each issue impacts the six Strategic Priorities. The most relevant issues for BBVA are those that help it achieve its strategy to a greater extent.

The result of this analysis is contained in the Group's materiality matrix.

Therefore, the five most relevant issues or BBVA's business strategy and its stakeholders are (in order of joint importance):

- Easy, fast and DIY (do it yourself): stakeholders expect to operate in an agile and simple way with BBVA, at any time and from anywhere, leveraging in the use of new technologies. These new technologies will allow greater efficiency in the operation, generating value for the shareholders.

- Solvency and sustainable results: stakeholders expect BBVA to be a robust, solvent and sustainable bank, thus contributing to the stability of the system. They demand a business model that responds to changes in the context: disruptive technologies, new competitors, geopolitical issues, etc.

- Ethical behavior and consumer protection: stakeholders expect BBVA to behave in a comprehensive manner and to protect clients or depositors by acting transparently, offering products that are appropriate to their risk profile and managing the ethical challenges presented by certain new technologies with integrity.

- Adequate and timely advice to customers: stakeholders expect BBVA to provide appropriate solutions to clients' personal needs and circumstances. It is also expected that the Bank will help them in managing their finances, proactively and with proper handling.

- Cybersecurity and responsible use of data:: stakeholders expect their data to be secure at BBVA and to used only for agreed purposes, always complying with current law. This is critical to maintaining trust.

Information on the Group's performance in these relevant matters in 2018 is reflected in the different chapters of this Management Report.

Responsible banking model

At BBVA we have a differential banking model that we refer to as responsible banking, based on seeking out a return adjusted to principles, strict legal compliance, best practices and the creation of long-term value for all stakeholders. It is reflected in the Bank's Corporate Social Responsibility or Responsible Banking Policy. The Policy's mission is to manage the responsibility for the Bank's impact on people and society, which is key to the delivery of BBVA's Purpose.

All the Group’s business and support areas integrate this policy into their operational models. The Responsible Business Unit coordinates the implementation and basically operates as a second line for defining standards and offering support.

The responsible banking model is supervised by the Board of Directors and its committees, as well as by the Bank's senior management.

The four pillars of BBVA's responsible banking model are as follows:

- Balanced relations with its customers, based on transparency, clarity and responsibility.

- Sustainable finance to combat climate change, respect human rights and achieve the UN Sustainable Development Goals (SDGs).

- Responsible practices with employees, suppliers and other stakeholders.

- Community investment to promote social change and create opportunities for all.

In 2018, BBVA approved its climate change and sustainable development strategy to contribute to the achievement of the Sustainable Development Goals (SDGs) and aligned with the Paris Agreement. This strategy is described in the Sustainable finance chapter.

Customer relationship

Customer experience

One of the Group's Strategic Priorities is a new standard in customer experience, that is, to ensure that the customer experience is distinguished by its simplicity, transparency, and swiftness, to further the customers empowerment and to offer them personalized advice. In 2018, BBVA's value proposition with its clients evolved with focus on several value streams: DIY – Do it yourself, Open Market, Physical & Human touchpoints, Advice and Smart Interactions, for both retail and company projects. In this sense, the solutions were more aligned with the needs of the customers, which had a direct effect on the customer experience. In parallel, BBVA also wants to be prepared to face possible disruptive trends that can change the current paradigm, which is why we also work on projects that may have an impact over a time horizon of more than 5 years

Through new ways of doing things and organizing (working in agile and applying a new operating model) the development of solutions is prioritized, a greater alignment and coordination at the Group level is created and the development of global solutions is motivated. All this contributes to offer better solutions in less time for customers while improving internal efficiency. In addition, BBVA works with an open banking mentality, which means working with third parties to offer customers the best solutions available in the market and also to be able to offer these solutions to the clients of these third parties.

Over the 2018, BBVA continued to build global products and capabilities. One example of this is GloMo (GLobal Mobile), a mobile banking platform developed globally by BBVA that is already available in Mexico and Uruguay, and is expected to be launched in Peru in 2019. This new BBVA application is the first one that has been built on a global development platform, which provides efficiency and optimizes resources, allowing for the reuse of components. This type of development allows for service modularity, making it possible to unify the customer experience in all countries with a unique design, but with a navigation logic adapted to the needs of the client in each country.

Net Promoter Score

In 2018, BBVA consolidated the quality and customer experience model that was launched in the previous year, year, placing the customer at the center of decisions, with a very clear and ambitious goal: to offer a differential service, regardless of the channel of communication they choose and to allow to be leaders in customer satisfaction in all the geographical areas in which it operates.

The internationally recognized Net Promoter Score (NPS or Net Recommendation Index – (IReNe, for its acronym is Spanish) methodology calculates the level of recommendation, and hence, the level of satisfaction of BBVA customers with its different products, channels and services. This index is based on a survey that measures on a scale of 0 to 10 whether a bank's customers are positive (score of 9 or 10), neutral (score of 7 or 8) or negative (score of 0 to 6) when asked if they would recommend their bank, a specific product or a channel to a friend or family member. This is vital information for identifying their needs and drawing up improvement plans, on multidisciplinary teams work to create unique and personal experiences.

The Group's internalization and application of this methodology over the last eight years has led to a steady increase in the customers' level of trust, as they recognize BBVA to be one of the most secure and recommendable banking institutions in every country where it operates.

In 2018, BBVA ranked first in the NPS indicator in six countries: Spain, Mexico, Turkey, Peru, Uruguay and Paraguay and second in Colombia.

TCR Communication

The Transparent, Clear and Responsible (TCR) Communication project promotes transparent, clear and responsible relations between BBVA and its customers.

- T is for transparency: providing customers with all relevant information at the right time, maintaining a balance between benefits and costs.

- C is for clarity, meaning easy to understand. It is achieved by the Group through language, structure and design.

- R is for responsibility, and means looking after the customers' interests in the short, medium and long term.

The objectives are to help customers make informed decisions, improve customer relations with the Bank, look out for their interests and make BBVA the most transparent and clearest bank in all the markets where it operates. It also means BBVA can attract new customers and encourage existing customers to recommend it.

In 2018, the project had three lines of work:

- Implement the TCR principles as they pertain to new digital solutions, with the participation of TCR experts in the global design of the BBVA mobile application, whose development, adaptation and implementation was made for Mexico and Peru, and collaboration in the development of the new Public Web in Mexico, Colombia and Peru. Work continues on a large number of global digital projects, both for mobile and for the web.

- Incorporate the TCR principles in the key content intended for customers, with the performance of maintenance works of TCR materials (files deliverable to customers, contracts, sales scripts, and claim letter responses) and the objective of continuing with all applicable updates, putting focus on improving the customer experience.

- Spread TCR principles throughout the Group, by means of training provided in workshops directed principally to digital project teams in Spain, Mexico, Argentina, Colombia and Peru. In addition, two new editions of the Clear Language in BBVA program were launched, which earned a satisfaction rating of 4.8 out of 5; the online course TCR Apply was created to help apply these principles on a day-to-day basis; and the TCR training was extended to the legal departments in Spain, Argentina, Colombia.

The project is coordinated by a global team working together with a network of local TCR owners located in the main countries in which the Group has a presence, and various Bank areas and individuals participate in its implementation.

TCR Indicators

BBVA uses an indicator, the Net TCR Score (NTCRS), which allows us to measure the degree to which customers perceive BBVA as a transparent and clear bank compared to its peers in the main localities.

Customer care

Complaints and claims

BBVA has an appropriate claims management and service model that positively transforms the customer experience. In this way, every interaction that the Group has with its customers is an opportunity to improve this model, thus ensuring that the business is customer-centric and transforming these interactions into positive experiences. This is important because one of the key moments determining customer experience is considered to be when a customer communicates dissatisfaction with a product or service, that is, when complaints and claims are received.

Following the path of digital transformation, any type of opinion that the customer provides by any means (NPS, digital feedback, complaints, claims, etc.) is examined, with the objective of learning more about their opinions and of having the opportunity to help them resolve any problem by offering simple, clear, agile and personalized responses.

Main indicators of claims (BBVA Group)

| 2018 | 2017 | |

|---|---|---|

| Number of claims before the banking authority (for each 10,000 active customers) | 9.40 | 10.02 |

| Average time for settling claims (normal days) | 7 | 7 |

| Claims settled by First Contact Resolution (FCR) (% over total claims) | 26 | 31 |

The various Group claims units are constantly evolving, optimizing processes and improving the management and care model, as a key aspect of differentiation in an increasingly competitive environment, thus reinforcing the objective of offering a unique experience to customers and the fulfillment of BBVA's aspiration: to strengthen the relationship with its customers.

These claims units focus their efforts on:

- reviewing and constantly monitoring claim metrics trends and the causes that generate these claims;

- implementing action plans focused on solving the root causes that generate these claims; and

- improving the execution of processes through their optimization or automation, finding a suitable balance of efficiency and improvement in the customer experience.

All of the registered and available information regarding claims in the Group is reviewed periodically through a global online site, with customized queries generated depending on the indicator or variable that is to be analyzed. The Group's senior management has a direct involvement in the follow-up of customer claims and complaints.

In short, BBVA’s claim management is an opportunity to offer greater value to customers and strengthen their loyalty to the Group, to achieve its aspiration to strengthen the relationship with its customers. In this respect, BBVA aims to promote greater agility and simplicity in the management of complaints and claims, through the implementation of optimal processes in this management, with the focus on the elimination of the main causes that generate the claims and with resolution of alternatives upon first contact.

As a result of the improvements implemented in the claims management process in BBVA, these registered a significant decrease in 2018 (-39.0% with respect to the figure of the previous year), basically in Spain and Mexico. This last country, with the biggest active customer base of the Group, is also the country with the biggest number of claims.

Number of claims before the banking authority by country (Number for each 10,000 active customers) (1)

| 2018 | 2017 | |

|---|---|---|

| Spain | 3.54 | 4.87 |

| The United States | 4.56 | 4.96 |

| Mexico | 17.94 | 16.12 |

| Turkey | 4.03 | 3.21 |

| Argentina | 1.11 | 2.68 |

| Chile | - | 5.55 |

| Colombia | 21.56 | 21.65 |

| Peru | 1.19 | 2.21 |

| Venezuela | 0.47 | 1.04 |

| Paraguay | 1.19 | 0.79 |

| Uruguay | 0.68 | 0.41 |

| Portugal | 21.92 | 34.84 |

- Scope: BBVA Group

- (1) The banking authority refers to the external body in which the customers can complain against BBVA.

The average time for resolving claims in the Group is maintained in 7 days, improving in Spain (10 days compared to 25 the previous year) and in Peru.

Average time for settling claims by countries (Normal days)

| 2018 | 2017 | |

|---|---|---|

| Spain | 10 | 25 |

| The United States | 4 | 3 |

| Mexico | 5 | 4 |

| Turkey | 2 | 2 |

| Argentina | 7 | 7 |

| Chile | - | 5 |

| Colombia | 5 | 4 |

| Peru | 9 | 12 |

| Venezuela | 13 | 13 |

| Paraguay | 6 | 6 |

| Uruguay | 7 | 8 |

| Portugal | 4 | 5 |

The claims settled by the First Contact Resolution (FCR) model account for 26% of total claims, thanks to the management and handling of these claims aims to reduce resolution times and increase the service quality, thus improving the customer experience.

Claims settled by First Contact Resolution (FCR. Percentage over total claims)

| 2018 | 2017 | |

|---|---|---|

| Spain(1) | n.a. | n.a. |

| The United States | 54 | 63 |

| Mexico | 30 | 38 |

| Turkey(2) | 38 | 44 |

| Argentina | 21 | 27 |

| Chile | - | 6 |

| Colombia | 69 | 73 |

| Peru | 8 | 4 |

| Venezuela | 0 | 1 |

| Paraguay | 39 | 28 |

| Uruguay | 14 | 12 |

| Portugal(3) | n.a. | n.a. |

- n.a. = not applicable

- (1) In Spain, is applicable a FCR type called IRR (Immediate resolution response) to credit card incidents, but not claims.

- (2) In Turkey, the weighting is calculated by the total number of customers.

- (3) This kind of management does not apply in Portugal.

Customer Care Service and Customer Ombudsman

In 2018, the activities of the Customer Care Service and Customer Ombudsman were carried out in accordance with the stipulations of article 17 of the Ministerial Order (OM) ECO/734/2004, dated March 11, of the Ministry of Economy, regarding customer care and consumer ombudsman departments at financial institutions, and in line with BBVA Group's Regulation for Customer Protection in Spain, approved in 2015 by the Bank's Board of Directors, with regard to regulation of the activities and powers of the Customer Care Service and Customer Ombudsman.

In accordance with the aforementioned regulation, the Customer Ombudsman has been made aware of and resolved, in the first instance, all complaints and claims submitted by the participants and beneficiaries of the pension plans, as well as those related to insurance and other financial products that BBVA Group Customer Care Service considered appropriate to escalate, based on the amount or particular complexity, as established under article 4 of the Regulation for Customer Protection.

Likewise, the Customer Ombudsman has been made aware of and resolved, in the second instance, all complaints and claims that customers opted to submit for their consideration after having obtained a dismissal resolution from the Customer Care Service.

Activity report on the Customer Care Service in Spain

The activity of the Customer Care Service takes place within the scope of the O.M ECO / 734 and in compliance with the competences and procedures established in the Regulation for the Defense of Customers in Spain of the BBVA Group. As stipulated in the Regulations, the Customer Care Service is entrusted with the task of dealing with and resolving the complaints received from customers in relation to the products and services marketed and contracted in Spanish territory by the entities of the BBVA Group.

The Customer Care Service in compliance with the European guidelines on claims established by the competent authorities ESMA (European Securities Market Authority) and EBA (European Banking Authority), works to detect the recurrent, systemic or potential problems of the Entity.

Like previous years, 2018 has been characterized by a complex environment. The main types of claims have been related to mortgage loans.

The Customer Care Service (SAC) continued the training plan that was launched in 2017 for the whole team. This plan has addressed, among other issues, regulations on transparency and protection of customers, as well as obligations arising from contracts for products and services. The objective of the plan is to guarantee adequate knowledge for managers in order to facilitate the continuous improvement in the claims management and the identification of the root causes thereof.

Claims of customers admitted to BBVA's Customer Care Service in Spain amounted to 84,533 cases in 2018, 51% less than in 2017, of which 81,626 were resolved by the Customer Care Service and concluded in the same year, which represents 97% of the total. 2,907 claims remained pending analysis. On the other hand, 42,688 claims were not admitted for processing as they did not meet the requirements set out in OM ECO/734. Nearly 40% of the claims received corresponded to mortgage loans, mainly mortgage arrangement expenses.

Complaints handled by Customer Care Service by complaint type (Percentage)

| Type | 2018 | 2017 |

|---|---|---|

| Resources | 29 | 9 |

| Assets products/loans | 39 | 79 |

| Insurances | 3 | 1 |

| Collection and payment services | 5 | 2 |

| Financial counselling and quality service | 4 | 2 |

| Credit cards | 13 | 4 |

| Securities and equity portfolios | 1 | 1 |

| Other | 6 | 2 |

| Total | 100 | 100 |

Complaints handled by Customer Care Service according to resolution (Number)

| 2018 | 2017 | |

|---|---|---|

| In favor of the person submitting the complaint | 25,970 | 29,041 |

| Partially in favor of the person submitting the complaint | 18,563 | 90,047 |

| In favor of the BBVA Group | 37,093 | 52,058 |

| Total | 81,626 | 171,146 |

Activity report of the BBVA Group´s customer ombudsman in Spain

In 2018, the Customer Ombudsman, along with the BBVA Group, has maintained the objective of unifying criteria and fostering the protection and security of customers, making progress in compliance with transparency and customer protection regulations. In order to efficiently translate their observations and criteria on the matters submitted for their consideration, the Ombudsman promoted several meetings with the Group's areas and units: Insurance, Pension Plan Manager, Business, Legal Services, etc.

In this sense, the Customer Ombudsman has been holding a Claims Follow-up Committee on a monthly basis, with the main objective of keeping a permanent dialog with the BBVA Group Services that contribute to positioning the Group in relation to its customers. The Directors of Quality, Legal Services and the Customer Care Service attend this committee. Likewise, the Customer Ombudsman participates in the Transparency and Good Practices Committee, in which the Bank's actions are analyzed, in order to adapt them to the regulations on transparency and good banking practices and standards.

Customer claims managed in the Customer Ombudsman's Office for a decision during the year 2018 have amounted to 3,020 cases. Of these, 114 have not been finally admitted for processing as they did not meet the requirements of Ministerial Order (OM) ECO/734/2004, and 133 remained as pending as of 31-12-18.

Complaints handled by the Customer Ombudsman office by complaint type (Number)

| Type | 2018 | 2017 |

|---|---|---|

| Insurance and welfare product | 753 | 600 |

| Assets operations | 709 | 367 |

| Investment services | 146 | 133 |

| Liabilities operations | 753 | 257 |

| Other banking products (credit card, ATM, etc.) | 437 | 140 |

| Collection and payment services | 106 | 69 |

| Other | 116 | 95 |

| Total | 3,020 | 1,661 |

The categorization of the claims managed in the previous table follows the criteria established by the Claims Department of the Bank of Spain, in its requests for information.

Complaints handled by Customer Ombudsman office according to resolution (Number)

| 2018 | 2017 | |

|---|---|---|

| In favor of the person submitting the complaint | - | - |

| Partially in favor of the person submitting the complaint | 1,482 | 797 |

| In favor of the BBVA Group | 1,290 | 622 |

| Processing Suspended | 1 | 8 |

| Total | 2,773 | 1,427 |

51.3% of customers who brought claims before the Customer Ombudsman during the course of the year obtained some type of satisfaction, total or partial, by resolution of the Customer Ombudsman in 2018. Customers unsatisfied by the Customer Ombudsman's response may appear before the official supervisory bodies (Bank of Spain, CNMV and General Directorate of Insurance and Pension Funds). The number of claims submitted by customers to supervisory bodies was 260 in 2018.

In 2018, the BBVA Group continued to make progress in the implementation of the different recommendations and suggestions of the Customer Ombudsman with regard to adapting products to the customer profiles and the need for transparent, clear and responsible information. All recommendations and suggestions of the Customer Ombudsman focus on raising the level of transparency and clarity of the information that BBVA Group provides for its customers, both in terms of commercial offers available to them for each product, and in compliance with the orders and instructions thereof, so that the following is guaranteed:

- an understanding by customers of the nature and risks of the financial products offered to them,

- the suitability of the product for the customer profile, and

- the impartiality and clarity of the information that the Entity targets at customers, including advertising information.

In addition, and with the advance in the digitalization of the products offered to customers and the increasing complexity thereof, a degree of special sensitivity is required with certain groups that, due to their profile, age or personal situation, present a certain degree of vulnerability.

Operational risk management and customer protection

The security measures at BBVA continued to be reinforced in 2018 through its monitoring and cyberprotection capabilities, for both employees and customers. In this respect, and alongside the strategy of using data as the main point of relationship with customers, analytical capabilities were developed that allow for the new threats associated with cybersecurity through data, and to combat them from a preventive viewpoint. Furthermore, a new program was created focusing on providing suitable protection of the Group's information, which is considered one of the main assets and which also allows it to adapt to any new regulations that may arise within the industry.

During the year 2018, a series of process services and security services in the field of Engineering has been introduced and improved. All this has been a direct result of the teamwork of the different technical areas that collaborated in improving the user experience and security. It is worth mentioning the improvement of the process of digital onboarding in Spain, introduced in the financial market in a pioneering manner in 2016; the improvement in the time required to become a customer through new validation techniques that guarantee customer identity; and the set-up of our own in-house developments allowing facial biometric payment, already underway with employees and planned for implementation with customers.

Various initiatives have been taken in 2018 in the area of business continuity, i.e., for incidents with low probability of occurrence but very high impact, mainly with regard to the enhancement of the Continuity Plan management tools. To be specific, the business impact analysis was updated, and the technological dependences on which the critical processes are based were reviewed, informing the corresponding continuity committees of their results so that, when applicable, they are aware of them and are able to improve their responses in case of unavailability due to information system failures.

Over the course of the year, various business continuity strategies were activated within the Group, including those related to torrential rains and hurricanes in the United States, and others pertaining to one-time social conflict events, problems with electrical/water supplies, and the extraordinary monitoring of the process of monetary reconversion in Venezuela.

With regard to personal data protection, the project for the implementation of the General Data Protection Regulation (GDPR) was finalized in the Group companies and branches in 2018. It is a continuous and living process, which means that each new product or service must comply with privacy requirements from its design, requiring a firm commitment to ensure respect for the fundamental right to the personal data protection. In addition, the protection of personal data is being strengthened in other areas with regard to suppliers and employees, where new protocols have been adopted in accordance with aforementioned regulation.

In addition, BBVA carried out a communication process with its customers on the new requirements imposed by the GDPR and the new range of rights that the data holders hold. For that, different communication channels were used: branches, postal mail, ATM and digital channels.

Educational and awareness-raising actions were carried out in this regard, in the area of employee training, planned for all those who form part of the Group, by areas and departments, and which culminate in the incorporation of a specific course on data protection in the corporate training catalog.

The position of the data protection delegate as a guarantor of the respect of the fundamental right to the personal data protection was reinforced and strengthened in 2018. Its team has progressively equipped itself with the resources and tools necessary to undertake all tasks entrusted to it in accordance with regulations, in order to guarantee the fulfillment of its duties and functions.

Finally, work is being carried out on the internal adaptation required by the new Organic Law for the Personal Data Protection.

Staff information

People management

BBVA's most important asset is its team, the people who make up the Group. For this reason, one of the six Strategic Priorities is having a first-class workforce. In this context, BBVA accompanies its transformation strategy with different initiatives in questions involving employees, such as:

- Development of a more transversal, transparent and effective model of people management, in such a way that each employee can occupy the most appropriate role for their profile in order to bring the greatest value to the Organization, with the greatest commitment; and, in turn, learn and grow professionally.

- Evolution in the forms of working towards an agile organizational model, in which teams are directly responsible for what they do, building everything from customer feedback and which are focused on the delivery of solutions that best meet current and future needs of the clients.

- Promoting a corporate culture of collaboration and entrepreneurship, which revolves around a set of values and behaviors that are shared by the individuals of the Group and which generate identity traits that differentiate it from other entities (see Our Values in the corresponding section of the Strategy and business model chapter).

- Incorporation of talent in a range of capacities not usually found in the financial sector, but which are key in the new stage in which the Group finds itself (data specialists, customer experience, etc.).

All this has enabled to become a purpose-driven company, that is, a company where staff guide their actions according to the Values, and are genuinely inspired and motivated by the same Purpose.

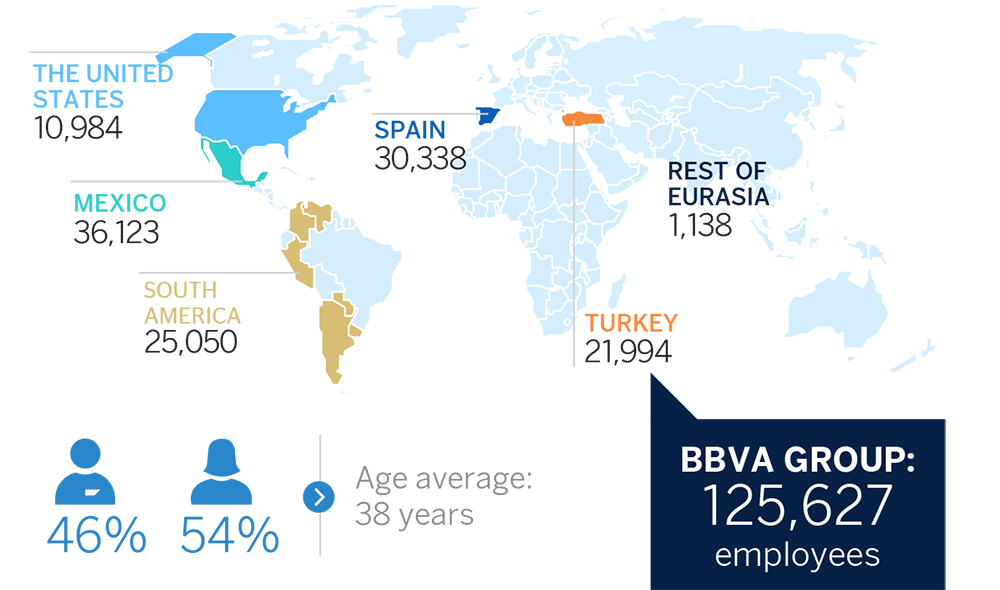

As of December 31, 2018, the BBVA Group had 125,627 employees located in more than 30 countries, 54% of whom were women and 46% men. The average age of the staff was 37.6 years. The average length of service in the Organization was 10.3 years, with a turnover of 6.5% in the year.

In 2018, the number of Group employees decreased (-6,229) due, to a large extent, to perimeter variations such as the sale of BBVA Chile (-4,005), completed in the third quarter of the year.

Professional development

The new people management model was consolidated and rolled out in 2018, a process that culminated with the global launch of a new people assessment system. All Group employees were invited to participate in this system in a 360º review, while the group of around 1,400 people who work for projects did so through a model specially designed for them. The calibrated assessments resulting from this process are the basis for building the BBVA talent map, on which the segmentation of the workforce rests, as well as the differentiated management policies.

The combination of the above with the identification and assessment of the existing roles in the Group makes it possible to get to know the professional possibilities of the employees even better, as well as to establish individual development plans, which promote functional mobility and professional growth.

Recruitment and development

In 2018, 18,656 professionals joined the Group, with one of the focuses being the attraction, recruitment and incorporation of new capacities profiles needed by BBVA in its transformation process.

In this manner, in order to be a data-driven organization, in 2018 the first edition of the Young Data Professionals global program was launched. Through this program, 35 recent graduates from universities in Spain, Argentina or Colombia participated in real projects with empowered and multidisciplinary teams, receiving first-level training, both in their specialty as well as in transversal competencies, accompanied at all times by mentors to aid in their development.

As a result of the initiatives involving brand positioning and promotion of the professional opportunities available at BBVA through various channels, 204,148 candidates were attracted. In 2018, BBVA eliminated gender and age as differential fields of the candidates, to avoid discrimination in the selection for both reasons, so the distribution by gender and age of the external candidates cannot be facilitated.

For its part, BBVA reinforced its internal mobility model throughout the year, placing the employee at the center of the process as the protagonist of their own career. In this sense, a new in-house portal was set-up in the Group, where all employees can learn about the opportunities available in the different locations, register for those that they are interested in, and see their progress in the different recruitment processes in which they participate. New policies based on transparency, trust and flexibility are thus brought into existence.

Training

BBVA's training priority in 2018 was to develop a continuous learning culture, necessary to drive the Group's transformation strategy. The people management model positions the employee as the true protagonist of their own development, and for this, the necessary knowledge for the performance of their functions is made available to all employees, with quick access to the training catalog. During 2018, existing training resources were incorporated into the market from platforms, suppliers and speakers of recognized prestige, which made it possible to offer a global catalog of training which included more than 9,000 training actions.

The training contents of 2018 focused on training involving the Group's core values, on regulatory requirements, on the necessary competencies linked to the people management model and, in particular, on the new required capacities: Agile, Design Thinking, Data or Behavioral Economics, among others. This training allowed BBVA to have more than 1,000 Design Ambassadors, more than 50 Agile Coaches and 250 Data Scientists.

The legal requirements of the MiFID II Directive (Markets in Financial Instruments Directive) was another priority focus of training through the different programs designed, and which guarantee the knowledge that employees who distribute information or advise on financial products and services to clients at the European level must possess. In 2018, 14,021 professionals were officially certified in Spain, in the different forms of the European Financial Planner Advisor (DAF/EIP, EFA and EFP).

Regarding training channels, online remains the priority channel and represents 71% of the total training provided in the Group. The main new development in online training in 2018 was the B-Token launch within the Group, a new model that allows access to training through a system of tokens that puts employees in charge of their own development, as they are the ones who choose which training to undertake, as well as how and when to undertake it.

Basic training data (BBVA Group)

| 2018 | 2017 | |

|---|---|---|

| Total investment in training (millions of euros) | 49.5 | 52.2 |

| Investment in training per employee (euros) (1) | 394 | 396 |

| Hours of training per employee (2) | 47.3 | 38.9 |

| Employees who received training (%) | 88 | 84 |

| Satisfaction with the training (rating out of 10) | 9.3 | 8.6 |

| Amounts received from FORCEM for training in Spain (millions of euros) | 3.3 | 3.1 |

- (1) Ratio calculated considering the Group´s workforce at the end of each year (125,627).

- (2) Ratio calculated considering the workforce of BBVA with access to the training.

Training data by professional category and gender (BBVA Group. 2018. Number)

| Number of employees with training | Training hours | |||||

|---|---|---|---|---|---|---|

| Total | Male | Female | Total | Male | Female | |

| Management team (1) | 2,501 | 1,773 | 728 | 118,099 | 80,542 | 37,557 |

| Middle men | 6,599 | 3,947 | 2,652 | 265,789 | 160,147 | 105,643 |

| Specialists | 26,831 | 13,231 | 13,600 | 1,102,703 | 570,189 | 532,514 |

| Sales force | 35,794 | 16,665 | 19,129 | 2,198,559 | 1,020,344 | 1,178,215 |

| Base positions | 37,004 | 14,069 | 22,935 | 1,462,670 | 544,211 | 918,458 |

| Total | 108,729 | 49,685 | 59,044 | 5,147,820 | 2,375,433 | 2,772,387 |

- (1) The management team includes the highest range of the Group's management.

Diversity and inclusion

BBVA considers diversity in its workforce to be one of the key elements it uses to attract and retain the best talent and offer the best possible service to its customers. It is proven that teams made up of people with different ways of thinking, dealing with problems, and making decisions obtain better results.

In terms of gender diversity, women make up 53.9% of the Group's workforce. Women hold 48% of management positions, 30.3% of technology and engineering positions, and 58.1% of business and profit generation positions.

In 2018, initiatives were launched to break down barriers that prevent greater diversity, with a focus placed on facilitating access to positions of responsibility for women. The most important initiatives put in place are:

- Implementation of the Rooney Rule, which requires that 50% of all candidates for management positions be women.

- Training in unconscious biases: various programs, both physical and online, so that team supervisors at BBVA become more aware of their unconscious biases, which mainly harm women and minorities, and learn to neutralize them.

- Improvement in the way in which job offers are drafted so as to make them more attractive for women and minorities.

- Coaching programs for women with high potential to help them assume positions of maximum responsibility and, in turn, for them to support other women in their careers.

BBVA's effort in favor of diversity has led to it being included in the Bloomberg Gender Equality Index, a ranking that includes the 100 best global companies in gender diversity, and in the Equileap Global Report on Gender Equality, which selects the 200 best global companies in terms of gender equality. BBVA is also a signatory of the Diversity Charter at European level and of the United Nations Women's Empowerment Principles.

In Spain, in 2018, BBVA renewed its Company Equality Seal granted by the Ministry of the Presidency, Parliamentary Relations and Equality to companies that are a model for good practices in this area. Likewise, the Equal Treatment and Opportunities Plan signed with the workers' representation allowed for progress in women's access to positions of greater responsibility in the Organization.

In addition, BBVA Spain won the good practices contest for companies in the network. This contest was created by the same Ministry to analyze indicators and evaluation tools, both through the semi-annual monitoring of metrics undertaken by the Equal Treatment and Opportunities Commission and with the participation of the Trade Union Representation, and through the creation of the Diversity Dashboard. This board gives visibility to the metrics by gender, age, training, country of origin, etc. within the Bank itself, through which you can check the degree of diversity of the teams and areas for improvement.

Additionally, BBVA renewed the Family-friendly Company certificate granted by the Más Familia Foundation for the practices and regulations in place at BBVA involving equal treatment and labor, work-family and personal life balance. It was also included in the Variable D2019 report that recognizes the 30 companies in Spain with best practices in diversity and inclusion.

In the United States, BBVA Compass received the highest possible score (100%) in the 2018 Corporate Equality Index, an index that assesses corporate practices and policies for LGBT employees (Lesbian, Gay, Bisexual and Transgender). This index also functions as a national comparison between the main and most influential companies in the country.

In Mexico, BBVA Bancomer conducted the Women Matter study at country level, in order to better understand opportunities for improvement in diversity issues. In line with this, the maternity and paternity program was continued as a supportive measure to help employees through this new stage and to have useful information to generate new initiatives.

In Turkey, Garanti implemented its maternity program by redesigning the process before and after maternity leave. Among other policies to support women who suffer from domestic violence, the Bank maintains a direct helpline for its employees.

Finally, at the end of 2018, all the banks of the Group’s footprint, have protocols for the prevention of sexual harassment, in Spain and the United States for several years, and prepared during the year in the rest of countries.

In particular, in the Bank's protocol in Spain, the Entity and the trade union representatives signing the document expressly state their rejection of any behaviour with sexual nature or connotation that has the purpose or produces the effect of threatening the dignity of a person, particularly when an intimidating, degrading or offensive environment is created, and they commit themselves to the application of this agreement as a solution to prevent, detect, correct and sanction this type of conduct in the company.

Employees by countries and gender (BBVA Group)

| 2018 | 2017 | |||||

|---|---|---|---|---|---|---|

| Number of employees | Male | Female | Number of employees | Male | Female | |

| Spain | 30,338 | 14,930 | 15,408 | 30,584 | 15,097 | 15,487 |

| The United States | 10,984 | 4,566 | 6,418 | 10,928 | 4,470 | 6,458 |

| Mexico | 36,123 | 16,843 | 19,280 | 37,207 | 17,271 | 19,936 |

| Turkey | 21,994 | 9,505 | 12,489 | 22,615 | 9,719 | 12,896 |

| South America | 25,050 | 11,492 | 13,558 | 29,423 | 13,385 | 16,038 |