The share

The Global economy is being severely affected by the COVID-19 pandemic. Supply, demand and financial factors caused an unprecedented fall in GDP in the first half of 2020. Supported by strong fiscal and monetary policy measures, as well as greater control over the spread of the virus, global growth rebounded more than expected in the third quarter, before slowing down in the fourth, when the number of infections rose again in many regions, mainly in the United States and Europe. As for 2021, the unfavorable evolution of the pandemic is expected to adversely affect activity in the short term, while new fiscal and monetary stimuli, as well as the administering of coronavirus vaccines, are expected to support recovery from mid-year onwards.

Following the massive fiscal and monetary stimuli to support economic activity and reduce financial tensions, government debt has increased across the board and interest rates have been cut, and are now at historical low levels. Additional countercyclical measures may be required. Similarly, a significant reduction in current stimuli is not expected, at least until the recovery takes hold.

Tensions in the financial markets have moderated rapidly since the end of March 2020, following the decisive actions taken by the main central banks and the fiscal packages announced in many countries. In recent months, the markets have shown relative stability and, at certain times, risk-taking movements. Likewise, progress related to the development of COVID-19 vaccines and prospects for economic recovery should pave the way for financial volatility to persist at relatively low levels in general going forward.

BBVA Research estimates that global GDP contracted by around 2.6% in 2020 and will expand by around 5.3% in 2021 and 4.1% in 2022. Activity will recover gradually and heterogeneously among countries. Various epidemiological, financial and geopolitical factors are also contributing to the persistent exceptionally high uncertainty.

With regard to the banking system, in an environment in which much of the economic activity has been at a stand still for several months, the services provided have played an essential role, basically for two reasons: firstly, the banks have ensured the proper functioning of collections and payments for households and companies, thereby contributing to the maintenance of economic activity; secondly, the granting of new lending or the renewal of existing lending has reduced the impact of the economic slowdown on household and business income. The support provided by the banks over the months of lockdown and public guarantees have been essential in softening the impact of the crisis on companies' liquidity and solvency, meaning that banking has become its main source of funding for most companies.

In terms of profitability, European and Spanish banking have deteriorated, primarily because many entities recorded high provisions for impairment on financial assets in the first two quarters of 2020 as a result of the worsening macroeconomic environment following the pandemic outbreak. Pre-pandemic profitability levels remained far from the levels prior to the previous financial crisis. This is in addition to the accumulation of capital since the previous crisis and the very low interest rate environment that we have been experiencing for several years. Nevertheless, the banks are facing this situation from a healthy position and with solvency that has been constantly increasing since the 2008 crisis, with reinforced capital and liquidity buffers and, therefore, with a greater lending capacity.

In a stock market year clearly marked by the evolution of the pandemic, the main stock market indexes have shown a mixed behaviour during the year 2020. In Europe, the Stoxx Europe 600 index fell slightly in the year, down 4.00%, and in Spain the Ibex 35 fell by 15.5%. In The United States, the S&P500 index showed a faster recovery and it was improved by 16.3% in the period.

With regard to the banking sector indexes, its performance was worse than the general market. In Europe, the Stoxx Europe 600 Banks index, which includes the banks in the United Kingdom, and the Euro Stoxx Banks, the Eurozone bank index, fell by 24.5% and 23.7% respectively, meanwhile in The United States, the S&P Regional Banks sectorial index fell by 10.6% in the period.

For its part, the BBVA share price fell by 19.0% during the year, with a lower drop than the drop of the banking sector in Spain (the Ibex 35 index fell by 27.3%) and closed the month of December at €4.04.

BBVA share evolution

Compared with European indexes (Base indice 100=31-12-19)

BBVA

Stoxx Europe 600

Stoxx Banks

The BBVA share and share performance ratios

| 31-12-20 | 31-12-19 | |

|---|---|---|

| Number of shareholders | 879,226 | 874,148 |

| Number of shares issued (millions) | 6,668 | 6,668 |

| Closing price (euros) | 4.04 | 4.98 |

| Book value per share (euros) | 6.70 | 7.32 |

| Tangible book value per share (euros) | 6.05 | 6.27 |

| Market capitalization (millions of euros) | 26,905 | 33,226 |

| Yield (dividend/price; %) (1) | 4.0 | 5.2 |

(1) Calculated by dividing shareholder remuneration over the last twelve months by the closing price of the period.

Regarding shareholder remuneration, the European Central Bank (hereinafter ECB) approved on December 15, 2020, given the persistent uncertainty about the economic impact of the COVID- 19 pandemic, a new recommendation which will be maintained until the end of September 2021 and repeals the previous recommendation. The decision continues the line of recommending to the credit institutions exercise extreme prudence in the distribution of profits, either through the payment of dividends or through conducting share buy-backs, remaining this remuneration below 15% of the cumulative profit for 2019 and 2020 financial years, and in any case, not higher than 20 basis points of the Common Equity Tier 1 (CET1).

Following the aforementioned recommendation, it is expected to be proposed for the consideration of the competent government bodies the intention to pay out €0.059 (gross) per share to its shareholders. The maximum amount distributed will be approximately €393m corresponding to the 15% consolidated profit for 2020 (excluding among others, the goodwill impairment in the United States, the capital gain from corporate operations and the remuneration of additional Tier 1 capital- AT1-), following the recommendation of the ECB.

As of December 31, 2020, the number of BBVA shares was 6,668 billion, and the number of shareholders reached 879,226. By type of investor, 57.18% of the capital belongs to institutional investors and the remaining 42.82% belongs to retail shareholders.

BBVA shares are included on the main stock market indexes, including the Ibex 35, and the Stoxx Europe 600 index, with a weighting of 6.34% and 0.31%, respectively at the closing of December of 2020. They are also included on several sector indexes, including Stoxx Europe 600 Banks, which includes the United Kingdom, with a weighting of 4.63% and the Euro Stoxx Banks index for the eurozone with a weighting of 8.58%.

Finally, BBVA maintains a significant presence on a number of international sustainability indexes or Environmental, Social and Governance (ESG) indexes, which evaluates companies' performance in these areas.

Group information

Results

The BBVA Group generated a net attributable profit of €1,305m during 2020, in a year marked by several factors that influenced the income statement:

- First, the outbreak of the COVID-19 pandemic, the main impacts of which were increased impairment on financial assets and higher provisions.

- Secondly, the goodwill impairment in the United States in the first quarter of 2020, amounting to €2,084m, also as a result of the pandemic. In relation to this business area, the sale agreement reached by the Group is detailed “Other relevant information” section. It should be noted that the Group's results in this report are shown from a management’s business perspective, that is, with the United States business area in continuity. Financial information is being presented to the senior management of the Group with this management’s business perspective, and the fourth quarter 2020 quarterly report includes a conciliation between the management’s business perspective and the Consolidated Financial Statements of the Group.

- Lastly, and to a lesser extent, the execution in the fourth quarter of 2020 of the bancassurance agreement reached with Allianz in Spain, once all required authorizations were received, which has represented a net capital gain of €304m, registered in the line of corporate operations of the Group.

Despite the complexity of the environment, the operating income registered an 11.7% year-on-year increase at constant exchange rates at the end of 2020, driven by the net trading income (NTI) and the operating expenses reduction.

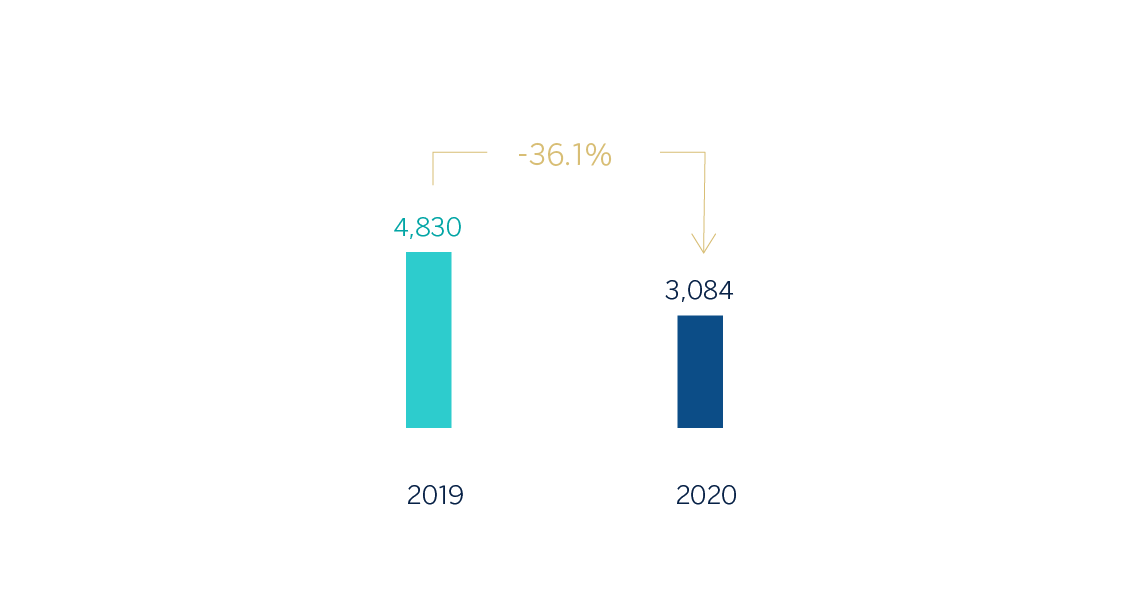

The Group’s adjusted net attributable profit, excluding the goodwill impairment in the United States and the results from corporate operations in 2020, stood at €3,084m, that is a 36.1% below the 2019 result, also excluding the goodwill impairment in the United States in the last quarter of 2019.

Net attributable profit (1)(Millions of Euros)

(1) Excluding the goodwill impairment in the United States, registered in 2019 and 2020 and the net capital gain from the bancassurance operation in 2020.

(1) Excluding the goodwill impairment in the United States, registered in 2019 and 2020 and the net capital gain from the bancassurance operation in 2020.

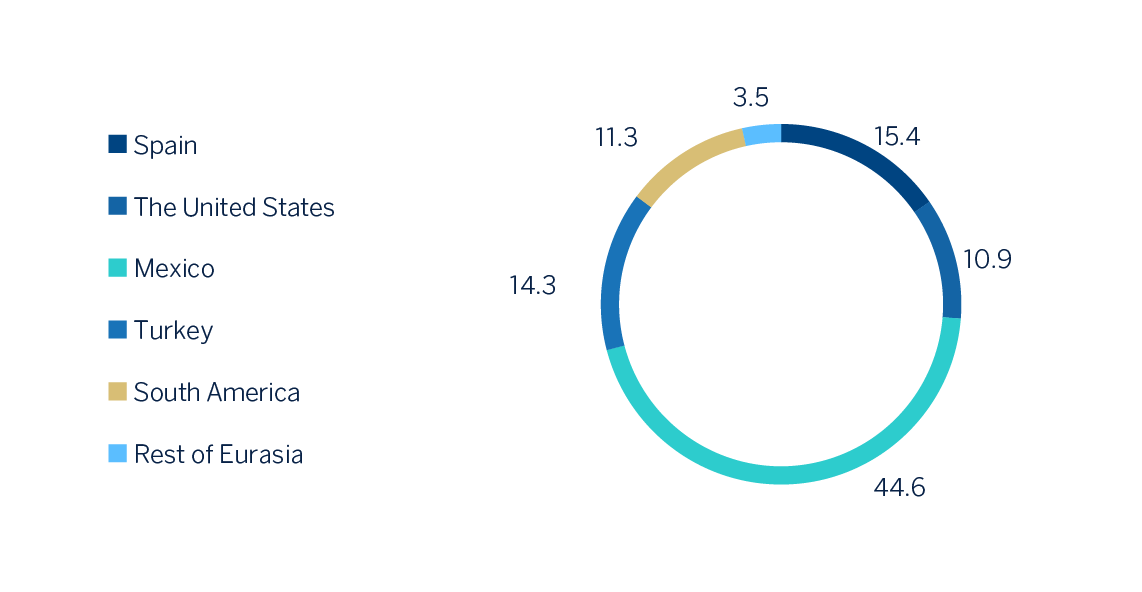

Net attributable profit breakdown (1) (Percentage. 2020)

(1) Excludes the Corporate Center.

(1) Excludes the Corporate Center.

Balance sheet and business activity

- The figure for loans and advances to customers (gross) fell by 4.5% compared to the end of the previous year, with deleveraging in all portfolios in the last quarter of 2020, with the exception of consumer and credit cards.

- Customer funds grew by 3.8% during 2020, mainly as a result of customers placing larger liquidity in demand deposits.

Liquidity and solvency

- The availability of substantial liquidity buffers in each of the geographical areas in which the BBVA Group operates and their management have allowed internal and regulatory ratios to be maintained well above the minimums required.

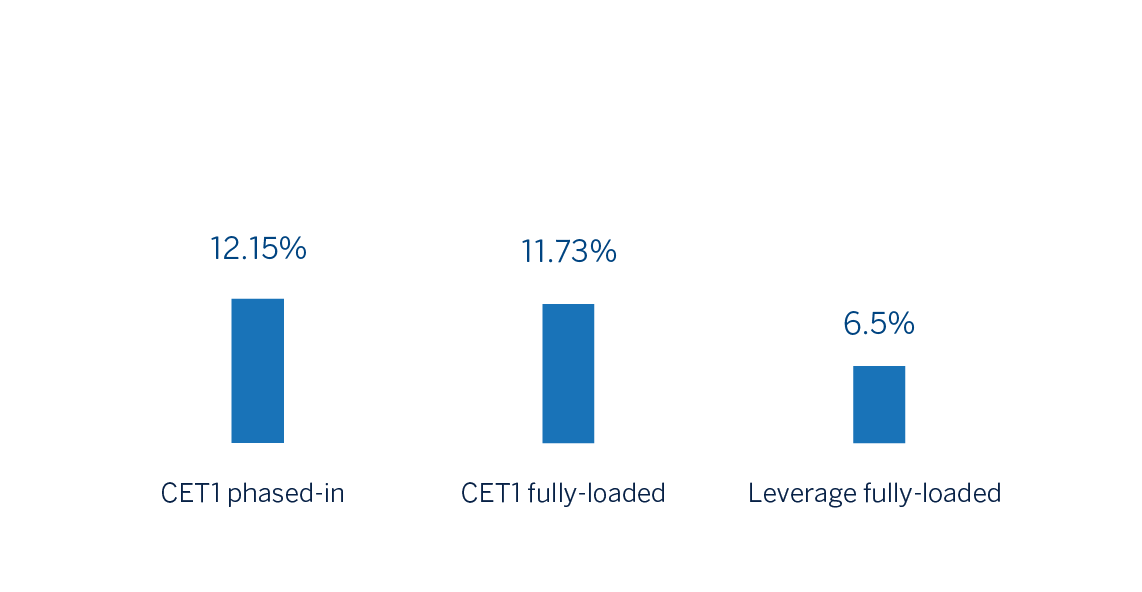

- From 2021 onwards the BBVA Group sets the target to keep the CET1 fully-loaded ratio between 11.5%-12.0%, increasing the distance to the minimum requirement (currently at 8.59%) to 291-341 basis points. As of December 31, 2020, the CET1 fully-loaded ratio stood at 11.73%, already within the target range. This ratio does not include the positive impact of the sale of BBVA USA and other companies in the United States with activities related to its banking business, which according to the current estimate and taking by reference the capital base in 2020, would place the CET1 fully- loaded ratio at 14.58%. Additionally, it does not include the effect of the closing of the sale of BBVA Paraguay, which would have a positive impact of approximately +6 basis points, which will be registered in the first quarter of 2021.

Capital and leverage ratios (Percentage as of 31-12-20)

Risk management

- The calculation of expected credit losses accumulated in 2020 incorporates:

- The update of the forward-looking information in the IFRS 9 models in order to reflect the circumstances created by the COVID-19 pandemic.

- The granting of relief measures in the form of temporary payment deferrals for customers affected by the pandemic, as well as the option to grant lending with a public guarantee facility. In relation to said payments deferrals and in order to mitigate as much as possible the impact of these measures for the Group, due to the high concentration in the time of their maturities, an anticipation plan has been worked out.

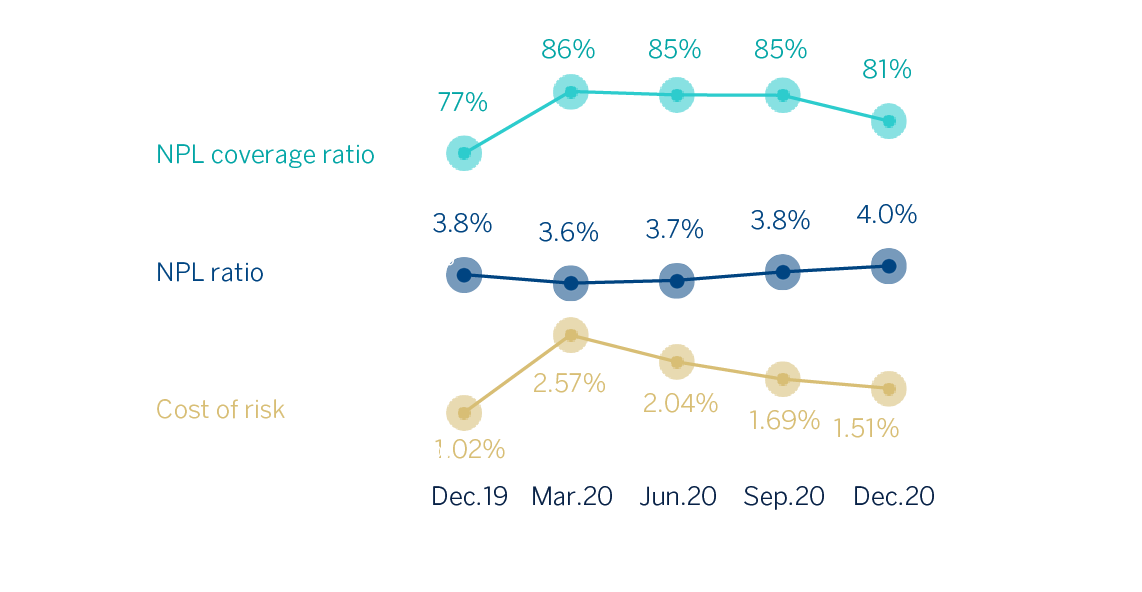

- The behaviour of the main credit risk indicators of the Group at the end of 2020 were:

- The NPL ratio stood at 4.0% at the end of December 2019, 17 basis points above the end of the previous year.

- The NPL coverage ratio closed at 81%, with a relevant improvement compared to the end of 2019.

- The cumulative cost of risk at the end of December stood at 1.51%, after the rebound experienced in the first quarter of 2020 and the subsequent correction throughout the year.

NPL and NPL coverage ratios and cost of risk (Percentage)

Other relevant information

Shareholder remuneration

- Regarding shareholder remuneration, the European Central Bank (hereinafter ECB) approved on December 15, 2020, given the persistent uncertainty about the economic impact of the COVID- 19 pandemic, a new recommendation which will be maintained until the end of September 2021 and repeals the previous recommendation. The decision continues the line of recommending to the credit institutions exercise extreme prudence in the distribution of profits, either through the payment of dividends or through conducting share buy-backs, remaining this remuneration below 15% of the cumulative profit for 2019 and 2020 financial years, and in any case, not higher than 20 basis points of the Common Equity Tier 1 (CET1).

- Following the aforementioned recommendation, it is expected to be proposed for the consideration of the competent government bodies the intention to pay out €0.059 (gross) per share to its shareholders. The maximum amount distributed will be approximately €393m corresponding to the 15% consolidated profit for 2020 (excluding among others, the goodwill impairment in the United States, the capital gain from corporate operations and the remuneration of additional Tier 1 capital- AT1-), following the recommendation of the ECB.

Agreement for the sale of the United States

- The BBVA Group announced, on November 16, 2020, that it has reached an agreement with The PNC Financial Services Group, Inc. (hereinafter PNC) for the sale of 100% of the shareholders' equity of its subsidiary BBVA USA Bancshares, Inc., which in turn owns, all of the shareholders' equity of the bank BBVA USA, as well as other companies of the BBVA Group in the United States with activities related to this banking business. The agreement reached does not include the sale of the institutional business of the BBVA Group developed through its broker dealer BBVA Securities Inc. or the participation in Propel Venture Partners US Fund I, L.P. Likewise, BBVA will continue to develop the wholesale business that it currently conducts through its New York branch. The price of the transaction amounts to USD 11,600m, which will be paid entirely in cash. It is estimated that the operation will generate a positive impact on the CET1 fully-loaded ratio of the BBVA Group of approximately 294 basis points and a net of taxes attributable profit of approximately €580m (calculated with a rate of 1.29 euros/U.S dollar) of which at the end of the financial year 2020, are already collected approximately €300m (corresponding to the results generated by the companies for sale from the signing of the transaction to the end of the year, and that there are recorded in the consolidated Financial Statements on 31 December, 2020) and approximately 9 basis points of positive impact in the CET1 fully-loaded ratio. As usual, the closing of the operation is subject to obtaining regulatory authorizations from the competent authorities and it is estimated that it will take place in mid-2021.

Sale of BBVA Paraguay

- The BBVA Group announced on 22 January 2021 that, once the regulatory authorizations were obtained, it has completed the sale of its direct and indirect stake of 100% of the Shareholders' equity of the Banco Bilbao Vizcaya Argentaria Paraguay S.A. (hereinafter, BBVA Paraguay) to the Banco GNB Paraguay S.A. The total amount received after the closing of the operation amounts to approximately USD 250m and has generated a capital loss, net of taxes, of approximately €9m. Likewise, this transaction will have a positive impact on BBVA Group’s Common Equity Tier 1 (fully-loaded) of approximately +6 basis points. This impact will be reflected in the first quarter of 2021’s capital base of BBVA Group.

Measures COVID-19

From the outset, BBVA has adopted a series of measures to support its main stakeholders. The main business continuity measures taken are:

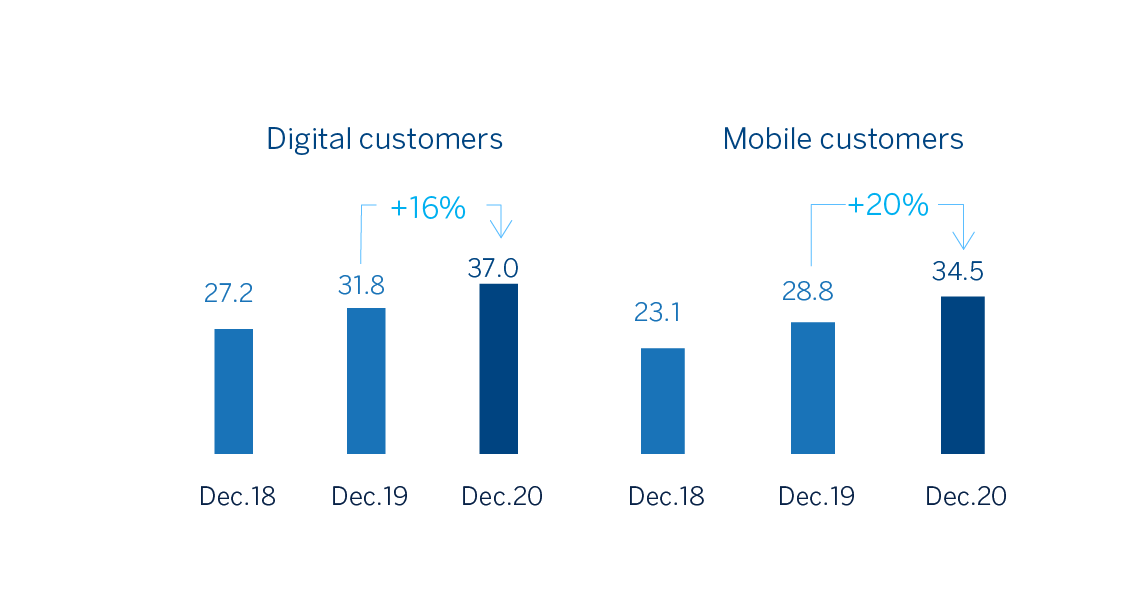

- In order to serve customers, and since financial services are legally considered an essential service in most of the countries in which the Group operates, the branch network remained operational, with dynamic management of the network considering the evolution of the pandemic and activity. In addition, the use of digital channels and remote managers was encouraged. The data indicates that the COVID-19 crisis is accelerating digitization: At Group level, and in cumulative terms, digital sales (measured in units) rebounded in March, and in April it reached 67.4%, with restrictions on the opening of branches in some of the countries where the Group operates, and in December 2020 they stood at 64.0%, which compares very positively with the 59.9% in February. Also at the end of the year, BBVA's digital customers accounted for 63% of the total and customers operating with the bank through their mobile phones accounted for 59% across the entire Group.

Digital and mobile customers (Millions)

- With employees, recommendations from health authorities have been followed, including taking an early stance on promoting working from home. The priority in BBVA's return plan is to protect the health of the employees, customers and society in general. The return plan is being carried out following five principles: 1) cautiousness; 2) gradual return; 3) work shifts; 4) strict hygiene and safety measures; 5) creation of early identification protocols. The crisis is being handled dynamically; adapting the procedures in each geographical area which the Group is present to the current situation, based on the latest data available regarding the evolution of the pandemic, the business and the level of customer service, in addition to the guidelines set by local authorities.

- In terms of cybersecurity, the increase in remote work and digital transactions as a result of the coronavirus crisis has led to an increase in the risk of cyber attacks. To ensure data and corporate information protection, BBVA has established the appropriate measures and continues to strengthen its prevention and monitoring efforts, thus mitigating the possible associated risks.

The banks are a key part of the solution to the COVID-19 crisis. Among other support and responsibility measures, they include:

- BBVA has activated support initiatives with a focus on the most affected customers, regardless of whether they are companies, SMEs, self-employed workers or private individuals, and which includes, among others:

- In Spain, support for SMEs, self-employed workers and companies through credit lines and lines guaranteed by the Spanish Instituto de Crédito Oficial (ICO), grace periods on loans to affected individuals (up to 12 months in residential mortgages for primary residence and up to 6 months in consumer lending), and moratorium of 3 months for citizens in social rental housing under the Social Housing Fund;

- In the United States, flexibility in the repayment of loans for small business and for consumer finance has been extended, and certain fees and commissions for individual customers have been eliminated;

- In Mexico, BBVA granted various supports with personalized characteristics based on the needs of each of the customer segments, offers personalized solutions in a wide variety of products ranging from a lack of 6 months in capital and/or interest in various lending products until the suspension of Point of Sale (POS) fees to support retailers with lower turnover, as well as different support plans aimed at each situation for larger business customers;

- In Turkey, delay until June 2021 of loan repayments, interests and amortizations until December 31, 2020, without any penalty for private customers and extension of up to 6 months in the payment of principal on credits to companies;

- In América del Sur, Argentina has provided micro-SMEs and SMEs with access to credit facilities to purchase teleworking equipment, funding facilities for payroll payments; Colombia has frozen the repayment of loans for individuals and companies for up to six months, and is offering a special working capital facility for companies; and in Peru, various measures were approved in order to support SMEs and customers with consumer loans or credit cards, including rescheduling of debts, extending the payment term.

- To support society in this fight against the COVID-19 pandemic, BBVA donated more than €35m to purchase medical supplies, support vulnerable groups and promote research. This donation was completed with more than €11m contributed by customers and employees.

Business areas

Spain

€5,554M*

-1.8%

The United States

€3,152M*

0.0%

Mexico

€7,017M*

-0.5%

Turkey

€3,573M*

+26.0%

South America

€3,225M*

+1.7%

Rest of Eurasia

€510M*

+12.3%

Spain

€5,554 Mill.*

-1.8%

Year on year changes. Balances as of 31-12-20.

Highlights

- Activity growth driven by corporate and investment banking operations and government support programs.

- Improved efficiency ratio, driven by controlled operating expenses.

- Risk indicators contained.

- Net attributable profit affected by the level of the impairment on financial assets.

Results

Net interest income

3,553-0.4% (2)

Gross income

5,554-1.8% (2)

Operating income

2,515+4.7% (2)

Net attributable profit

606-56.3% (2)

Activity (1)

Performing loans and advances to customers under mangement

+0.8%Customers funds under management

+8.1%

Risks

NPL coverage ratio

60%

67%

NPL ratio

4.4%

4.3%

Cost of risk

0.08%

0.67%

DEC 19

DEC 20

(1) Excluding repos.

(2) Year on year changes.

The United States

€3,152 Mill.*

0.0%

Year on year changes. Balances as of 31-12-20.

Highlights

- Flat lending activity and strong increase in customer deposits in the year.

- The cost of risk favorable evolution continues, with a significant improvement in the quarter.

- Positive evolution of fees and commissions and NTI.

- Net attributable profit impacted by the Fed rate reduction and the significant increase in the impairment on financial assets line.

Results

Net interest income

2,284-2.6% (2)

Gross income

3,1520.0% (2)

Operating income

1,281+4.4% (2)

Net attributable profit

429-25.5% (2)

Activity (1)

Performing loans and advances to customers under mangement

0.0%Customers funds under management

+13.1%

Risks

NPL coverage ratio

101%

84%

NPL ratio

1.1%

2.1%

Cost of risk

0.88%

1.18%

DEC 19

DEC 20

(1) Excluding repos.

(2) Year on year changes at constant exchange rate.

Mexico

€7,017 Mill.*

-0.5%

Year on year changes. Balances as of 31-12-20.

Highlights

- Slight deceleration of activity, impacted by the macroeconomic environment.

- Solid liquidity position.

- Controlled expenses growing significatively under the inflation and the strength of the gross income.

- Net attributable profit affected by the significant increase in the impairment on financial assets line.

Results

Net interest income

5,415-0.7% (1)

Gross income

7,017-0.5% (1)

Operating income

4,677-1.1% (1)

Net attributable profit

1,759-25.8% (1)

Activity (2)

Performing loans and advances to customers under mangement

-1.0%Customers funds under management

+10.0%

Risks

NPL coverage ratio

136%

122%

NPL ratio

2.4%

3.3%

Cost of risk

3.01%

4.02%

DEC 19

DEC 20

(2) Excluding repos.

(1) Year on year changes at constant exchange rate.

Turkey

€3,573 Mill.*

+26.0%

Year on year changes. Balances as of 31-12-20.

Highlights

- Significant credit growth driven by Turkish lira loans. Strong growth in foreign currency deposits.

- Outstanding performance of recurring revenue and efficiency ratio improvement.

- Reduction in the NPL ratio year-to date.

- Double digit growth in the main income statement margins.

Results

Net interest income

2,783+25.2% (2)

Gross income

3,573+26.0% (2)

Operating income

2,544+35.6% (2)

Net attributable profit

563+41.0% (2)

Activity (1)

Performing loans and advances to customers under mangement

+25.9%Customers funds under management

+28.9%

Risks

NPL coverage ratio

75%

80%

NPL ratio

7.0%

6.6%

Cost of risk

2.07%

2.13%

DEC 19

DEC 20

(1) Excluding repos.

(2) Year on year changes at constant exchange rate.

South America

€3,225 Mill.*

+1.7%

Year on year changes. Balances as of 31-12-20.

Highlights

- Activity growth impacted by the support measures from the different governments.

- Year-on-year growth in recurring revenues and year-on-year decline in NTI due to the sale of the stake in Prisma in 2019.

- Contained growth in expenditure, well below the area's average inflation.

- Net attributable profit affected by the increase in the impairment on financial assets line.

Results

Net interest income

2,701+0.9% (2)

Gross income

3,225+1.7% (2)

Operating income

1,853+0.8% (2)

Net attributable profit (3)

446-22.6% (2)

Activity (1)

Performing loans and advances to customers under mangement

+12.6%Customers funds under management

+22.5%

Risks

NPL coverage ratio

100%

110%

NPL ratio

4.4%

4.4%

Cost of risk

1.88%

2.36%

DEC 19

DEC 20

(1) Excluding repos.

(2) Year on year changes at constant exchange rates.

Rest of Eurasia

€510 Mill.*

+12.3%

Year on year changes. Balances as of 31-12-20.

Highlights

- Activity mainly affected by the loans amortizations made during the second half of the year.

- Contained risk indicators.

- Increased recurring income and good performance of NTI.

- Reduction of operating expenses.

Results

Net interest income

214+22.4% (2)

Gross income

510+12.3% (2)

Operating income

225+39.8% (2)

Net attributable profit

137+7.6% (2)

Activity (1)

Performing loans and advances to customers under mangement

-3.8%Customers funds under management

-1.2%

Risks

NPL coverage ratio

98%

100%

NPL ratio

1.2%

1.1%

Cost of risk

0.18%

0.30%

DEC 19

DEC 20

(1) Excluding repos.

(2) Year on year changes.

* Gross income

News

Contact

Shareholder attention line

Shareholder attention line912 24 98 21

Subscription service

Subscription service  Shareholder Office

Shareholder Office Contact email

Contact email