Solvency

Capital base

BBVA's fully loaded CET1 ratio stood at 11.6% as of the end of September 2019, isolating the impact of the first IFRS 16 implementation which came into effect on January 1, 2019 (-11 basis points) represents a growth of 33 basis points compared to December 2018. This increase is supported by the recurring organic capital generated and the impacts on the capital ratio of the positive evolution of the markets registered, mainly during the first six months of the year.

Risk-weighted assets (RWA) increased at current euros by approximately €19,800m in the first nine months of 2019 as a result of the growth of activity, mainly in the emerging markets, the incorporation of regulatory impacts (IFRS 16 implementation and TRIM — Targeted Review of Internal Models) for approximately €7,300m (which have had an impact on the CET1 ratio of -24 basis points); additionally, the impact of appreciation, particularly the U.S. Dollar and Mexican Peso, has increased the RWA by approximately €5,300m. Finally, in the second quarter of the year, the European Commission recognized Argentina as a country whose supervisory and regulatory1 requirements are considered equivalent, which has a positive impact on the RWA evolution.

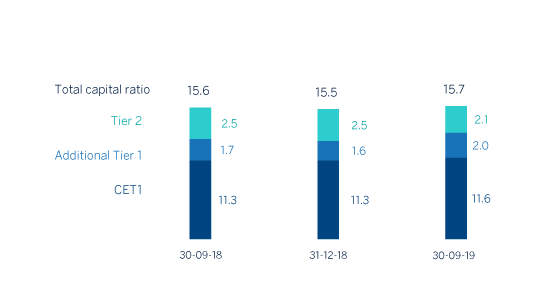

Fully-loaded capital ratios (Percentage)

Capital base (Millions of euros)

| CRD IV phased-in | CRD IV fully-loaded | |||||

|---|---|---|---|---|---|---|

| 30-09-19 (1) (2) | 31-12-18 | 30-09-18 | 30-09-19 (1) (2) | 31-12-18 | 30-09-18 | |

| Common Equity Tier 1 (CET 1) | 43,423 | 40,313 | 39,662 | 42,626 | 39,571 | 38,925 |

| Tier 1 | 51,029 | 45,947 | 45,765 | 50,103 | 45,047 | 44,868 |

| Tier 2 | 8,638 | 8,756 | 8,847 | 7,798 | 8,861 | 8,670 |

| Total Capital (Tier 1 + Tier 2) | 59,668 | 54,703 | 54,612 | 57,901 | 53,907 | 53,538 |

| Risk-weighted assets | 368,136 | 348,264 | 343,051 | 368,630 | 348,804 | 343,271 |

| CET1 (%) | 11.8 | 11.6 | 11.6 | 11.6 | 11.3 | 11.3 |

| Tier 1 (%) | 13.9 | 13.2 | 13.3 | 13.3 | 12.9 | 13.1 |

| Tier 2 (%) | 2.3 | 2.5 | 2.6 | 2.1 | 2.5 | 2.5 |

| Total capital ratio (%) | 16.2 | 15.7 | 15.9 | 15.7 | 15.5 | 15.6 |

- (1) As of September 30, 2019, the difference between the phased-in and fully-loaded ratios arises from the temporary traetment of certain capital items, mainly of the impact of IFRS9, to which the BBVA Group has adhered voluntarily (in accordance with article 473bis of the CRR).

- (2) Provisional data.

In terms of capital issuances, BBVA S.A. conducted three public capital issuances: the issuance of preferred securities that may be converted into ordinary BBVA shares (CoCos), registered with the Spanish Securities Market Commission (CNMV) for €1,000m, at an annual coupon of 6.0% and an amortization option after five years of being issued; another issuance of CoCos, registered with the Securities Exchange Commission (SEC), for US$1,000m and a coupon of 6.5% with an amortization option after five and a half years; and a Tier 2 subordinated debt issuance of €750m, with a maturity period of 10 years, an amortization option after five years of being issued and a coupon of 2.575%2. In the first nine months of the year the Group continued its funding program to meet the MREL (minimum requirement for own funds and eligible liabilities) requirements published in May 2018, by closing three public issuances of senior non-preferred debt for a total of €3,000m, one of which, for €1,000m, was a green bond.

Additionally, the early amortization options on three issuances were exercised: one for CoCos, for €1,500m with a coupon of 7% issued in February 2014; another issuance of Tier 2 subordinated debt, for €1,500m with a coupon of 3.5% issued in April 2014 and amortized in April 2019; and a further Tier 2 debt issued in June 2009 by Caixa d'Estalvis de Sabadell with an outstanding nominal amount of €4,878,000, amortized in June 2019.

In terms of the Group’s remaining subsidiaries, Mexico carried out the issuance of a Tier 2 debt instrument for US$750m with a maturity period of 15 years with an early amortization option in the tenth year and a coupon of 5.875%. The funds obtained were used to carry out a partial repurchase of two subordinated issuances (US$250m with maturity in 2020 and US$500m with maturity in 2021).

Regarding shareholder remuneration, on October 15 a gross cash dividend was paid for the financial year 2019 of €0.10 per share, in line with the Group's dividend policy of maintaining a pay-out ratio of 35-40% of recurring profit.

The phased-in CET1 ratio stood at 11.8% as of September 30, 2019, taking into account the effect of the IFRS 9 standard. Tier 1 stood at 13.9% and Tier 2 at 2.3%, resulting in a total capital ratio of 16.2%.

These levels are above the requirements established by the supervisor in its SREP letter (Supervisory Review and Evaluation Process), applicable in 2019. Since March 1, 2019, at the consolidated level, this requirement has been established at 9.26% for the CET1 ratio and 12.76% for the total capital ratio. Its variation compared to 2018 is explained by the end of the transitional period for the implementation of the capital conservation buffer and the capital buffer applicable to Other Systemically Important Institutions, as well as the progression of the countercyclical capital buffer. For its part, the CET1 Pillar 2 requirement (P2R) remains unchanged at 1.5%.

Finally, the Group's maintained a solid leverage ratio of 6.9% fully-loaded (7.0% phased-in), the highest among its peer group.

1 On April 1, 2019, the Official Journal of the European Union published Commission Implementing Decision (EU) No 2019/536, which includes Argentina within the list of third countries and territories whose supervisory and regulatory requirements are considered equivalent for the purposes of the treatment of exposures in accordance with Regulation (EU) No 575/2013.

2 These issuances are calculated as capital instruments (as additional Tier 1 the first two and as Tier 2 the last one) without prior authorization required, all in accordance with the Royal Decree 309/2019, of April 26, which partially implements Law 5/2019, of March 15, regulating real estate loan agreements and adopting other financial measures.

Ratings

During the first nine months of the year, Moody's, S&P, DBRS and Scope confirmed the rating they assign to BBVA's senior preferred debt (A3, A-, A (high) and A+ respectively). Fitch increased this rating by a notch in July 2019, considering that BBVA's loss-absorbing capital buffers (such as senior non-preferred debt) are sufficient to materially reduce the risk of default. In these actions, the agencies highlighted the Group's diversification and self-sufficient franchise model, with subsidiaries responsible for managing their own liquidity. These ratings, together with their outlooks, are shown in the following table:

Ratings

| Rating agency | Long term (1) | Short term | Outlook |

|---|---|---|---|

| DBRS | A (high) | R-1 (middle) | Stable |

| Fitch | A | F-1 | Negative |

| Moody’s | A3 | P-2 | Stable |

| Scope Ratings | A+ | S-1+ | Stable |

| Standard & Poor’s | A- | A-2 | Negative |

- (1) Ratings assigned to long term senior preferred debt. Additionally, Moody’s and Fitch assign A2 and A rating respectively, to BBVA’s long term deposits.