Risk management

Credit risk

The calculation of the expected credit losses at the end of March includes the update of the forward looking information in the models under IFRS 9 in order to reflect the circumstances created by the COVID-19 pandemic in the macroeconomic environment, which is characterized by a high degree of uncertainty regarding its intensity and duration. As a consequence, this update is based on the best information available between the reporting date of this report and its date of publication. This information may change in the future depending on the evolution of the macroeconomic environment or its uncertainty. The effect of the aforementioned update is significant in terms of estimated losses and has been calculated for all geographical areas where the Group operates, taking into account both the macroeconomic scenarios as well as the effects on specific sectors and customers as much as possible. The scenarios consider the various economic measures which have been announced by governments and monetary authorities all over the world. Due to this, the scenarios include the prediction that in a relatively close time horizon, a more aligned economic environment with the previously existing long-term perspectives may be reached.

BBVA Group's main risk indicators evolved as follows in the first quarter of 2020, as a result, among other reasons, of the situation explained in the previous paragraph:

- Credit risk remained stable at +0.2% in the quarter. Nonetheless, at constant exchange rates, it grew by 3.1% with generalized increases in all geographical areas.

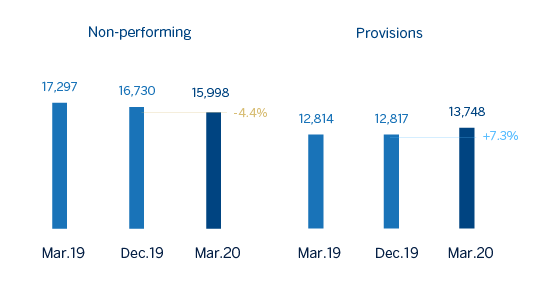

- The balance of non-performing loans fell by 4.4% in the first quarter of 2020 (down 1.3% at constant exchange rates), primarily due to the reduction in Spain.

- The NPL ratio stood at 3.6% as of March 31, 2020 which represents a decrease of 17 basis points compared to December 2019.

- Loan-loss provisions increased strongly by 7.3% in the last three months (up 13.6% at constant exchange rates) due to the higher provisions for the adjustment in the macro scenario due to the negative effects of COVID-19 and for specific clients in the commercial portfolio of certain business areas.

- The NPL coverage ratio closed at 86%, which was an improvement of 932 basis points compared to the end of 2019.

- The cumulative cost of risk stood at 2.57% as of March 31, 2020, which represents a significant increase of 155 basis points compared to the figure at the end of 2019.

Non-performing loans and provisions (Millions of euros)

Credit risk (1) (Millions of euros)

| 31-03-20 (2) | 31-12-19 (2) | 30-09-19 (2) | 30-06-19 | 31-12-18 | |

|---|---|---|---|---|---|

| Credit risk | 442,648 | 441,964 | 438,177 | 434,955 | 439,152 |

| Non-performing loans | 15,998 | 16,730 | 17,092 | 16,706 | 17,297 |

| Provisions | 13,748 | 12,817 | 12,891 | 12,468 | 12,814 |

| NPL ratio (%) | 3.6 | 3.8 | 3.9 | 3.8 | 3.9 |

| NPL coverage ratio (%)(3) | 86 | 77 | 75 | 75 | 74 |

- (1) Include gross loans and advances to customers plus guarantees given.

- (2) Figures without considering the classification of BBVA Paraguay as non-current assets and liabilities held for sale (NCA&L).

- (3) The NPL coverage ratio includes the valuation adjustments for credit risk during the expected residual life of those financial instruments which have been acquired (mainly originated from the acquisition of Catalunya Banc, S.A.). Excluding these allowances, the NPL coverage ratio would stand at 83% as of March 31, 2020, 74% in 2019 and 71% as of March 31, 2019.

Breakdown of credit risk according to stage (Millons of euros)

| 31-03-2020 | 31-12-2019 | 31-03-19 | ||||

|---|---|---|---|---|---|---|

| Gross exposure |

Provisions | Gross exposure |

Provisions | Gross exposure |

Provisions | |

| Loans and advances to customers | 397,170 | (13,368) | 396,012 | (12,447) | 393,321 | (12,522) |

| Stage 1 | 348,564 | (2,794) | 346,548 | (2,138) | 345,654 | (2,152) |

| Stage 2 | 33,316 | (2,448) | 33,464 | (2,185) | 31,109 | (2,440) |

| Stage 3 | 15,291 | (8,126) | 16,000 | (8,124) | 16,559 | (7,930) |

| Contingent risks | 45,478 | (380) | 45,952 | (370) | 45,831 | (292) |

| Stage 1 | 41,266 | (58) | 41,715 | (60) | 41,955 | (34) |

| Stage 2 | 3,504 | (98) | 3,507 | (83) | 3,138 | (92) |

| Stage 3 | 708 | (224) | 731 | (227) | 738 | (167) |

| Credit risk | 442,648 | (13,748) | 441,964 | (12,817) | 439,152 | (12,814) |

| Stage 1 | 389,830 | (2,852) | 388,263 | (2,197) | 387,608 | (2,185) |

| Stage 2 | 36,820 | (2,546) | 36,971 | (2,269) | 34,247 | (2,532) |

| Stage 3 | 15,998 | (8,349) | 16,730 | (8,351) | 17,297 | (8,097) |

- (1) Figures without considering the classification of BBVA Paraguay as non-current assets and liabilities held for sale (NCA&L).

Non-performing loans evolution (Millones de euros)

| 1Q20 (1) (2) | 4Q19 (2) | 3Q19 (2) | 2Q19 | 1Q19 | |

|---|---|---|---|---|---|

| Beginning balance | 16,730 | 17,092 | 16,706 | 17,297 | 17,087 |

| Entries | 2,121 | 2,484 | 2,565 | 2,458 | 2,353 |

| Recoveries | (1,435) | (1,509) | (1,425) | (1,531) | (1,409) |

| Net variation | 686 | 975 | 1,139 | 927 | 944 |

| Write-offs | (944) | (1,074) | (991) | (958) | (775) |

| Exchange rate differences and other | (474) | (262) | 237 | (561) | 41 |

| Period-end balance | 15,998 | 16,730 | 17,092 | 16,706 | 17,297 |

| Memorandum item: | |||||

| Non-performing loans | 15,291 | 16,000 | 16,400 | 15,999 | 16,559 |

| Non performing guarantees given | 708 | 731 | 692 | 707 | 738 |

- (1) Preliminary data.

- (2) Figures without considering the classification of BBVA Paraguay as non-current assets and liabilities held for sale (NCA&L).

Structural risks

Liquidity and funding

Management of liquidity and funding at BBVA aims to finance the recurring growth of the banking business at suitable maturities and costs, using a wide range of instruments that provide access to a large number of alternative sources of financing. In this context, it is important to notice that given the nature of BBVA’s business, the funding of lending activity is fundamentally carried out through the use of stable customer funds.

Due to its subsidiary-based management model, BBVA is one of the few major European banks that follows the Multiple Point of Entry (MPE) resolution strategy: the parent company sets the liquidity policies, but the subsidiaries are self-sufficient and responsible for managing their own liquidity (taking deposits or accessing the market with their own rating), without fund transfers or financing occurring between either the parent company and the subsidiaries, or between the different subsidiaries. This strategy limits the spread of a liquidity crisis among the Group's different areas, and ensures that the cost of liquidity and financing is correctly reflected in the price formation process.

During the first quarter of 2020, liquidity conditions remained comfortable across all countries in which the BBVA Group operates. In the second part of the quarter, the global crisis caused by COVID-19 had a significant impact on financial markets. The effects of this crisis on the Group's balance sheets have fundamentally been felt through greater drawing down of credit facilities by wholesale customers in the face of worsening funding conditions in the markets, with no significant effect in the retail world. In view of this situation, a joint response has been made by the different central banks, through specific measures and programs to facilitate the funding of the real economy and the availability of liquidity in the financial markets.

BBVA Group maintains a solid liquidity position in every geographical area with regulatory ratios remained comfortably above the minimum levels required:

- The BBVA Group's liquidity coverage ratio (LCR) remained significantly above 100% and stood at 134% as of March 31, 2020. For the calculation of this ratio, it is assumed that there is no transfer of liquidity among subsidiaries; i.e. no kind of excess liquidity levels in foreign subsidiaries are considered in the calculation of the consolidated ratio. When considering these excess liquidity levels, the BBVA Group's LCR would stand at 156% (22 percentage points above 134%). In addition, it comfortably exceeded 100% in all subsidiaries (Eurozone 156%, Mexico 146%, the United States 144% and Turkey 153%).

- The Net Stable Funding Ratio (NSFR), defined as the ratio between the amount of stable funding available and the amount of stable funding required, is one of the Basel Committee's essential reforms, and requires banks to maintain a stable funding profile in relation to the composition of their assets and off-balance sheet activities. This ratio should be at least 100% at all times. At the BBVA Group, the NSFR, calculated according to the Basel requirements, remained above 100% throughout 2020 and stood at 120% as of March 31, 2020. It comfortably exceeded 100% in all subsidiaries (Eurozone 114%, Mexico 127%, United States 112% and Turkey 151%).

The most relevant aspects related to the main geographical areas are the following:

- In the Eurozone, the liquidity situation remains comfortable with a high quality ample liquidity buffer. The impact of the COVID-19 crisis has led to greater loan volumes through the increase in the drawing down of credit facilities in the wholesale business of Corporate & Investment Banking, also accompanied by a growth in customer deposits. In addition, it is important to mention the different measures implemented by the European Central Bank (ECB) in order to face the crisis, such as the expansion of asset purchase programs, especially through the PEPP (Pandemic Emergency Purchase Program) for €750,000m until the end of the year, the coordinated action of Central Banks for the provision of US dollars, a package of temporary collateral easing measures affecting eligibility for use in funding operations and the easing and improvement of the conditions for the TLTRO III program. This easing of the TLTRO III program conditions will allow the increase of the maximum amount available for BBVA from €21 billion to €35 billion.

- BBVA USA also maintains an adequate liquidity buffer consisting of high-quality assets which allows it to face this environment from a sound position. As in the Eurozone, there was an increase in loans mainly due to a rise in the drawing down of credit facilities by companies. Deposits also grew in the quarter although at a slower rate than loans.

- In BBVA Mexico, the liquidity situation remained sound in the first quarter of 2020. As in the previously mentioned geographical areas, as a result of the COVID-19 crisis, there was an increase in the drawdowns of credit facilities, mainly by wholesale customers, which was largely offset by the increase in deposits, and ending the quarter with a comfortable position in all liquidity ratios. Regarding the measures taken by Banxico, in addition to reducing the monetary policy rate, it announced a reduction in the Monetary Regulation Deposit and the start of auctions of US dollars with credit institutions (swap line with the Fed).

- In Garanti BBVA, the liquidity situation remained comfortable in the first quarter of 2020 with a similar contraction in foreign currency loans and deposits, while in the local currency there was similar growth in deposits and loans. As a result of the COVID-19 crisis, there have been increases in some credit risk indicators in Turkey (Credit Default Swaps) which have led to increased collateral requirements that cover derivative valuations and wholesale funding. These increased collateral requirements have been met through the entity’s excess liquidity. Despite these outflows, Garanti BBVA maintains a sound liquidity buffer.

- In South America, an adequate liquidity situation prevails throughout the region despite increased volatility in the financial markets in the last month. In Argentina, outflows of US dollar deposits in the banking system have been gradually declining over the first quarter. BBVA Argentina continues to maintain a sound liquidity position, as shown by the liquidity ratios. In Colombia, market volatility has resulted in an increase in customer bank deposits (improving the credit gap) by increasing the preference for liquidity and reducing off-balance sheet funds (mutual funds). An adequate liquidity position also prevails in Peru.

After two months of great stability at the start of 2020, the wholesale funding markets in which the Group operates were affected by the events of COVID-19 and secondary prices suffered a material correction as a result of the increased volatility. This led to a significant increase in the issue premiums and levels of access to the primary market.

The main transactions carried out by the companies that form part of the BBVA Group in the first quarter of 2020 were:

- BBVA S.A. carried out two issuances of senior non-preferred debt totaling €1,400m and a Tier 2 issuance totaling €1,000m (see the “Solvency” chapter of this report for more information).

- In the United States, BBVA USA did not issue wholesale debt in the first quarter, in line with the funding plan.

- In Mexico, a local senior issuance was successfully carried out in February for MXN 15,000m (€573m) in three tranches. Two tranches in Mexican pesos over 3 and 5 years (one for MXN 7,123m at the Interbank Equilibrium Interest Rate (TIIE) 28 plus 5 basis points and another for MXN 6,000m at TIIE 28 plus 15 basis points, respectively), and another tranche in US dollars over 3 years (USD 100m at 3-month Libor plus 49 basis points). The purpose of this issuance was to bring forward the refinancing of maturities in the year, taking advantage of the good market conditions, as well as to strengthen the liquidity situation by offsetting the seasonal outflows of deposits in the early months of the year.

- In Turkey, Garanti BBVA carried out a Tier 2 issuance for TRY 750m (see the “Solvency” chapter of this report for more information).

- In South America, there have been no issuances during the first quarter of 2020.

Foreign exchange

Foreign exchange risk management of BBVA's long-term investments, principally stemming from its overseas franchises, aims to preserve the Group's capital adequacy ratios and ensure the stability of its income statement.

In the first quarter of 2020, foreign exchange markets have also been affected by the shock of COVID-19 spreading globally and its effects on the economy. As a result, after a good start to the year, the Mexican peso closed the first quarter with a depreciation of 18.9% against the euro. Another currency that has been hit hard by these conditions is the Colombian peso (down 17.3%), which like the Mexican peso has been affected by the sharp fall in oil prices. Other currency depreciations have been smaller: Chilean peso (down 9.3%), Turkish lira (down 7.2%), Argentine peso (down 4.7%) and Peruvian sol (down 0.9%). In contrast, the US dollar (up 2.5%) has appreciated against the euro in this environment. BBVA has maintained its policy of actively hedging its main investments in emerging markets, covering on average between 30% and 50% of annual earnings and around 70% of the CET1 capital ratio excess. Based on this policy, the sensitivity of the CET1 ratio to a 10% depreciation of the main emerging-market currencies against the euro stood at -3 basis points for the Mexican peso and -3 basis points for the Turkish lira. In the case of the US dollar, the sensitivity to a depreciation of 10% against the euro is approximately +10 basis points, as a result of RWAs denominated in US dollars outside the United States. At the close of March, the coverage level for expected earnings for 2020 stood near 50% in Turkey, 100% in Mexico and also at a very high level in the case of Colombia.

Interest rate

The aim of managing interest-rate risk is to limit the sensitivity of the balance sheets to interest rate fluctuations. BBVA carries out this work through an internal procedure following the guidelines established by the European Banking Authority (EBA), which measures the sensitivity of net interest income and economic value to determine the potential impact of a range of scenarios on the Group's different balance sheets.

The model is based on assumptions intended to realistically mimic the behavior of the balance sheet. Of particular relevance are assumptions regarding the behavior of accounts with no explicit maturity and prepayment estimates. These assumptions are reviewed and adapted at least once a year to take into account any changes in behavior.

At the aggregate level, BBVA continues to maintain a moderate risk profile, in line with the established target, showing a net interest income position which would be favored by an increase in interest rates, through effective management of structural balance sheet risk, taking into account the volatility in rates generated by COVID-19 in the second part of the quarter, this having virtually no effect due to the sound recurrence of the income.

By area, the main features are:

- Spain and the United States have balance sheets characterized by a high proportion of variable-rate loans in the loan portfolio (basically, mortgages in Spain and corporate lending in both countries) and liability composed mainly of customer deposits. The ALCO portfolios act as hedging for the bank's balance sheet, mitigating its sensitivity to interest rate fluctuations. The profile of both balance sheets has remained stable during the first quarter of 2020, with a moderate increase in the sensitivity of net interest income in the United States due to higher forecasts for prepayments in mortgage assets in the face of falling market rates.

In addition, European benchmark interest rates (Euribor) have continued to fall slightly from the close of 2019 to mid-March, recovering since then by around 20-30 basis points (depending on the maturity). This has mainly been the result of two aspects: first, the adjustment of expectations after the European Central Bank maintained the marginal deposit facility rate at -0.50% when the market had discounted a reduction; second, the increase in the required credit spread (since Euribor is a non-collateralized interest rate) and the illiquidity or lack of transactions in the commercial paper market. In the United States, benchmark rates (Libor) have fallen in the quarter (-75 basis points for the 1-month benchmark, -100 basis points for the 12-month benchmark) following the Fed's rate cuts. - Mexico continues to show a balance between the balance sheet items benchmarked at fixed and variable interest rates. In terms of the assets most sensitive to interest rate fluctuations, the corporate portfolio stands out, while consumer loans and mortgages are mostly at a fixed rate. The ALCO portfolio is used to neutralize the longer duration of customer deposits. The sensitivity of net interest income continues to be limited and stable in 2020, considering the new interest rate scenario that emerged in March, where the market is discounting lower benchmark rates throughout 2020 compared to the start of the quarter. The variation has been significantly lower for longer maturities.

- In Turkey, the interest rate risk (broken down into Turkish lira and US dollars) was very limited: on the asset side, the sensitivity of loans, mostly fixed rate but with relatively short maturities and the ALCO portfolio, including inflation-linked bonds, is balanced by the sensitivity of deposits, which are re-priced in the short term, in liabilities. The evolution of the currency balance sheets was positive in the year, showing a reduction in the sensitivity of the net interest income. In this new scenario, the market is discounting a benchmark rate below that discounted at the beginning of the quarter.

- In South America, the interest rate risk remained low due to the fixed/variable composition and maturities being very similar for assets and liabilities in most countries in the region. In addition, in balance sheets with several currencies, interest rate risk is managed for each of the currencies, showing a very low level of risk. Balance sheet profiles in the countries that make up this business area remain stable, maintaining a near-constant and limited net interest income sensitivity throughout 2020. Central bank reactions have shown a benchmark rate path below that expected at the beginning of the quarter.