Risk management

Credit risk

BBVA Group's risk metrics continued to perform well along 2018:

- Credit risk decreased by 3.6% throughout 2018 or -0.4% isolating the impact of the sale of BBVA Chile (-1.8% and +1.3%, respectively, at constant exchange rates), mainly due to lower activity in Non Core Real Estate and contraction in Turkey and South America due to the exchange rates evolution. During the fourth quarter credit risk increased by +1.3% (+0.6% at constant exchange rates).

- The balance of non-performing loans decreased throughout 2018 by -16.6% (-11.1% in constant terms), highlighting the good performance of the Banking activity in Spain and Non Core Real Estate. Wholesale customers in Turkey and the United States deteriorated, having a negative impact in its balance of non-performing loans. In the last quarter of 2018 there was a decrease of 3.4% at current exchange rates (-0.5% at constant exchange rates).

- The NPL ratio stood at 3.9% as of December 31, 2018, a reduction of 19 basis points with respect to September 30, 2018 and of 61 basis points throughout the year.

- Loan-loss provisions decreased by 6.2% during the last 12 months (-0.3% at constant exchange rates) whereas the decrease over the quarter amounted to 3.1% (-2.5% at constant exchange rates).

- NPL coverage ratio closed at 73% with an improvement of 812 basis points over the year and 26 basis points in the last 3 months.

- The cumulative cost of risk through December 2018 was 1.01%, +13 basis points higher than the figure for 2017.

Non-performing loans and provisions (Millions of Euros)

Credit risk (1) (Millions of Euros)

| 31-12-18 | 30-09-18 | 30-06-18 (2) | 31-03-18 (2) | 31-12-17 (2) | |

|---|---|---|---|---|---|

| Credit risk | 433,799 | 428,318 | 451,587 | 442,446 | 450,045 |

| Non-performing loans | 17,087 | 17,693 | 19,654 | 19,516 | 20,492 |

| Provisions | 12,493 | 12,890 | 13,954 | 14,180 | 13,319 |

| NPL ratio (%) | 3.9 | 4.1 | 4.4 | 4.4 | 4.6 |

| NPL coverage ratio (%) | 73 | 73 | 71 | 73 | 65 |

- (1) Include gross loans and advances to customers plus guarantees given.

- (2) Figures without considering the classification of non-current assets held for sale.

Non-performing loans evolution (Millions of Euros)

| 4Q 18 (1) | 3Q 18 | 2Q 18 (2) | 1Q 18 (2) | 4Q 17 (2) | |

|---|---|---|---|---|---|

| Beginning balance | 17,693 | 19,654 | 19,516 | 20,492 | 20,932 |

| Additions | 3,005 | 2,168 | 2,596 | 2,065 | 3,757 |

| Recoveries | (1,548) | (1,946) | (1,655) | (1,748) | (2,142) |

| Net variation | 1,456 | 222 | 942 | 317 | 1,616 |

| Write-offs | (1,681) | (1,606) | (863) | (913) | (1,980) |

| Exchange rate differences and other | (382) | (576) | 59 | (380) | (75) |

| Period-end balance | 17,087 | 17,693 | 19,654 | 19,516 | 20,492 |

| Memorandum item: | |||||

| Non-performing loans | 16,348 | 17,045 | 18,627 | 18,569 | 19,753 |

| Non performing guarantees given | 739 | 649 | 1,027 | 947 | 739 |

- (1) Preliminary data.

- (2) Figures without considering the reclassification of non-current assets held for sale.

Structural risks

Liquidity and funding

Management of liquidity and funding in BBVA aims to finance the recurring growth of the banking business at suitable maturities and costs, using a wide range of instruments that provide access to a large number of alternative sources of financing, always in compliance with current regulatory requirements.

Due to its subsidiary-based management model, BBVA Group is one of the few large European banks that follows the MPE resolution strategy ("Multiple Point of Entry"): the parent company sets the liquidity and risk policies, but the subsidiaries are self-sufficient and responsible for the managing their liquidity (taking deposits or accessing the market with their own rating), without funds transfer or financing occurring between either the parent company and the subsidiaries or between different subsidiaries. This principle limits the spread of a liquidity crisis among the Group's different areas and ensures that the cost of liquidity and funding is correctly reflected in the price formation process.

The financial soundness of the Group's banks continues to be based on the funding of lending activity, fundamentally through the use of stable customer funds. During 2018, liquidity conditions remained comfortable across BBVA Group's global footprint:

- In the Eurozone, the liquidity situation is still comfortable, reducing the credit gap and growth in customer deposits.

- In the United States, the liquidity situation is adequate. The credit gap increased during the year due to the dynamism of consumer and commercial credit as well as to the cost-containment strategy for deposits, in an environment of competition in prices and rising rates.

- In Mexico, the liquidity position is sound as the environment has improved after the electoral process and the new commercial agreement with the United States. The credit gap has widened year-to-date due to deposits growing less than lending.

- The liquidity situation in Turkey is stable, showing a reduction in the credit gap as a result of deposits growing faster than lending.

- In South America, the liquidity situation remains comfortable in all geographies. In Argentina, despite the volatility of the markets which has been reducing at the end of the year, the liquidity situation is adequate.

The wholesale funding markets in the geographic areas where the Group operates continued to be stable, with the exception of Turkey where the volatility increased during the third quarter, having stabilized in the fourth quarter with the renewal of the maturities of syndicated loans of different entities.

The main operations carried out by the entities that form part of the BBVA Group during 2018 were:

- BBVA, S.A. completed three operations: an issuance of senior non-preferred debt for €1.5 billion, with a floating coupon at 3-month Euribor plus 60 basis points and a maturity of five years. It also carried out the largest issuance made by a financial institution in the Eurozone of the so-called “green bonds" (€1 billion). It was a 7-year senior non-preferred debt issuance, which made BBVA the first Spanish bank to carry out this type of issuance. The high demand allowed the price to be lowered to mid-swap plus 80 basis points. Finally, BBVA carried out an issuance of preferred securities contingently convertible into newly issued ordinary shares of BBVA (CoCos). This transaction was, for the first time, available to Spanish institutional investors and it was registered with the CNMV for an amount of €1 billion, an annual coupon of 5.875% for the first five years and amortization option from the fifth year. Additionally, it closed a private issuance of Tier 2 subordinated debt for US$300m, with a maturity of 15 years, with a coupon of 5.25%.

- In the United States, BBVA Compass issued in June a senior debt bond for US$1.15 billion in two tranches, both at three years: US$700m at a fixed rate with a reoffer yield of 3.605%, and US$450m at a floating rate of 3-month Libor plus 73 basis points.

- In Mexico, BBVA Bancomer completed an international issuance of subordinated Tier 2 debt of US$1 billion. The instrument was issued at a price equivalent to Treasury bonds plus 265 basis points at a maturity of 15 years, with a ten-year call (BBVA Bancomer 15NC10). In addition, two new Banking Securities Certificates were issued for 7 billion Mexican pesos in two tranches, one of them being the first green bond issued by a private bank in Mexico (3.5 billion Mexican pesos at three years at TIIE28 + 10 basis points).

- In Turkey, Garanti issued the first private bond in emerging markets for US$75m over six years, to support women's entrepreneurship, and renewed the financing of two syndicated loans.

- On the other hand, in South America, in Chile, Forum issued senior debt on the local market for an amount equivalent to €108m and BBVA Peru issued a three-year senior debt in the local market for an aggregate amount of €53m.

As of December 31, 2018, the liquidity coverage ratio (LCR) in BBVA Group remained comfortably above 100% in the period and stood at 127%. For the calculation of the ratio it is assumed that there is no transfer of liquidity among subsidiaries; i.e. no kind of excess liquidity levels in the subsidiaries abroad are considered in the calculation of the consolidated ratio. When considering this excess liquidity levels, the ratio would stand at 154% (27 percentage points above 127%). All the subsidiaries remained comfortably above 100% (Eurozone, 145%; Mexico, 154%; Turkey, 209%; and the United States, 143%).

Foreign exchange

Foreign-exchange risk management of BBVA’s long-term investments, basically stemming from its franchises abroad, aims to preserve the Group's capital adequacy ratios and ensure the stability of its income statement.

The year 2018 was notable for the depreciation against the euro of the Turkish lira (down 25.0%) and the Argentine peso (down 47.8%), while the Mexican peso (+5.2%) and the U.S. Dollar (+4.7%) appreciated. BBVA has maintained its policy of actively hedging its main investments in emerging countries, covering on average between 30% and 50% of the earnings for the year and around 70% of the excess of CET1 capital ratio. In accordance with this policy, the sensitivity of the CET1 ratio to a depreciation of 10% of the main emerging currencies (Mexican peso or Turkish lira) against the euro remains at around a negative two basis points for each of these currencies. In the case of the dollar, the sensitivity is approximately a positive eleven basis points to a depreciation of 10% of the dollar against the euro, as a result of RWAs denominated in U.S. Dollar outside the United States. The coverage level of the expected earnings for 2019, at the closing of January, 2019 is, 85% for Mexico and 30% for Turkey.

Interest rates

The aim of managing interest-rate risk is to maintain a sustained growth of net interest income in the short and medium-term, irrespective of interest-rate fluctuations, while controlling the impact on capital through the valuation of the portfolio of financial assets at fair value with changes reflected in other accumulated comprehensive income.

The Group's banks have fixed-income portfolios to manage their balance-sheet structure. During 2018, the results of this management were satisfactory, with limited risk strategies in all the Group's banks. Their capacity of resilience to market events has allowed them to face the cases of Italy and Turkey.

After the formation of the new government in Italy, the reaction of the market to the budget negotiation process has contributed to the sustained pressure on the Italian debt, however without significant impact on the capital ratio.

In Turkey, an excessive economic growth have given rise to inflationary tensions that, together with the level of current account deficits, have weakened the Turkish Lira. In this context, the Central Bank of Turkey (CBRT) has raised rates to contain the depreciation of the currency. Risk management and bond portfolio with a high component of inflation-linked bonds have stabilized the net interest income and limited impact on the capital ratio.

Finally, it is worth noting the following monetary policies pursued by the different central banks in the main geographical areas where BBVA operates:

- No relevant changes in the Eurozone, where interest rates remain at 0% and the deposit facility rate at -0.40%.

- In the United States the upward trend in interest rates continues. The increases of 25 basis points each in March, June, September and December, left the rate at 2.50%.

- In Mexico, after making two increases in the first half of the year, Banxico raised them again twice in the fourth quarter from 7.75% to 8.25%

- In Turkey, after the increases in the first three quarters of the year, the central bank maintained the average interest rate at 24.00% in the fourth quarter.

- In South America, the monetary authorities of Colombia and Peru have maintained their reference rates flat throughout the quarter, considering in its decision the behavior of inflation next to the established goals, as well as the dynamics of domestic demand. In Argentina, the adopted measures at the beginning of the quarter in terms of monetary policy (increase in reserve requirements and the reference rate) in order not to increase the monetary base and curb inflation which have delivered their results, with a certain deceleration in inflation.

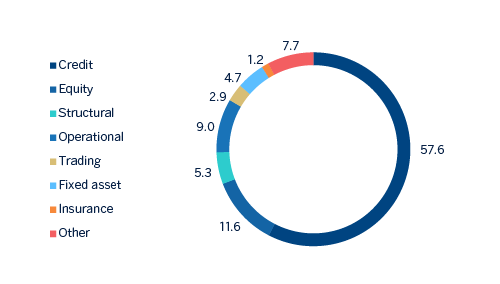

Economic capital

Consumption of economic risk capital (ERC) at the close of December 2018, in consolidated terms, was €31,177m, equivalent to a decline of 0.8% compared to September 2018. Variation within exact time period and at constant exchange rates was down 2.1%, which is mainly explained by structural risk associated with the transfer of the real estate assets of BBVA in Spain to Cerberus Capital Management, L.P. (Cerberus). There were also less relevant decreases in credit risk and equity (goodwill).

Consolidated economic risk capital breakdown

(Percentage as of December 2018)