Solvency

Capital base

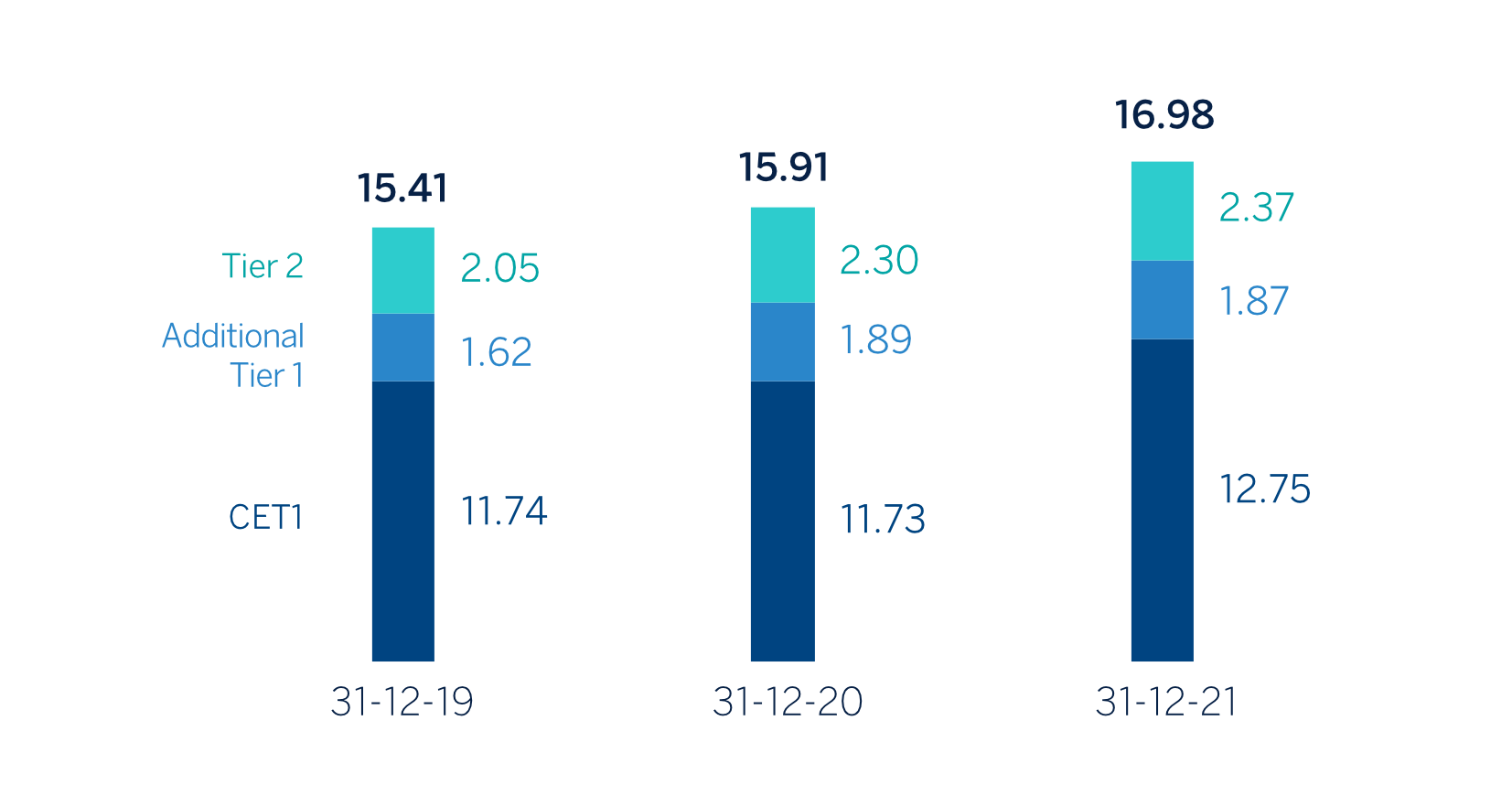

The Group's CET1 Fully-loaded ratio stood at 12.75% as of December 31, 2021, which represents a decrease in in the quarter (-173 basis points), although it maintains a large management buffer on the Group's capital requirements and is above the management target, which is to be within the range of 11.5-12% CET1. This CET1 level includes the deduction of the total amount of the share buyback program authorized by the supervisor, amounting to maximum €3.500m and representing an impact of approximately -130 basis points. For more information on the Group' share buyback program, please see "Other highlights" at the end of the "Highlights" section.

In addition to the above-mentioned effect, during the fourth quarter of 2021, the recurrent income generation net of dividends and remunerations of AT1 instruments contributed 18 basis points. On the other hand, the growth of risk-weighted assets (RWAs) had an impact of- 49 basis points, which is mostly explained by the growth of activity in the quarter and additionally, to a lesser extent, by the update of the RWAs for operational risk (which is carried out annually, and which is explained by the increase in the level of revenues compared to previous periods) and, by the growth of the RWAs that are specific to market activity and are exposed to higher volatility. Finally, the other items affecting the CET1, most notably the effect of exchange rate evolution and portfolio valuation, resulted in a reduction of 12 basis points.

The consolidated fully-loaded additional Tier 1 capital (AT1) stood at 1.87% as of December 31, 2021, which results in a decrease of -4 basis points compared to the previous quarter.

The consolidated fully-loaded Tier 2 ratio as of December 31, 2021 stood at 2.37%, a decrease of -11 basis points in the quarter. The total fully-loaded capital adequacy ratio stands at 16.98%.

Following the latest SREP (Supervisory Review and Evaluation Process) decision, received on February, 2022 and applicable as from March 1, 2022, the ECB has informed the Group that the Pillar 2 requirement would remain at 1.5% (of which 0.84% must be CET1 at least). Therefore, BBVA must maintain a CET1 capital ratio of 8.60% and a total capital ratio of 12.76% at the consolidated level.

The phased-in CET1 ratio, on consolidated terms, stood at 12.98% as of December 31, 2021, considering the transitory effect of the IFRS 9 standard. AT1 reached 1.86% and Tier 2 reached 2.40%, resulting in a total capital adequacy ratio of 17.24%.

FULLY-LOADED CAPITAL RATIOS (PERCENTAGE)

CAPITAL BASE (MILLIONS OF EUROS)

| CRD IV phased-in | CRD IV fully-loaded | |||||

|---|---|---|---|---|---|---|

| 31-12-21 (1) (2) | 31-12-20 | 31-12-19 | 31-12-21 (1) (2) | 31-12-20 | 31-12-19 | |

| Common Equity Tier 1 (CET 1) | 39,937 | 42,931 | 43,653 | 39,172 | 41,345 | 42,856 |

| Tier 1 | 45,674 | 49,597 | 49,701 | 44,910 | 48,012 | 48,775 |

| Tier 2 | 7,383 | 8,547 | 8,304 | 7,283 | 8,101 | 7,464 |

| Total Capital (Tier 1 + Tier 2) | 53,057 | 58,145 | 58,005 | 52,193 | 56,112 | 56,240 |

| Risk-weighted assets | 307,791 | 353,273 | 364,448 | 307,331 | 352,622 | 364,942 |

| CET1 (%) | 12.98 | 12.15 | 11.98 | 12.75 | 11.73 | 11.74 |

| Tier 1 (%) | 14.84 | 14.04 | 13.64 | 14.61 | 13.62 | 13.37 |

| Tier 2 (%) | 2.40 | 2.42 | 2.28 | 2.37 | 2.30 | 2.05 |

| Total capital ratio (%) | 17.24 | 16.46 | 15.92 | 16.98 | 15.91 | 15.41 |

- (1) As of December 31, 2021, the difference between the phased-in and fully-loaded ratios arises from the temporary treatment of certain capital items, mainly of the impact of IFRS 9, to which the BBVA Group has adhered voluntarily (in accordance with article 473bis of the CRR and the subsequent amendments introduced by the Regulation (EU) 2020/873).

- (2) Preliminary data.

Regarding shareholder remuneration, after the lifting of the recommendations by the European Central Bank, on September 30, 2021, BBVA informed that the BBVA’s Board of Directors approved the payment in cash of €0.08 gross per share, as gross interim dividend against 2021 results, which was paid on October 12, 2021. This dividend is already considered within the capital ratios of the Group. In addition, on February 3, 2022 it was announced that a cash distribution in the amount of €0.23 gross per share was expected to be submitted to the relevant governing bodies for consideration. If approved, the total cash distributions would amount to €0.31 gross per share. Therefore, the total shareholder remuneration will be the result of the cash payments discussed and the share buyback programs.

SHAREHOLDER STRUCTURE (31-12-2021)

| Shareholders | Shares issued | |||

|---|---|---|---|---|

| Number of shares | Number | % | Number | % |

| Up to 500 | 341,510 | 41.3 | 63,972,992 | 1.0 |

| 501 to 5,000 | 381,597 | 46.2 | 671,795,023 | 10.1 |

| 5,001 to 10,000 | 55,785 | 6.7 | 392,338,799 | 5.9 |

| 10,001 to 50,000 | 43,159 | 5.2 | 824,841,257 | 12.4 |

| 50,001 to 100,000 | 3,092 | 0.4 | 210,665,277 | 3.2 |

| 100,001 to 500,000 | 1,410 | 0.2 | 256,532,572 | 3.8 |

| More than 500,001 | 282 | 0.0 | 4,247,740,660 | 63.7 |

| Total | 826,835 | 100.0 | 6,667,886,580 | 100.0 |

With regard to MREL (Minimum Requirement for own funds and Eligible Liabilities) requirements, BBVA must reach, by January 1, 2022, an amount of own funds and eligible liabilities equal to 24.78%6 of the total RWAs of its resolution group, at a sub-consolidated7 level (hereinafter, the "MREL in RWAs"). This is currently the most restrictive requirement for BBVA. Given the structure of own funds and admissible liabilities of the resolution group, as of December 31, 2021, the MREL ratio in RWAs stands at 28.34%8,9, complying with the aforementioned MREL requirement.

With the aim of reinforcing compliance with these requirements, in March 2021, BBVA carried out an issue of a senior preferred debt for an amount of €1 billion, with a maturity of 6 years and an option for early redemption after five years. In September 2021, BBVA issued a €1 billion a floating rate senior preferred social bond, maturing in 2 years. These issuances have mitigated the loss of eligibility of three issuances, two senior preferred issues and one senior non-preferred issue issued during 2017 and reaching their maturity in 2021. In this regard, in January 2022, a senior non-preferred bond for €1 billion has been issued, with a maturity of 7 years and an option for early redemption in the sixth year, with a coupon of 0.875%, although it is not taken into account for the December 2021 ratios.

Lastly, the Group's leverage ratio stood at 6.7% fully-loaded (6.8% phased-in)10 as of December 31, 2021. These figures include the effect of the temporary exclusion of certain positions with the central banks of the different geographical areas where the Group operates, foreseen in the “CRR-Quick fix”.

Ratings

During 2021, BBVA’s rating has continued to show its strength and all agencies have maintained their rating in the A category. Last December, S&P upgraded BBVA’s rating one notch to A from A-, considering that a sizable enough cushion of bail-inable instruments has been issued, and following a methodological update that recognizes the strength of the Multiple Point of Entry (MPE) resolution strategy. The outlook changed to negative from stable, now conditioned by the rating given by S&P to the Spanish sovereign (also A, with negative outlook). The following table shows the credit ratings and outlook given by the agencies:

Ratings

| Rating agency | Long term (1) | Short term | Outlook |

|---|---|---|---|

| DBRS | A (high) | R-1 (middle) | Stable |

| Fitch | A- | F-2 | Stable |

| Moody’s | A3 | P-2 | Stable |

| Standard & Poor’s | A | A-1 | Negative |

(1) Ratings assigned to long term senior preferred debt. Additionally, Moody’s and Fitch assign A2 and A- rating respectively, to BBVA’s long term deposits.

4 Pursuant to the new applicable regulation, the MREL in RWAs and the subordination requirement in RWAs do not include the combined requirement of applicable capital buffers.

5 In accordance with the resolution strategy MPE (“Multiple Point of Entry”) of the BBVA Group, established by the SRB, the resolution group is made up of Banco Bilbao Vizcaya Argentaria, S.A. and subsidiaries that belong to the same European resolution group. As of December 31, 2019, the total RWAs of the resolution group amounted to €204,218m and the total exposure considered for the purpose of calculating the leverage ratio amounted to €422,376m

6 Own resources and eligible liabilities to meet, both, MREL and the combined capital buffer requirement applicable.

7 As of December 31, 2021, the MREL ratio in Leverage Ratio stands at 11.35% and the subordination ratios in terms of RWAs and in terms of exposure of the leverage ratio, stand at 24.65% and 9.87%, respectively, being preliminary data.

8The Group’s leverage ratio is provisional at the date of release of this report.