Turkey

Highlights

- Growth in activity, again driven by loans and deposits in Turkish lira

- Year-on-year growth in recurring revenue and NTI

- Solid risk indicators

- Positive half-year net attributable profit

Business activity (1)

(VARIATION AT CONSTANT EXCHANGE RATE COMPARED TO 31-12-21)

(1) Excluding repos.

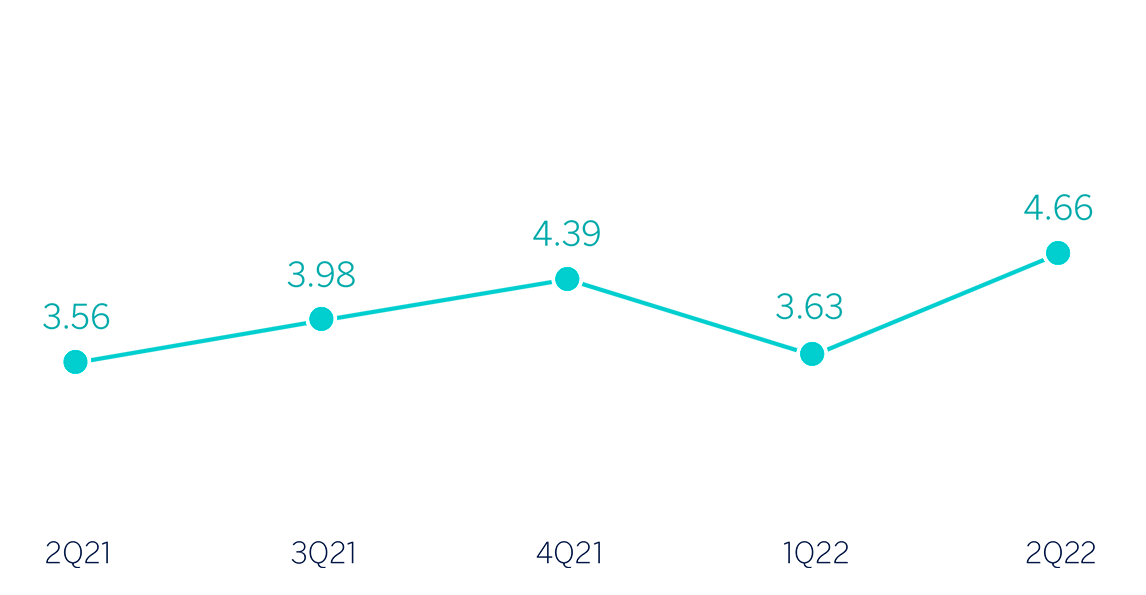

Net interest income/ AVERAGE TOTAL ASSETS

(Percentage at Constant exchange rate)

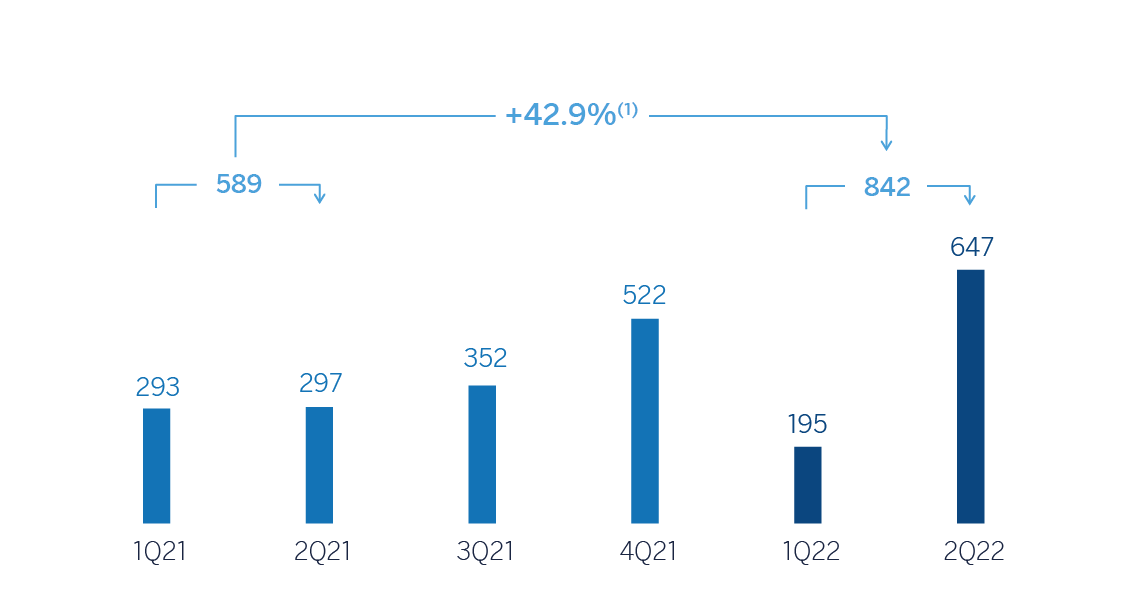

Operating income

(Millions of euros at constant exchange rate)

(1) At current exchange rate: -21.4%.

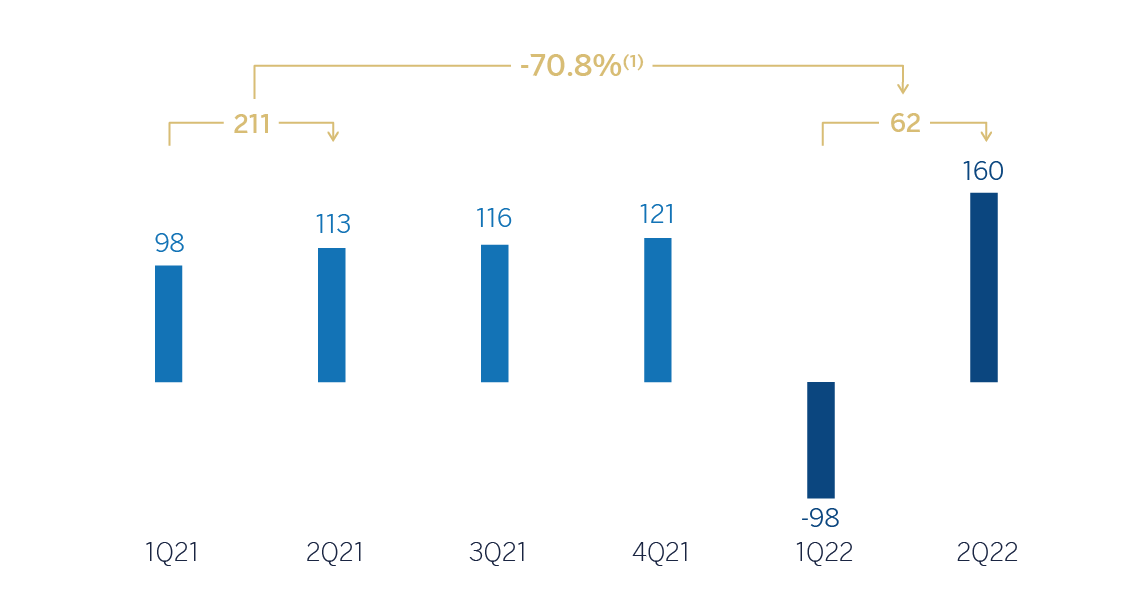

Net attributable profit (LOSS)

(Millions of euros at constant exchange rate)

(1) At current exchange rate: +84.0%.

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1H22 | ∆% | ∆% (1) | 1H21(2) |

|---|---|---|---|---|

| Net interest income | 1,163 | 12.2 | 104.2 | 1,036 |

| Net fees and commissions | 295 | (0.8) | 80.4 | 297 |

| Net trading income | 395 | 119.9 | 300.0 | 180 |

| Other operating income and expenses | (511) | n.s. | n.s. | 58 |

| Gross income | 1,342 | (14.6) | 55.4 | 1,571 |

| Operating expenses | (500) | 0.1 | 82.1 | (499) |

| Personnel expenses | (280) | (0.5) | 80.9 | (282) |

| Other administrative expenses | (156) | 1.2 | 84.1 | (154) |

| Depreciation | (64) | 0.3 | 82.4 | (64) |

| Operating income | 842 | (21.4) | 42.9 | 1,072 |

| Impairment on financial assets not measured at fair value through profit or loss | (171) | 2.1 | 85.8 | (168) |

| Provisions or reversal of provisions and other results | (34) | n.s. | n.s. | 48 |

| Profit (loss) before tax | 637 | (33.1) | 21.7 | 952 |

| Income tax | (636) | 264.7 | n.s. | (174) |

| Profit (loss) for the period | 1 | (99.8) | (99.7) | 778 |

| Non-controlling interests | 60 | n.s. | n.s. | (394) |

| Net attributable profit (loss) | 62 | (84.0) | (70.8) | 384 |

- (1)At constant exchange rate.

- (2) Restated balances due to reallocation of some technology expenses. For more information, please refer to the “Business Areas” section.

| Balance sheets | 30-06-22 | ∆% | ∆% (1) | 31-12-21 |

|---|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 8,051 | 3.7 | 17.9 | 7,764 |

| Financial assets designated at fair value | 5,598 | 5.8 | 20.3 | 5,289 |

| Of which: loans and advances | 1 | (99.8) | (99.8) | 295 |

| Financial assets at amortized cost | 48,362 | 16.4 | 32.4 | 41,544 |

| Of which: loans and advances to customers | 35,610 | 13.4 | 28.9 | 31,414 |

| Tangible assets | 921 | 47.8 | 68.1 | 623 |

| Other assets | 1,168 | 14.0 | 29.7 | 1,025 |

| Total assets/liabilities and equity | 64,101 | 14.0 | 29.6 | 56,245 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 2,381 | 4.8 | 19.2 | 2,272 |

| Deposits from central banks and credit institutions | 5,307 | 29.9 | 47.7 | 4,087 |

| Deposits from customers | 42,688 | 11.3 | 26.6 | 38,341 |

| Debt certificates | 3,897 | 7.7 | 22.5 | 3,618 |

| Other liabilities | 3,007 | 38.8 | 57.9 | 2,166 |

| Regulatory capital allocated | 6,821 | 18.4 | 34.6 | 5,761 |

| Relevant business indicators | 30-06-22 | ∆% | ∆% (1) | 31-12-21 |

|---|---|---|---|---|

| Performing loans and advances to customers under management (2) | 35,152 | 14.8 | 30.6 | 30,610 |

| Non-performing loans | 2,863 | (4.4) | 8.7 | 2,995 |

| Customer deposits under management (2) | 42,687 | 11.4 | 26.6 | 38,335 |

| Off-balance sheet funds (3) | 4,925 | 26.5 | 43.8 | 3,895 |

| Risk-weighted assets | 51,055 | 2.7 | 16.8 | 49,718 |

| Efficiency ratio (%) | 37.2 | 29.5 | ||

| NPL ratio (%) | 5.9 | 7.1 | ||

| NPL coverage ratio (%) | 83 | 75 | ||

| Cost of risk (%) | 0.88 | 1.33 |

- (1) At constant exchange rate.

- (2) Excluding repos.

- (3) Includes mutual funds and pension funds.

Macro and industry trends

Despite the complex local and global macroeconomic environment, economic activity has been stronger than expected in the first half of the year. According to BBVA Research’s estimates, the resilience in activity could lead to growth of 5.0% in 2022. This figure is significantly higher than the 2.5% forecasted 3 months ago. Moreover, the relative strength of demand, high commodity prices and the sharp depreciation of the Turkish lira in a context of negative interest rates in real terms have all contributed to an inflationary spike, with annual inflation reaching 78.6% in June 2022. According to BBVA Research's estimates, growth could slow to 3.0% in 2023, which would reduce inflationary pressures and improve the external accounts. However, the economic environment remains highly unstable due to the combination of high inflation, very low real rates, pressure on the Turkish lira, high external funding needs, and the current global context.

Total credit volumes in the banking system increased by 57.6% year-on-year in local currency terms as of May 2022, including +49,6% growth in the Turkish lira portfolio and +71,3% growth in the foreign currency credit portfolio. Meanwhile, deposits grew by 73.0%. These growth rates are adjusted for inflation and the depreciation of the Turkish lira. The system's NPL ratio stood at 2.61% in May 2022 (3.69% in May 2021 and 3.16% at the end of 2021).

Unless expressly stated otherwise, all comments below on rates of changes for both activity and income, will be presented at constant exchange rates. For the conversion of these figures, the exchange rate as of June 30, 2022 is used. These rates, together with changes at current exchange rates, can be observed in the attached tables of the financial statements and relevant business indicators.

Activity

The most relevant aspects related to the area’s activity during the first six months of 2022 were:

- Lending activity (performing loans under management) increased by 30.6% between January and June 2022, driven by the growth in Turkish lira loans (+36.0%). This growth was mainly supported by commercial loans and, to a lessor extent, credit cards and consumer loans. Foreign currency loans (in U.S. dollars) continued decreasing in the first half of 2022 (-4.8%).

- Customer deposits under management (67% of the area's total liabilities as of June 30, 2022) remained the main source of funding for the balance sheet and increased by 26.6%. Especially noteworthy is the positive performance of Turkish lira time deposits (+51.3%), which represent a 72.1% of total customer deposits in local currency, as well as demand deposits (+45.5%). Foreign currency deposits (in U.S. dollars) decreased by 11.1%. For its part, the evolution of off-balance sheet funds (+43.8%) also stood out.

The most relevant of the evolution of the area's activity in the second quarter of 2022 has been:

- Lending activity (performing loans under management) was above the previous quarter (+13.4%) thanks to the similar dynamism of the evolution as observed during the first six months of 2022: positive evolution of the Turkish lira loans, highlighting consumer loans (+15.3%),credit cards (+21.7%) and, especially, business loans (+18.6%).

- In terms of asset quality, the NPL ratio decreased by 78 basis points compared to the end of March 2022 to 5.9%, due to increased activity in the quarter, especially in Turkish lira loans, together with NPL flows where the entries of individualized cases were offset by recoveries and, retail portfolio sales. The NPL coverage ratio improved to 83% as of June 30, 2022.

- Total funds under management showed a positive quarterly evolution (+13.6%), highlighting the growth of local currency time and demand deposits (+14.0% and +23.4%, respectively), as well as the growth of off-balance sheet funds (+18.5%).

Results

Turkey generated a net attributable profit of €62m between January and June 2022. This result includes the application of accounting for hyperinflation in Turkey in the second quarter of 2022, with effect from January 1 of the same year, which includes, among others, the loss of the net monetary position for a gross import of €-1,686m, partially offset by the gross impact of income derived from inflation-linked bonds (CPI linkers) for €+1,132m, both recorded in the "Other operating income and expenses" line, and includes the impact from the application of the spot exchange rate as of June 30, 2022. It also includes the effect on the result attributed to the Group after the acquisition of 1,517,195,890 shares equivalent to 36.12% of the share capital of Garanti BBVA after the completion of the voluntary takeover bid. These results are not comparable with those from the first half of 2021, as accounting for hyperinflation has been applied since January 1, 2022.

The most significant aspects of quarterly evolution in the area's income statement were:

- Net interest income recorded significant growth (+49.0%), due to higher Turkish lira loan volumes and an increase in the customer spread.

- Net fees and commissions increased by 35.8%, mainly driven by the positive performance in payment systems, money transfers, asset management, contingent commitments and Project Finance.

- NTI performed significantly well (+40.3%), mainly due to FX trading gains, the earnings generated by the Global Markets unit, as well as gains from derivatives transactions.

- Other operating income and expenses line, which includes, among others, the aforementioned loss in value of the net monetary position due to the country's inflation rate, compares positively with the first quarter of 2022. It should be noted that said loss is partially offset by the income derived from the inflation-linked bonds (CPI linkers), which increased between April and June, in relation to those obtained in the first quarter of 2022. Apart from the above, a greater contribution from the subsidiaries of Garanti BBVA.

- Operating expenses grew by 21.7%, mainly due to higher personnel expenses.

- Impairment on financial assets decreased by 9.7% mainly due to lower requirements in the collective wholesale portfolio due to recoveries and repayments of singular clients. As a result of the above and also favored by the growth in lending activity, the accumulated cost of risk at the end of June 2022 decreased to 0.88% from the 0.99% accumulated at the end of the previous quarter.

- The provisions and other results line closed June with a higher loss than the previous quarter, mainly due to higher provisions for special funds and contingent liabilities.

Ultimately, the accumulated income tax at the end of June 2022 is affected by the application of IAS 29, generating additional adjustments to the tax expense, together with the increase in the tax rate from 23% to 25% with effect as from April 2022.