South America

Highlights

- Growth in lending activity in the first half of the year, with greater dynamism between April and June.

- Reduction in higher-cost customer funds.

- Year-on-year increase in recurring income and NTI and higher adjustment for inflation in Argentina.

- Year-on-year comparison influenced by net attributable profit as a result of the increase in the impairment on financial assets line in 2020 due to the outbreak of the pandemic.

Business activity (1)

(Year-to-date change, at constant exchange

rates)

(1) Excluding repos.

It excludes the balances of BBVA Paraguay

as of 31-12-2020.

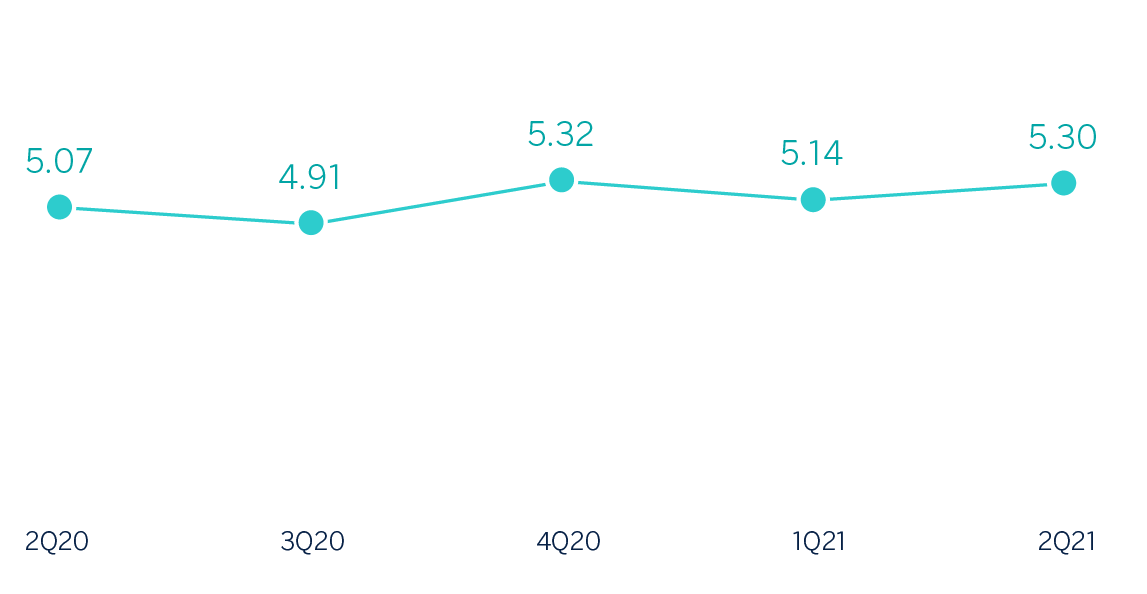

Net interest income/ATAs

(Percentage. Constant exchange rates)

General note: Excluding BBVA Paraguay.

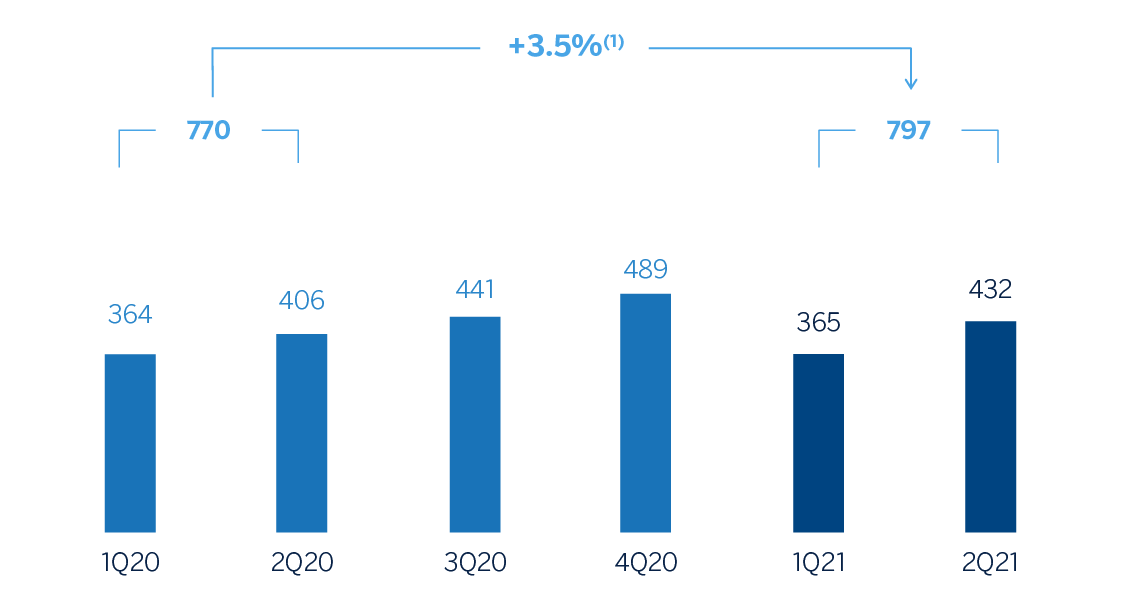

Operating income

(Millions of euros at constant exchange rates)

(1) At current exchange rates: -15.6%.

At constant exchange rates, excluding BBVA

Paraguay in 1Q20 and 2Q20: +6.3%

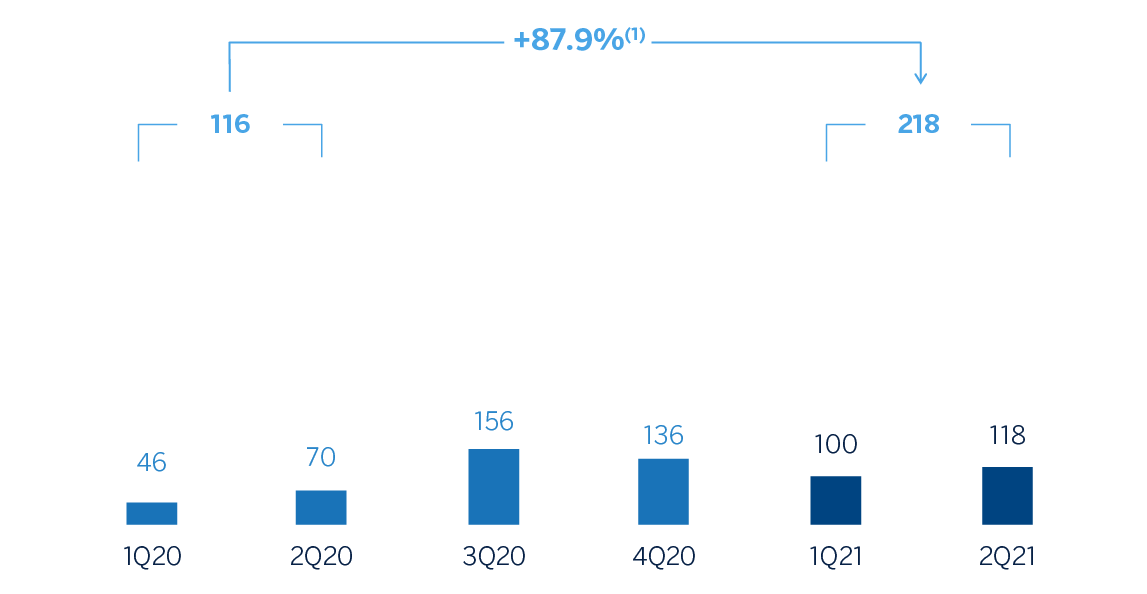

Net attributable profit

(Millions of euros at constant exchange rates)

(1) At current exchange rates:+37.0%.

At constant exchange rate, excluding BBVA

Paraguay in 1Q20 and 2Q20:+110.1%

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1H21 | ∆% | ∆% (1) | ∆% (2) | 1H20 |

|---|---|---|---|---|---|

| Net interest income | 1,328 | (8.0) | 9.8 | 12.3 | 1,443 |

| Net fees and commissions | 267 | 15.0 | 39.8 | 43.2 | 232 |

| Net trading income | 180 | 4.5 | 26.4 | 30.0 | 172 |

| Other operating income and expenses | (295) | 61.3 | 75.0 | 77.6 | (183) |

| Gross income | 1,480 | (11.1) | 7.7 | 10.4 | 1,664 |

| Operating expenses | (683) | (5.1) | 13.0 | 15.6 | (719) |

| Personnel expenses | (332) | (7.0) | 12.0 | 14.8 | (357) |

| Other administrative expenses | (281) | 0.4 | 19.3 | 21.6 | (279) |

| Depreciation | (70) | (15.5) | (3.4) | (1.2) | (83) |

| Operating income | 797 | (15.6) | 3.5 | 6.3 | 945 |

| Impaiment on financial assets not measured at fair value through profit or loss | (343) | (43.0) | (34.4) | (33.5) | (603) |

| Provisions or reversal of provisions and other results | (29) | (35.1) | (24.1) | (23.4) | (45) |

| Profit/(loss) before tax | 424 | 42.9 | 103.6 | 117.7 | 297 |

| Income tax | (131) | 61.1 | 130.1 | 135.4 | (81) |

| Profit/(loss) for the period | 293 | 36.0 | 93.6 | 110.6 | 216 |

| Non-controlling interests | (75) | 33.2 | 112.1 | 112.1 | (57) |

| Net attributable profit/(loss) | 218 | 37.0 | 87.9 | 110.1 | 159 |

| Balance sheets | 30-06-21 | ∆% | ∆% (1) | ∆% (2) | 31-12-20 |

|---|---|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 7,128 | 0.0 | 4.2 | 11.7 | 7,127 |

| Financial assets designated at fair value | 7,266 | (0.9) | 4.2 | 4.3 | 7,329 |

| Of which loans and advances | 233 | 116-4 | 129.3 | 129.3 | 108 |

| Financial assets at amortized cost | 36,356 | (5.7) | (1.6) | 1.5 | 38,549 |

| Of which loans and advances to customers | 32,635 | (2.9) | 1.3 | 4.7 | 33,615 |

| Tangible assets | 799 | (1.1) | 2.0 | 3.0 | 808 |

| Other assets | 1,794 | 10.5 | 15.4 | 17.6 | 1,624 |

| Total assets/liabilities and equity | 53,343 | (3.8) | 0.5 | 3.6 | 55,436 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 1,177 | (11.3) | (6.3) | (6.3) | 1,326 |

| Deposits from central banks and credit institutions | 5,349 | (0.6) | 3.1 | 3.3 | 5,378 |

| Deposits from customers | 35.236 | (4.4) | (0.1) | 3.9 | 36,874 |

| Debt certificates | 3,133 | (4.2) | (0.9) | (0.1) | 3,269 |

| Other liabilities | 3,993 | 4.7 | 9.4 | 11.0 | 3,813 |

| Regulatory capital allocated | 4,456 | (6.7) | (2.4) | 1.0 | 4,776 |

| Relevant business indicators | 30-06-21 | ∆% | ∆% (1) | ∆% (2) | 31-12-20 |

|---|---|---|---|---|---|

| Performing loans and advances to customers under management (3) | 32,749 | (2.9) | 1.4 | 4.7 | 33,719 |

| Non-performing loans | 1,802 | 1.2 | 5.6 | 8.0 | 1,780 |

| Customer deposits under management (4) | 35,236 | (4.5) | (0.1) | 3.9 | 36,886 |

| Off-balance sheet funds (5) | 13,961 | 1.7 | 1.5 | 1.5 | 13,722 |

| Risk-weighted assets | 39,113 | (1.7) | 2.8 | 6.2 | 39,804 |

| Efficiency ratio (%) | 46.1 | 42.6 | |||

| NPL ratio (%) | 4.7 | 4.4 | |||

| NPL coverage ratio (%) | 108 | 110 | |||

| Cost of risk (%) | 1.93 | 2.36 |

- (1) Figures at constant exchange rates.

- (2) Figures at constant exchange rates excluding BBVA Paraguay.

- (3) Excluding repos.

- (4) Excluding repos and including specific marketable debt securities.

- (5) Includes mutual funds, pension funds and other off-balance sheet funds.

South America. Data per country (Millions of euros)

| Operating income | Net attributable profit/(loss) | |||||||

|---|---|---|---|---|---|---|---|---|

| Country | 1H 2021 | ∆% | ∆% (1) | 1H 2020 | 1H 2021 | ∆% | ∆% (1) | 1H 2020 |

| Argentina | 93 | (51.0) | n.s. | 190 | 15 | (64.3) | n.s. | 43 |

| Colombia | 289 | (2.1) | 5.2 | 295 | 106 | 120.3 | 136.7 | 48 |

| Peru | 343 | (2.9) | 15.9 | 353 | 55 | 69.7 | 102.6 | 32 |

| Other countries (2) | 72 | (32.4) | (28.8) | 107 | 42 | 16.7 | 30.0 | 36 |

| Total | 797 | (15.6) | 3.5 | 945 | 218 | 37.0 | 87.9 | 159 |

- (1) Figures at constant exchange rates.

- (2) Bolivia, Chile (Forum), Paraguay in 2020, Uruguay and Venezuela. Additionally, it includes eliminations and other charges.

South America. Relevant business indicators per country (Millions of euros)

| Argentina | Colombia | Peru | ||||

|---|---|---|---|---|---|---|

| 30-06-21 | 31-12-20 | 30-06-21 | 31-12-20 | 30-06-21 | 31-12-20 | |

| Performing loans and advances to customers under management (1) (2) | 2,775 | 2,553 | 11,400 | 11,022 | 15,393 | 14,558 |

| Non-performing loans and guarantees given (1) | 78 | 48 | 680 | 639 | 951 | 871 |

| Customer deposits under management (1) (3) | 5,349 | 4,196 | 12,157 | 11,444 | 14,251 | 15,274 |

| Off-balance sheet funds (1) (4) | 1,346 | 880 | 982 | 1,478 | 1,906 | 2,068 |

| Risk-weighted assets | 5,548 | 5,685 | 12,951 | 13,096 | 16,469 | 15,845 |

| Efficiency ratio (%) | 70.4 | 53.6 | 35.3 | 35.2 | 37.0 | 37.7 |

| NPL ratio (%) | 2.7 | 1.8 | 5.3 | 5.2 | 4.9 | 4.5 |

| NPL coverage ratio (%) | 176 | 241 | 110 | 113 | 101 | 101 |

| Cost of risk (%) | 2.76 | 3.24 | 2.27 | 2.64 | 1.85 | 2.13 |

- (1) Figures at constant exchange rates.

- (2) Excluding repos.

- (3) Excluding repos and including specific marketable debt securities.

- (4) Includes mutual funds.

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. These rates, together with the changes at current exchange rates, can be found in the attached tables of the financial statements and relevant business indicators. The information for this business area includes BBVA Paraguay with regard to data on the results, activity, balance sheet and relevant business indicators for 2020, but does not include Paraguay for 2021, as the sale agreement materialized in January of that year. To facilitate an homogeneous comparison, the attached tables include a column at constant exchange rates that does not take BBVA Paraguay into account. All comments for this area also exclude BBVA Paraguay.

Activity and results

The most relevant aspects related to the area's activity during the first half of 2021 were:

- Lending activity (performing loans under management) showed a variation of +4.7% compared to December 2020, with greater dynamism between April and June (+3.8%) compared to the first quarter of 2021 (+0.9%), due to the seasonal nature of summer vacations in some countries of the area. By portfolio, the wholesale portfolio recorded an increase of +5.8% and the retail portfolio closed out with growth of +3.7% in the first half of 2021.

- With regard to asset quality, the NPL ratio stood at 4.7%, with an increase compared to the close of December 2020, and the NPL coverage ratio fell to 108% in the same period.

- Customer funds under management increased by (+3.2%) compared to December 2020 closing balances. Deposits from customers under management increased by 3.9%, despite efforts in some countries to reduce higher-cost current and savings accounts, in an environment whereby the Group's liquidity situation throughout the region is adequate. Off-balance sheet funds increased +1.5% in the area as a whole between January and June 2021.

South America generated a cumulative net attributable profit of €218m between January and June 2021, representing year-on-year variation of +110.1%, mainly due to the improved performance of recurring income and NTI between January and June 2021 (+17.8%), despite COVID-19 outbreaks and restrictions on mobility. All this in a comparison that is also influenced by the significant provision for impairment on financial assets in the first half of 2020, caused by the worsening macroeconomic scenario following the outbreak of the pandemic in March 2020. The cumulative impact of inflation in Argentina on the area's net attributable profit at the close of June 2021 stood at a loss of €-97m, compared to a cumulative loss of €-58m at the close of June 2020.

The key countries for the business area, Argentina, Colombia and Peru performed as follows in the first half of 2021 in terms of activity and results:

Argentina

- Lending activity increased 8.7% compared to the close of December 2020, a figure that is below inflation, with growth in the retail segment (+12.5%), namely credit cards (+8.9%). The NPL ratio increased in the quarter to 2.7% and the NPL coverage ratio fell to 176% respectively, as of June 30, 2021.

- Balance sheet funds continued to grow (+27.5% in the first half 2021), with a particular focus on wholesale liabilities during the second quarter, while off-balance sheet funds increased 53.0% compared to December 2020.

- Net attributable profit stood at €15m, thanks to the good performance in recurring income, a higher contribution in NTI due to foreign exchange derivative transactions, as well as higher operating expenses and a higher rate of inflation compared to the first half of 2020.

Colombia

- Lending activity showed growth of 3.4% compared to 2020 year-end thanks to the performance of wholesale portfolios (+4.8%) and retail portfolios (+2.7%). In terms of asset quality, the NPL ratio and NPL coverage ratio remained stable at 5.3% and 110% respectively at the close of June 2021.

- Deposits from customers under management increased by 6.2%, compared to 2020 year-end, with a significant reduction in the cost of said deposits. Off-balance sheet funds closed 33.6% down in the six-month period due to the volatility of investments made by institutional customers.

- Net attributable profit stood at €106m, significantly above (+136.7% year-on-year) the €48m posted between January and June 2020, thanks to, both the strength of operating income, which increased by 5.2% due to higher recurring income, and lower provisions for impairment on financial assets compared to the same period last year, when they increased significantly due to the pandemic outbreak.

Peru

- Lending activity closed out the first half posting favorable growth of +5.7% compared to 2020 year-end, mainly due to the performance of mortgages, consumer finance and growth in corporate lending (+7.1% compared to 2020 year-end), which captured liquidity in order to weather political uncertainty caused by the electoral process. The NPL ratio increased slightly in the second quarter of 2021 due to the deterioration of certain retail portfolios and stood at 4.9%. The NPL coverage ratio remained stable at 101%.

- Deposits from customers under management fell -6.7% in the first six months of 2021, with a decrease in time deposits to reduce their costs. Off-balance sheet funds also declined compared to the close of December 2020 (-7.8%).

- Recurring income grew 8.4% compared to the first half of 2020, thanks to good performance in fees (+37.4% in the same period of time), particularly in fees for cards due to increased operations at retailers. Meanwhile, NTI increased by 46.9%, as a result of more foreign exchange transactions and good performance in derivative transactions. Provisions for impairment on financial assets saw a year-on-year decrease (-25.3%), as a result of significant provisions made in the first half of 2020 following the pandemic outbreak in March 2020. As a result, net attributable profit stood at €55m, 102.6% higher than the figure posted between January and June 2020.