Spain

Highlights

- Growth in lending activity despite the usual seasonality in the first quarter of the year

- Favorable year-on-year evolution of the main margins

- Significant improvement in the efficiency ratio

- Lower impairment on financial assets and good performance of risk indicators

Business activity (1)

(VARIATION COMPARED TO 31-12-21)

(1) Excluding repos.

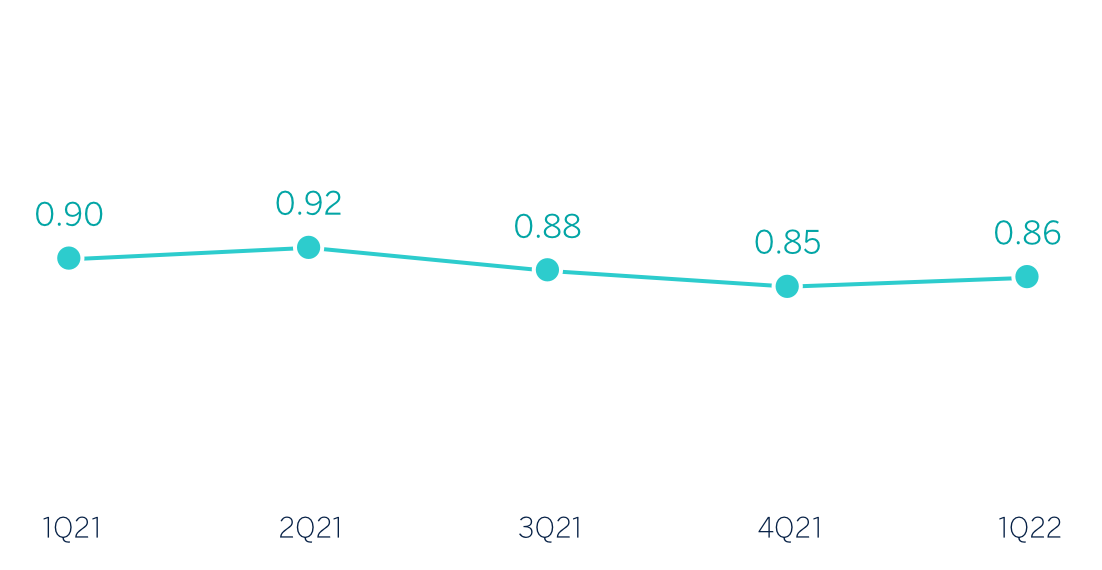

Net interest income/AVERAGE TOTAL ASSETS

(Percentage)

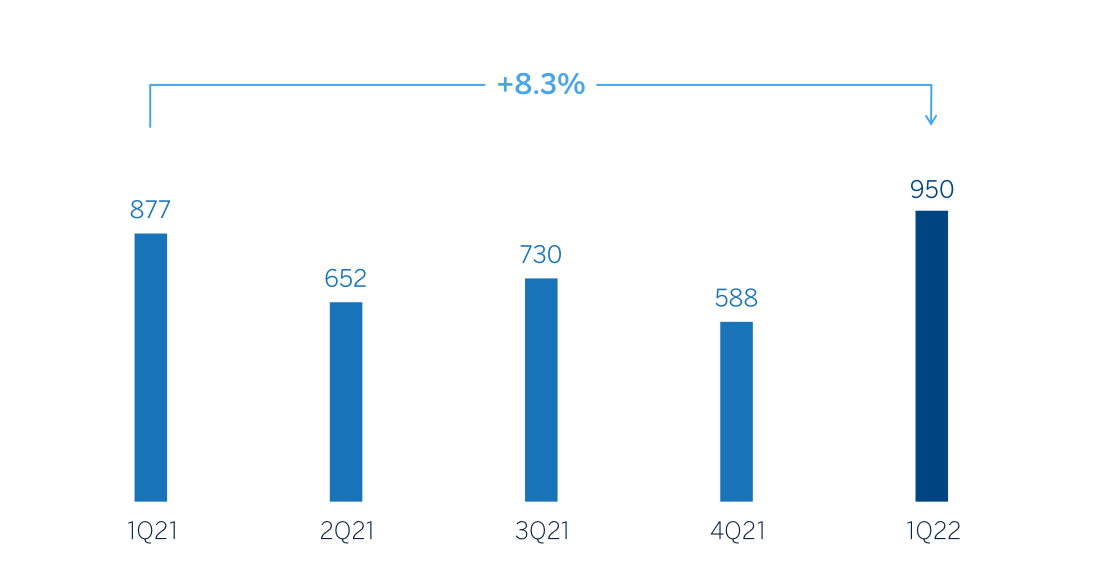

Operating income (Millions of euros)

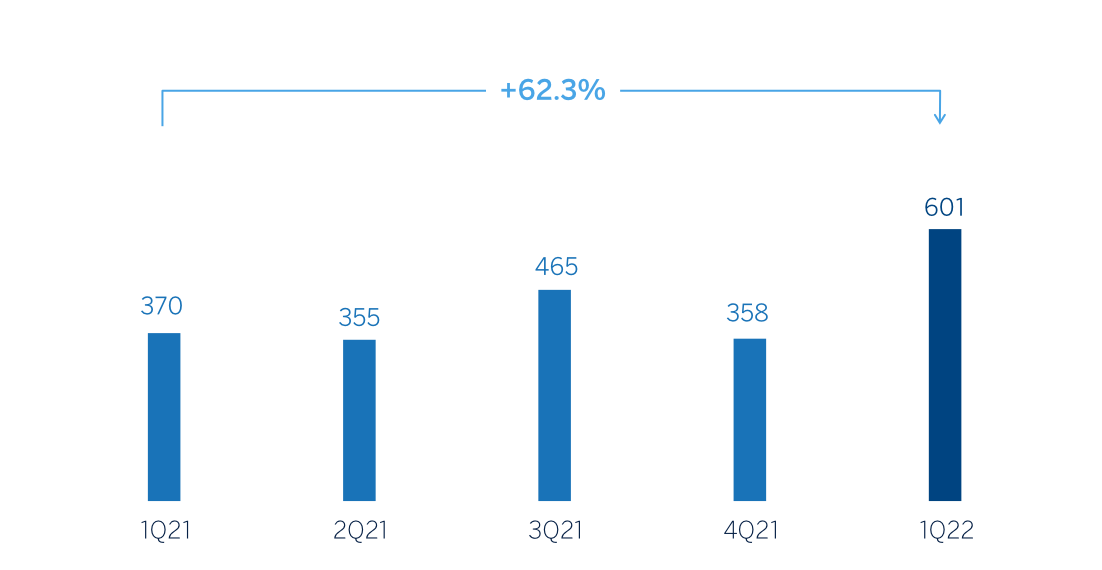

Net attributable profit (LOSS) (Millions of euros)

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1Q22 | ∆% | 1Q21 (1) |

|---|---|---|---|

| Net interest income | 859 | (0.8) | 866 |

| Net fees and commissions | 536 | 5.4 | 509 |

| Net trading income | 190 | 1.3 | 187 |

| Other operating income and expenses | 79 | 10.9 | 71 |

| Of which: insurance activities (2) | 96 | 7.1 | 90 |

| Gross income | 1,663 | 1.9 | 1,633 |

| Operating expenses | (714) | (5.6) | (756) |

| Personnel expenses | (383) | (10.5) | (428) |

| Other administrative expenses | (226) | 3.7 | (218) |

| Depreciation | (105) | (5.0) | (110) |

| Operating income | 950 | 8.3 | 877 |

| Impairment on financial assets not measured at fair value through profit or loss | (89) | (51.7) | (185) |

| Provisions or reversal of provisions and other results | (19) | (89.5) | (186) |

| Profit (loss) before tax | 841 | 66.1 | 506 |

| Income tax | (239) | 76.4 | (136) |

| Profit (loss) for the period | 602 | 62.3 | 371 |

| Non-controlling interests | (1) | 38.2 | (1) |

| Net attributable profit (loss) | 601 | 62.3 | 370 |

- (1) Restated balances. For more information, please refer to the “Business Areas” section.

- (2) Includes mutual funds, customer portfolios and pension funds.

| Balance sheets | 31-03-22 | ∆% | 31-12-21 |

|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 28,567 | 8.3 | 26,386 |

| Financial assets designated at fair value | 136,353 | (6.3) | 145,546 |

| Of which: Loans and advances | 42,486 | (16.1) | 50,633 |

| Financial assets at amortized cost | 199,699 | -0.0/td> | 199,646 |

| Of which: Loans and advances to customers | 171,950 | 0.5 | 171,081 |

| Inter-area positions | 37,242 | 9.6 | 33,972 |

| Tangible assets | 2,508 | (1.0) | 2,534 |

| Other assets | 5,675 | 6.2 | 5,346 |

| Total assets/liabilities and equity | 410,045 | (0.8) | 413,430 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 75,724 | (6.9) | 81,376 |

| Deposits from central banks and credit institutions | 59,876 | 9.3 | 54,759 |

| Deposits from customers | 206,451 | (0.1) | 206,663 |

| Debt certificates | 36,027 | (5.7) | 38,224 |

| Inter-area positions | - | - | - |

| Other liabilities | 17,622 | (4.3) | 18,406 |

| Regulatory capital allocated | 14,345 | 2.4 | 14,002 |

| Relevant business indicators | 31-03-22 | ∆% | 31-12-21 |

|---|---|---|---|

| Performing loans and advances to customers under management (1) | 169,095 | 0.5 | 168,235 |

| Non-performing loans | 8,436 | (0.2) | 8.450 |

| Customer deposits under management (1) | 205,927 | 0.0 | 205,908 |

| Off-balance sheet funds (2) | 90,828 | (3.7) | 94,095 |

| Risk-weighted assets | 109,623 | (3.7) | 113,797 |

| Efficiency ratio (%) | 42.9 | 51.7 | |

| NPL ratio (%) | 4.2 | 4.2 | |

| NPL coverage ratio (%) | 61 | 62 | |

| Cost of risk (%) | 0.17 | 0.30 |

- (1) Excluding repos.

- (2) Includes mutual funds, customer portfolios and pension funds.

Macro and industry trends

The economic recovery continued in the last months of 2021 and the first months of 2022, despite the negative impact on activity of the increased infections caused by new variants of the COVID-19. According to official estimates, after a fall of 10.8% in 2020, the GDP grew 5.1% in 2021. Inflation continued to accelerate (in March 2022 it stood at 9.8%), driven mainly by energy prices. According to BBVA Research, in a context of high uncertainty, mainly due to the war between Ukraine and Russia, GDP growth could decelerate this year to around 4.1%, a lower level than previously expected (5.5%), although still relatively high, supported by the growing use of resources from European funds. Given the recent rise in commodity prices, particularly energy prices, inflation will likely remain high this year (around 7.0%, on average).

With regard to the banking system, with data as of the end of January 2022, lending volumes to the private sector recorded a decline of 0.1% year-on-year, also after a decline of 0.1% in 2021 as a whole. The NPL ratio remained contained at 4.32% in January 2022 after rising 3 basis points since December 2021 due to the slight decrease in credit volume in January. In 2021 as a whole, the NPL ratio fell 22 basis points to 4.29%. In addition, it should be noted that the system maintained comfortable levels of solvency and liquidity.

Activity

The most relevant aspects related to the area's activity during 2022 were:

- Lending activity (performing loans under management) was higher than at the end of 2021 (+0.5%), due largely to the growth in business segments, especially loans to SMEs (+4.3%), which compensated for the usual seasonal slowdown in credit cards (+0.7%, including consumer loans) and lower activity with public administrations (-1.9%).

- With regard to asset quality, the non-performing loan ratio decreased by 4 basis points in the quarter to 4.2% mainly due to the good level of recoveries, supported by the reclassification of moratoriums, following months of good payment behavior after the grace period expired. In terms of the NPL coverage ratio, it remained stable in the quarter, reaching 61%.

- Total customer funds registered a variation of -1.1% compared to 2021 year-end. In the quarter, the off-balance sheet funds recorded a decrease of 3.5%, mainly due to the negative effect of the markets evolution. For its part, the balance of customer deposits under management remained stable between January and March as the increase in deposits held by retail customers compensated for the decrease in balances held with public administrations. By product, demand deposits grew by 0.9%, compensating for the drop in time deposits (-9.2%).

Results

Spain generated a net attributable profit of €601m during the first quarter of 2022, up 62.3% from the result achieved between January and March of the previous year, due to the good performance of gross income, driven by commissions, the significant reduction in personnel expenses, as well as lower write-offs and provisions.

The most notable aspects of the year-on-year changes in the area's income statement at the end of March 2022 were:

- Net interest income registered a slight decrease of 0.8%, mainly due to the effect of the low interest rates' environment on the stock of loans, which was partially offset by lower financing costs.

- Fees and commissions showed a positive performance (+5.4% year-on-year), mainly favored by a greater contribution from banking services and revenues associated with asset management and insurance.

- NTI at the end of March 2022 was 1.3% higher than in the same period of the previous year, due in part to the greater contribution of the Global Markets area.

- The other operating income and expenses line compares positively to the previous year, favored by the better performance of the insurance business.

- Operating expenses were lower than at the end of the first quarter of 2021 (-5.6% in year-on-year terms), mainly due to lower personnel expenses as a result of the staff decrease.

- Due to the gross income growth and the declined expenses, the efficiency ratio stood at 42.9%, representing a significant improvement compared to the 46.3% recorded at the end of March 2021.

- Impairment on financial assets was 51.7% lower compared to the first quarter of 2021, due to the good performance of the underlying asset supported by some non-recurring items recorded in the first quarter of 2022. As a result, the accumulated cost of risk at the end of March 2021 stood at 0.17%.

- The provisions and other results line closed the first quarter of the year at €-19m, which positively compares with the last year, mainly due to lower legal and labor contingencies, higher results from real estate assets and lower provisions for off- balance sheet risks.