Risk management

Credit risk

BBVA Group's risk metrics have continued to perform positively throughout the year :

- Credit risk fell by 2.1% in the last quarter, and by 3.9% since the end of 2016 (down 0.4% and up 0.1%, respectively, at constant exchange rates). The key factors are: ongoing deleveraging in Spain (partly explained by the decline in the Non Core Real Estate area), Turkey (mainly due to negative exchange rate effects) and, to a lesser degree, the United States (also due to the exchange rate, given that at constant exchange rates there was a slight increase in activity over the quarter). The rest of the geographical areas reported growth (also in constant exchange rate terms). South America posted a decline from the end of December 2016, which is also explained by the unfavorable effect of exchange rates.

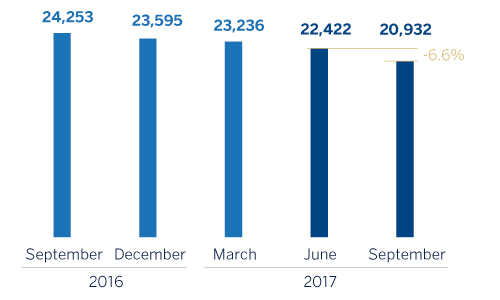

- Non-performing loans continue declining, falling by 6.6% over the quarter and 11.3% relative to December 2016. Almost the entire geographic footprint performed positively, especially Spain.

- The Group’s NPL ratio continues to improve (down 22 basis points over the last three months and 37 basis points since December 2016) to 4.5% at the close of September 2017, driven by the decline in non-performing loans.

- Coverage provisions also fell, albeit by less than non-performing loans: down 5.3% on June (down 3.8% excluding exchange-rate effects) and 9.2% lower than December 2016.

- The NPL coverage ratio closed the first nine months at 72%, an improvement of 105 basis points over the last three months and 162 basis points since December 2016.

- Finally, the cumulative cost of risk to September stood at 0.93%, in line with the first half of 2017 (0.92%) and 9 percentage points above the overall figure for 2016 (0.84%).

Non-performing loans (Million euros)

Credit risks (1) (Million euros)

| 30-09-17 | 30-06-17 | 31-12-16 | 30-09-16 | 30-09-16 | |

|---|---|---|---|---|---|

| Non-performing loans and guarantees given | 20,932 | 22,422 | 23,236 | 23,595 | 24,253 |

| Credit risks | 461,794 | 471,548 | 480,517 | 480,720 | 472,521 |

| Provisions | 15,042 | 15,878 | 16,385 | 16,573 | 17,397 |

| NPL ratio (%) | 4.5 | 4.8 | 4.8 | 4.9 | 5.1 |

| NPL coverage ratio (%) | 72 | 71 | 71 | 70 | 72 |

- (1) Include gross loans and advances to customers plus guarantees given.

Non-performing loans evolution (Million euros)

| 3Q 17(1) | 1Q 17 | 4Q 16 | 3Q 16 | 3Q 16 | |

|---|---|---|---|---|---|

| Beginning balance | 22,422 | 23,236 | 23,595 | 24,253 | 24,834 |

| Entries | 2,250 | 2,525 | 2,490 | 3,000 | 2,588 |

| Recoveries | (1,999) | (1,930) | (1,698) | (2,141) | (1,784) |

| Net variation | 251 | 595 | 792 | 859 | 804 |

| Write-offs | (1,575) | (1,070) | (1,132) | (1,403) | (1,220) |

| Exchange rate differences and other | (165) | (340) | (18) | (115) | (165) |

| Period-end balance | 20,932 | 22,422 | 23,236 | 23,595 | 24,253 |

| Memorandum item: | |||||

| Non-performing loans | 20,222 | 21,730 | 22,572 | 22,915 | 23,589 |

| Non-performing guarantees given | 710 | 691 | 664 | 680 | 665 |

- (1) Preliminary data.

Structural risks

Liquidity and funding

Management of liquidity and funding in BBVA aims to finance the recurring growth of the banking business at suitable maturities and costs, using a wide range of instruments that provide access to a large number of alternative sources of finance, always in compliance with current regulatory requirements.

A core principle in BBVA’s management of the Group’s liquidity and funding is the financial independence of its banking subsidiaries abroad. This principle prevents the propagation of a liquidity crisis among the Group’s different areas and ensures that the cost of liquidity is correctly reflected in the price formation process.

In the first nine months of 2017, liquidity and funding conditions have remained comfortable across BBVA Group’s global footprint:

- The financial soundness of the Group’s banks continues to be based on the funding of lending activity, fundamentally through the use of stable customer funds.

- Activity both on the euro balance sheet and in Mexico has continued to generate liquidity, as deposits have shown a positive trend that has led to a narrowing of the credit gap.

- In the United States, the credit gap has widened in the first nine months of the year because of the area’s deliberate strategy to control the cost of deposits.

- Comfortable liquidity situation in Turkey, due to the maintenance of good market conditions in the third quarter, with a stable credit gap.

- In South America, the liquidity situation remains comfortable, allowing a reduction of the growth of wholesale deposits to match lending activity.

- In addition, in the third quarter BBVA S.A. successfully completed its first issuance of €1.5 billion in senior non-preferred (SNP) debt. In total, over the first nine months of 2017, BBVA S.A. has accessed the wholesale funding markets for a total of €5 billion, using senior debt (€1 billion in the first quarter and €1.5 billion in the second), Tier 2 debt (€1 billion in the first quarter) and SNP debt (€1.5 billion). A number of private issuance transactions of Tier 2 securities have also been closed for around €500m, and one additional Tier 1 issue of €500m, all in the first half of the year.

- The long-term wholesale funding markets have remained stable in the other geographical areas where the Group operates.

- In Turkey, Garanti’s securities issues continue to strengthen its balance-sheet structure. Of note are the following: in the first quarter, senior debt for USD 500m; in the second quarter, subordinate debt for USD 750m, collateralized bonds for an equivalent of €126m, and renewal of the syndicated loan; and in the third quarter, collateralized bonds for an equivalent of €71m.

- In the United States, BBVA Compass returned to the markets in the second quarter with a 5-year senior debt issue of USD 750m.

- In Mexico, BBVA Bancomer has carried out two local senior debt issues for a total of €326m with maturities of 3 and 5 years.

- In South America, BBVA Chile has also made a number of senior issues with maturities ranging from 4 to 10 years on the local market for an equivalent of €558m. In Peru, BBVA Continental has issued €52m on the market with a maturity of 3 years.

- Short-term funding has continued to perform positively, in a context marked by a high level of liquidity.

- BBVA’s LCR liquidity coverage ratio continues at levels of over 100%, clearly higher than demanded by regulations (over 80% in 2017), both at Group level and in all its banking subsidiaries.

Foreign exchange

Foreign-exchange risk management of BBVA’s long-term investments, basically stemming from its franchises abroad, aims to preserve the Group’s capital adequacy ratios and ensure the stability of its income statement.

The first nine months has been marked by:

- The debate on the removal of negative rates by the ECB and a reduction in the asset purchasing program (QE) in view of the improvement in macroeconomic data.

- The result of the French elections.

- Activation of the process for the United Kingdom's exit from the European Union (Brexit).

- The gradual interest-rate hike by the Federal Reserve (Fed) and the announcement of a normalization of its balance sheet following positive macroeconomic data (pending inflation figures).

- Uncertainty with respect to the fiscal and commercial policies of the new U.S. administration, which generated a high level of volatility in the case of the Mexican peso, above all in the first three months of 2017.

In this context, BBVA has maintained its policy of actively hedging its main investments in emerging countries, covering on average between 30% and 50% of earnings expected for 2017 and around 70% of the excess CET1 capital ratio (which is not naturally covered by the ratio itself). In accordance with this policy, at the close of September 2017, the sensitivity of the CET1 ratio to a depreciation of 10% of the main emerging currencies (Mexican peso or Turkish lira) against the euro remains limited to less than 2 basis points, and the coverage level of the expected earnings for 2017 in these two countries would be around 60% in Mexico and 50% in Turkey.

Interest rates

The aim of managing interest-rate risk is to maintain a sustained growth of net interest income in the short and medium term, irrespective of interest-rate fluctuations, while controlling the impact on the capital adequacy ratio through the valuation of the portfolio of available-for-sale assets.

The Group’s banks have fixed-income portfolios to manage the balance-sheet structure. In the first nine months of 2017, the results of this management have been satisfactory, with limited risk strategies in all the Group’s banks.

Finally, the following is worth noting with respect to the monetary policy pursued by the different central banks of the main geographical areas where BBVA operates between January and September 2017:

- No relevant changes in the Eurozone, where rates remain at 0%.

- In the United States the upward trend in interest rates continues, with a rise in March and another in June, to 1.25%.

- In Mexico, Banxico has made a number of interest-rate hikes so far this year, so the monetary policy level at the close of September is 7%.

- In Turkey, the period has been marked by the Central Bank’s (CBRT’s) interest-rate hikes, which have increased the average cost of funding to 11.99%.

- In South America, the monetary authorities have continued their expansive policies, lowering rates in Peru (75 basis points), Colombia (225 basis points) and Chile (100 basis points). In Argentina, where inflation has resisted falling, there has been an increase of 150 basis points.

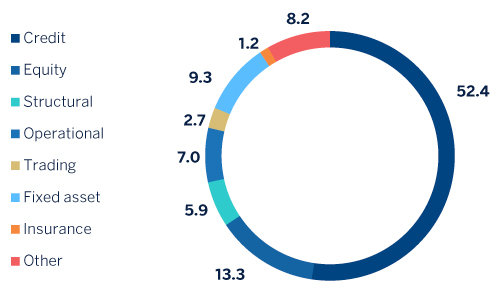

Economic capital

Consumption of economic risk capital (ERC) at the close of August 2017 stood at €35,334m in consolidated terms, which is equivalent to a decline of 2.0% with respect to the end of May this year (down 0.5% at constant exchange rates). This fall is mainly focused on goodwill (included in equity ERC and due to the depreciation of the dollar against the euro), trading risk (mainly in Spain and Turkey) and fixed assets (focused on asset withdrawals in the Anida Operaciones Singulares unit).

Attributable economic risk capital breakdown

(Percentage as of August 2017)