The United States

Highlights

- Increase in loans on the commercial portfolios, whereas retail segments have been affected by the pandemic. Strong increase in customer deposits.

- The cost of risk continues to improve.

- Positive evolution of fees and commissions and NTI.

- Lower net attributable profit due to a fall in net interest income and a significant increase in the impairment on financial assets line.

Business activity (1)

(Year-on-year change at constant exchange rate. Data as of 30-09-20)

(1) Excluding repos.

Net interest income/ATAs

(Percentage. Constant exchange rate)

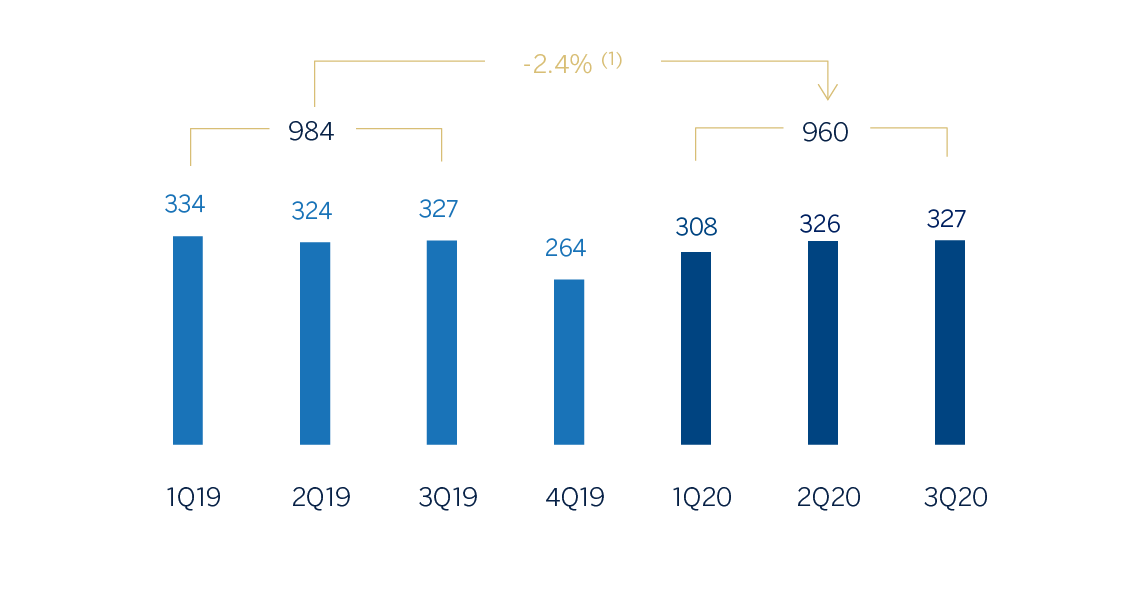

Operating income

(Millions of euros at constant exchange rate)

(1) At current exchange rate: -2.8%.

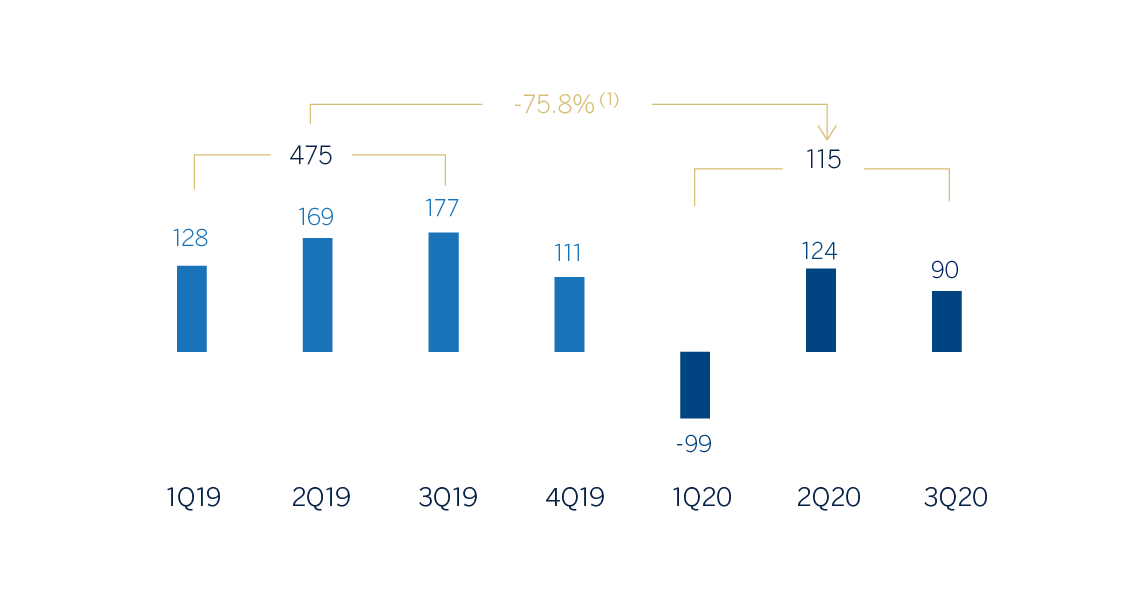

Net attributable profit

(Millions of euros at constant exchange rate)

(1) At current exchange rate: -75.9%.

Financial statements and relevant business indicators

(Millions of euros and percentage)

| Income statement | Jan.-Sep. 20 | ∆% | ∆% (1) | Jan.-Sep. 19 |

|---|---|---|---|---|

| Net interest income | 1,708 | (5.8) | (5.5) | 1,813 |

| Net fees and commissions | 503 | 2.9 | 3.3 | 489 |

| Net trading income | 176 | 27.0 | 28.8 | 139 |

| Other operating income and expenses | (13) | n.s. | n.s. | 2 |

| Gross income | 2,374 | (2.8) | (2.4) | 2,442 |

| Operating expenses | (1,414) | (2.8) | (2.5) | (1,454) |

| Personnel expenses | (821) | (2.2) | (1.9) | (839) |

| Other administrative expenses | (435) | (3.2) | (2.9) | (449) |

| Depreciation | (158) | (4.2) | (4.0) | (165) |

| Operating income | 960 | (2.8) | (2.4) | 989 |

| Impaiment on financial assets not measured at fair value through profit or loss | (848) | 108.9 | 109.1 | (406) |

| Provisions or reversal of provisions and other results | 5 | (5.1) | 5.7 | 5 |

| Profit/(loss) before tax | 117 | (80.0) | (79.9) | 588 |

| Income tax | (3) | (97.7) | (97.7) | (110) |

| Profit/(loss) for the year | 115 | (75.9) | (75.8) | 478 |

| Non-controlling interests | - | - | - | - |

| Net attributable profit | 115 | (75.9) | (75.8) | 478 |

| Balance sheets | 30-09-20 | ∆% | ∆%(1) | 31-12-19 |

|---|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 17,205 | 107.5 | 116.2 | 8,293 |

| Financial assets designated at fair value | 6,654 | (13.1) | (9.5) | 7,659 |

| Of which: Loans and advances | 345 | 32.0 | 37.6 | 261 |

| Financial assets at amortized cost | 70,435 | 1.3 | 5.6 | 69,510 |

| Of which: Loans and advances to customers | 61,987 | (1.9) | 2.3 | 63,162 |

| Inter-area positions | - | - | - | - |

| Tangible assets | 857 | (6.2) | (2.3) | 914 |

| Other assets | 2,581 | 19.9 | 25.0 | 2,153 |

| Total assets/liabilities and equity | 97,732 | 10.4 | 15.1 | 88,529 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 336 | 19.4 | 24.5 | 282 |

| Deposits from central banks and credit institutions | 5,914 | 44.9 | 51.0 | 4,081 |

| Deposits from customers | 73,297 | 8.5 | 13.1 | 67,525 |

| Debt certificates | 3,096 | (12.8) | (9.1) | 3,551 |

| Inter-area positions | 4,909 | 43.7 | 49.8 | 3,416 |

| Other liabilities | 6,535 | 12.1 | 16.8 | 5,831 |

| Economic capital allocated | 3,644 | (5.2) | (1.2) | 3,843 |

| Relevant business indicators | 30-09-20 | ∆% | ∆% (1) | 31-03-19 |

|---|---|---|---|---|

| Performing loans and advances to customers under management (2) | 62,698 | (0.9) | 3.3 | 63,241 |

| Non-performing loans | 1,264 | 73.2 | 80.5 | 730 |

| Customer deposits under management (2) | 73,300 | 8.5 | 13.1 | 67,528 |

| Off-balance sheet funds (3) | - | - | - | - |

| Risk-weighted assets | 63,021 | (3.3) | 0.8 | 65,170 |

| Efficiency ratio (%) | 59.5 | 61.0 | ||

| NPL ratio (%) | 1.9 | 1.1 | ||

| NPL coverage ratio (%) | 95 | 101 | ||

| Cost of risk (%) | 1.69 | 0.88 |

- (1) Figures at constant exchange rate.

- (2) Excluding repos.

- (3) Includes mutual funds, pension funds and other off-balance sheet funds.

Activity

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and earnings, will be given at constant exchange rates. These rates, together with changes at current exchange rates, can be found in the attached tables of financial statements and relevant business indicators.

The most relevant aspects related to the area's activity during the first nine months of 2020 were:

- The lending activity for the area (performing loans under management) showed lower dynamism between July and September (down 5.3% in the quarter), due to the combined effect of several factors, including the volume of liquidity injected into the system until June and the use by companies of credit facilities provided during the first and second quarters of the year. In comparison with December 2019, the loan portfolio increased by 3.3%, mainly due to the growth of the Corporate and Business Banking segment (up 9.1%), which was driven by the Paycheck Protection Program. The rest of the retail portfolio showed reductions in rates of change with respect to the end of 2019 (down 2.3%), due to the unfavorable impact of the pandemic.

- In terms of risk indicators, the NPL ratio increased due to the entry into non-performing loans of some wholesale customers and closed at 1.9%. For its part, the NPL coverage ratio stood at 95%, compared to 101% at the end of December 2019.

- Customer deposits under management increased by 13.1% between January and September, in part due to the placement of the increased liquidity made available to customers in demand deposits.

Results

The United States generated a net attributable profit of €115m during the first nine months of 2020, 75.8% less than in the same period of the previous year. The most relevant aspects related to the income statement are summarized below:

- Net interest income fell by 5.5% year-on-year, affected by the Fed's interest rate cuts, for a total of 225 basis points since the first quarter of 2019, partially offset by the lower financing costs due to the excellent cost of deposits management, which led to a 4.8% increase in the quarter of this margin.

- Net fees and commissions closed with an increase of 3.3% compared to the same period last year (up 11.4% in the quarter), due mainly to commissions generated by the Global Markets unit.

- NTI contribution increased (up 28.8% year-on-year) thanks to the higher results of the Global Markets unit.

- Operating expenses fell compared to the same period of the previous year (down 2.5% year-on-year), as a result of both the decrease in some discretionary expenditures due to the pandemic and the containment plans implemented.

- Increase in the impairment on financial assets (up 109.1% year-on-year), explained mainly by the adjustment in the macroeconomic scenario due to the negative effects of COVID-19, mainly registered in the first quarter, and to higher loan-loss provisions to cover specific customers in the Oil & Gas sector. Consequently, the cumulative cost of risk as of September 2020 stood at 1.69%, after the rebound experienced in March due to the sharp increase in the impairment on financial assets.

- Income tax recorded a charge of €3m, significantly below that recorded in the previous year, as a result of the correction of the calculation of the effective tax rate for the year as a whole.