The BBVA share

Global growth decelerated in 2019 to growth rates slightly below 3% in annual terms in the second half of the year, below the 3.6% of 2018. Increased trade protectionism and geopolitical risks had a negative impact on economic activity, mainly on exports and investment, additionally to the structural slowdown in the Chinese economy and the cyclical moderation of the US and eurozone economies. However, the counter-cyclical policies announced last year, led by central banks, along with the recent reduction in trade tensions between the United States and China and the disappearance of the risk of a disorderly Brexit in the short term, are leading to some stabilization of global growth, based on the relatively strong performance of private consumption supported by the relative strength of labor markets and low inflation. Thus, global growth forecasts stand around 3.2% for both 2019 and 2020.

In terms of monetary policy, the major central banks took more loosening measures last year. In the United States, the Federal Reserve reduced interest rates between July and October by 75 basis points to 1.75%. In the eurozone, the European Central Bank (ECB) announced in September a package of monetary measures to support the economy and the financial system, including: (i) a deposit facility interest rate reduction of ten basis points, leaving them at -0.50%, (ii) the adoption of a phased interest rate system for the previously mentioned deposit facility, (iii) a new debt purchase program of 20 million euros per month, and (iv) an improvement in financing conditions for banks in the ECB's liquidity auctions. The latest signs of growth stabilization contributed to the decision of both monetary authorities to keep interest rates unchanged in recent months, although additional stimulus measures are not ruled out in the event of a further deterioration of the economic environment. In China, in addition to fiscal stimulus decisions and exchange rate depreciation, a cut in reserve requirements for banks was recently announced and base rates have been reduced. Accordingly, interest rates will remain low in major economies, enabling emerging countries to gain room for maneuver.

The main stock market indexes performed positively during 2019. In Europe, the Stoxx Europe 600 index increased by 23.2% in year-on-year terms, with a 5.8% increase in the fourth quarter. In Spain, the rise of the Ibex 35 during 2019 was more moderate (up 11.8% in 2019 and up 3.3 in the fourth quarter). In the United States, the growth rates remain as observed throughout the year and the S&P 500 rose 28.9% in 2019.

With regard to the banking sector indexes, particularly in Europe, its performance was worse than the general market indexes despite the good performance in the fourth quarter. The Stoxx Europe 600 Banks index, which includes banks in the United Kingdom, and the banks index for the Eurozone, the Euro Stoxx Banks, revalued by 8.6% and 11.1%, respectively in 2019. In the United States, the S&P Regional Banks Select Industry Index, on the other hand, increased 24.2% compared to the close of the 2018 financial year.

For its part, the BBVA share price increased by 7.5% during the year, up 4.2% in the fourth quarter, and closing December 2019 at €4.98.

BBVA share evolution

Compared with European indices (Base indice 100=31-12-18)

BBVA

Stoxx Europe 600

Stoxx Banks

Regarding shareholder remuneration, on October 15 BBVA paid a cash interim dividend of €0.10 (gross) per share on account of the 2019 dividend. A cash payment in a gross amount of €0.16 per share, to be paid in April 2020 as final dividend for 2019, is expected to be proposed for the consideration of the competent governing bodies. Therefore, total shareholder remuneration in 2019 stands at €0.26 (gross) per share. This payment is consistent with the shareholder remuneration policy announced by Relevant Event of February 1, 2017.

Shareholder remuneration

(Euros-gross/share)

Cash

Group information

Results

- Generalized increase of recurring revenue items (net interest income and net fees and commissions), which, in constant terms, grow in all business areas.

- Higher contribution from the NTI, which compensates the lower contribution of the other operating income and expenses line.

- Contained growth in the operating expenses and improvement of the efficiency ratio.

- Impairment on financial assets increased 4.3% year-on-year, mainly as a result of higher loan-loss provisions in the United States.

- Following the annual evaluation of its goodwills, BBVA has recorded a goodwill impairment in the United States of €1,318m, mainly due to the evolution of interest rates in the country and the slowdown in the economy. This impact does not affect the tangible net equity, the capital, or the liquidity of BBVA Group and is included in the Corporate Center in the line of other profits and gains (losses) of the income statement.

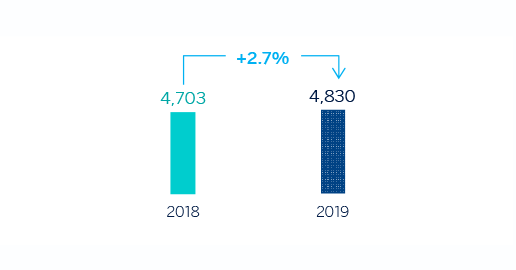

- In 2019, the net attributed profit stood at €3,512m, 35.0% less than in 2018. If BBVA Chile (the results contributed up to its sale and the capital gains generated by the operation) and the goodwill impairment in the United States are excluded from the year-on-year comparison, the Group's net attributable profit grew by 2.7% compared to 2018.

Net attributable profit (Millions of Euros)

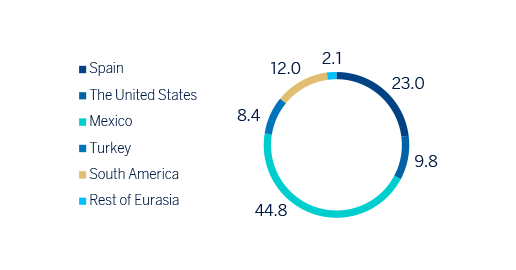

Net attributable profit breakdown (1) (Percentage. 2019)

(1) Excludes the Corporate Center.

Balance sheet and business activity

- The number of loans and advances to customers (gross) registered a growth of 2.2% during 2019, with increases in the business areas of Mexico, and to a lesser extent, in the United States, South America and Rest of Eurasia.

- Good performance of customer funds (+3.8% year-on-year) thanks to the evolution of demand deposits, mutual funds and pension funds.

Solvency

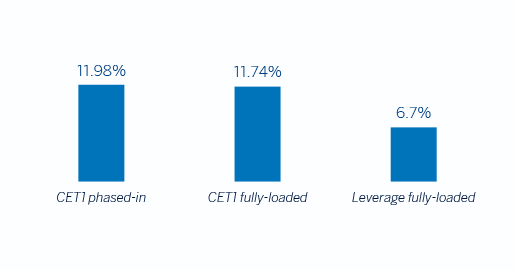

- As a result of the supervisory review and evaluation process (SREP) carried out by the European Central Bank (ECB), BBVA received a communication on December 4, that it is required to maintain, on a consolidated basis and as of January 1, 2020, a CET1 capital ratio of 9.27% and a total capital ratio of 12.77%. On December 31, 2019, the fully-loaded CET1 ratio stood at 11.74%, up 51 basis points in the year (excluding the impact of IFRS 16 standard’s implementation). Thus, BBVA's capital adequacy ratios at the end of 2019 remained above the regulatory requirements applicable as of January 1, 2020.

Capital and leverage ratios (Percentage, 2019)

Risk management

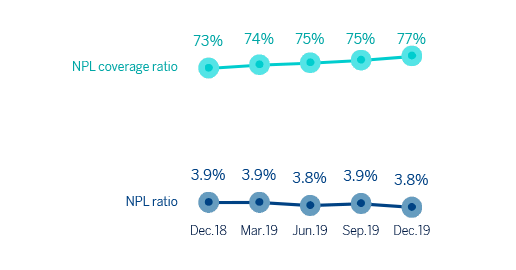

- Positive performance of the risk metrics. Non-performing loans showed a downward trend similar to previous years. The NPL ratio stood at 3.8%, the NPL coverage ratio at 77% and the cost of risk at 1.04%.

NPL and NPL coverage ratios (Percentage)

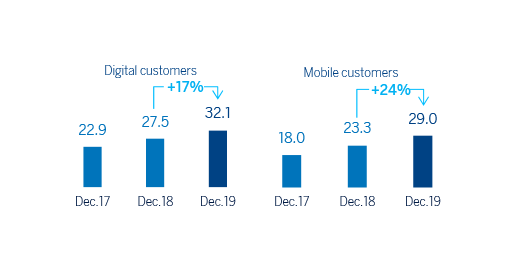

Transformation

Other matters of interest

- During the 2019 financial year, two restatements of consolidated information were made:

- As a result of the implementation of IAS 29 "Financial information in hyperinflationary economies," and in order to make the 2019 information comparable to that of 2018, the balance sheets, the income statements and ratios for the Group's first three quarters of the 2018 financial year and the South American business area, were restated to reflect the impacts of hyperinflation in Argentina in the quarter in which they were generated. This impact was recorded for the first time in the third quarter of 2018, but with accounting effects as of January 1, 2018.

- The amendment to IAS 12 "Income Tax" has meant that the tax impact of the distribution of generated benefits must be recorded in the "Expense or income for taxes on the profits of the continuing activities" of the consolidated income statement for the year, when previously recorded as "Net equity". So, in order for the information to be comparable, the information for the years shown above has been restated in such a way that a payment of €76 million and a charge of €5 million have been recorded in the consolidated profit and loss accounts for the years 2018 and 2017, respectively, against "Less: Interim dividends." This reclassification has no impact on the consolidated net assets.

- On August 7, 2019, BBVA reached an agreement with Banco GNB Paraguay S.A., for the sale of its stake in Banco Bilbao Vizcaya Argentaria Paraguay, S.A. (BBVA Paraguay), which amounts to 100% of its share capital. As a result of the above, all items in BBVA Paraguay's balance sheet have been reclassified into the category of “Non-current assets (liabilities) and disposal groups held for sale”(hereinafter NCA&L).

- On January 1, 2019, IFRS 16 “Leases” entered into force, which requires the lessee to recognize the assets and liabilities arising from the rights and obligations of lease agreements. The main impacts are the recognition of an asset through the right of use and a liability based on future payment obligations. The impact of the first implementation was €3,419m and €3,472m, respectively, resulting in a decrease of 11 basis points of the CET1 capital ratio.

Business areas

Spain

€5,734M*

-3.9%

The United States

€3,223M*

+2.3%

Mexico

€8,029M*

+6.0%

Turkey

€3,590M*

+2.6%

South America

€3,850M*

+14.3%

Rest of Eurasia

€454M*

+9.6%

Spain

€5,734 Mill.*

-3.9%

Millions of euros and year-on-year changes

Highlights

- Growth in consumer, retail and commercial portfolios.

- Net Interest income influenced by the impact of IFRS 16.

- Continued decrease in operating expenses.

- Positive impact of the sale of non-performing and write-off portfolios on loan loss provisions and risk indicators.

Results

Net interest income

3,645-1.4% (1)

Gross income

5,734-3.9% (1)

Operating income

2,480-5.8% (1)

Net attributable profit

1,386-1.0% (1)

Activity (2)

Performing loans and advances to customers under mangement

-1.4%Customers funds under management

+1.2%

Risks

NPL coverage ratio

57%

60%

NPL ratio

5.1%

4.4%

Cost of risk

0.21%

0.12%

DEC 18

DEC 19

(1) Excluding repos.

(2) Year on year changes.

The United States

€3,223 Mill.*

+2.3%

Millions of euros and year-on-year changes at constant exchange rate

Highlights

- Activity impacted by Fed’s interest-rate cuts.

- Good performance of net fees and commissions and NTI.

- Continued improvement of the efficiency ratio.

- Net attributable profit affected by the impairment on financial assets.

Results

Net interest income

2,395-0.2% (1)

Gross income

3,223+2.3% (1)

Operating income

1,257+5.8% (1)

Net attributable profit

590-23.9% (1)

Activity (2)

Performing loans and advances to customers under mangement

+2.1%Customers funds under management

+3.7%

Risks

NPL coverage ratio

85%

101%

NPL ratio

1.3%

1.1%

Cost of risk

0.39%

0.88%

DEC 18

DEC 19

(1) Excluding repos.

(2) Year on year changes at constant exchange rate.

Mexico

€8,029 Mill.*

+6.0%

Millions of euros and year-on-year changes at constant exchange rate

Highlights

- Good performance of the lending activity, boosted by growth in the retail portfolio.

- Positive trend of customer funds especially in demand deposits.

- Net Interest Income growth in line with activity.

- Excellent performance of the NTI.

- Cumulative cost of risk at historically low levels.

Results

Net interest income

6,209+5.9% (1)

Gross income

8,029+6.0% (1)

Operating income

5,384+6.5% (1)

Net attributable profit

2,699+8.2% (1)

Activity (2)

Performing loans and advances to customers under mangement

+7.6%Customers funds under management

+7.0%

Risks

NPL coverage ratio

154%

136%

NPL ratio

2.1%

2.4%

Cost of risk

3.07%

3.01%

DEC 18

DEC 19

(1) Excluding repos.

(2) Year on year changes at constant exchange rate.

Turkey

€3,590 Mill.*

+2.6%

Millions of euros and year-on-year changes at constant exchange rate

Highlights

- In Turkish lira, positive activity performance and relevant improvement in the spread.

- Operating expenses growth below the inflation rate.

- Positive evolution of net fees and commissions and lower requirements for loan-loss provisions on financial assets.

Results

Net interest income

2,814+0.1% (1)

Gross income

3,590+2.6% (1)

Operating income

2,375-0.2% (1)

Net attributable profit

506-0.5% (1)

Activity (2)

Performing loans and advances to customers under mangement

+6.7%Customers funds under management

+16.6%

Risks

NPL coverage ratio

81%

75%

NPL ratio

5.3%

7.0%

Cost of risk

2.44%

2.07%

DEC 18

DEC 19

(1) Excluding repos.

(2) Year on year changes at constant exchange rate.

South America

€3,850 Mill.*

+14.3%

Millions of euros and year-on-year changes at constant exchange rates

Highlights

- Positive evolution of activity in the main countries: Argentina, Colombia and Peru.

- Improved efficiency ratio, supported by the growth in net interest income and the control in operating expenses.

- Greater NTI contribution in the year due to the positive effect derived from Prisma sale in Argentina and the positive contribution of foreign exchange transactions.

- Net attributable profit impacted by Argentina's inflation adjustment.

- Positive contribution of the main countries to the Group’s attributable profit.

Results

Net interest income

3,196+15.2% (1)

Gross income

3,850+14.3% (1)

Operating income

2,276+25.2% (1)

Net attributable profit (3)

721+43.8% (1)

Activity (2)

Performing loans and advances to customers under mangement

+7.0%Customers funds under management

+7.2%

Risks

NPL coverage ratio

97%

100%

NPL ratio

4.3%

4.4%

Cost of risk

1.44%

1.88%

DEC 18

DEC 19

(1) Excluding repos.

(2) Year on year changes at constant exchange rates.

Rest of Eurasia

€454 Mill.*

+9.6%

Millions of euros and year-on-year changes

Highlights

- Good performance in lending, especially in Asia.

- Flattish recurring revenue and positive performance of the NTI.

- Controlled growth of operating expenses.

- Improved risk indicators.

Results

Net interest income

175+0.0% (1)

Gross income

454+9.6% (1)

Operating income

161+26.1% (1)

Net attributable profit

127+32.3% (1)

Activity (2)

Performing loans and advances to customers under mangement

+18.7%Customers funds under management

-1.1%

Risks

NPL coverage ratio

83%

98%

NPL ratio

1.7%

1.2%

Cost of risk

-0.11%

0.02%

DEC 18

DEC 19

(1) Excluding repos.

(2) Year on year changes.

* Gross income

News

Contact

Shareholder attention line

Shareholder attention line912 24 98 21

Subscription service

Subscription service  Shareholder Office

Shareholder Office Contact email

Contact email