Spain

Highlights

- Growth in lending activity and stable customer funds in the quarter

- Solid asset quality indicators

- Significant improvement in efficiency

- Year-on-year decrease of impairment on financial assets during the semester

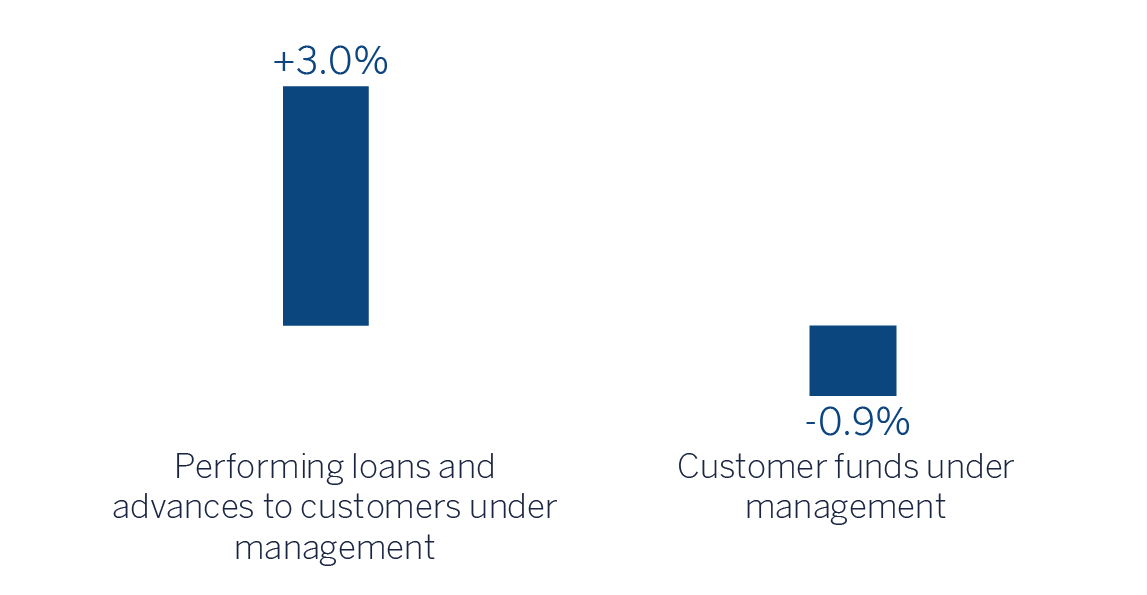

Business activity (1)

(VARIATION COMPARED TO 31-12-21)

(1) Excluding repos.

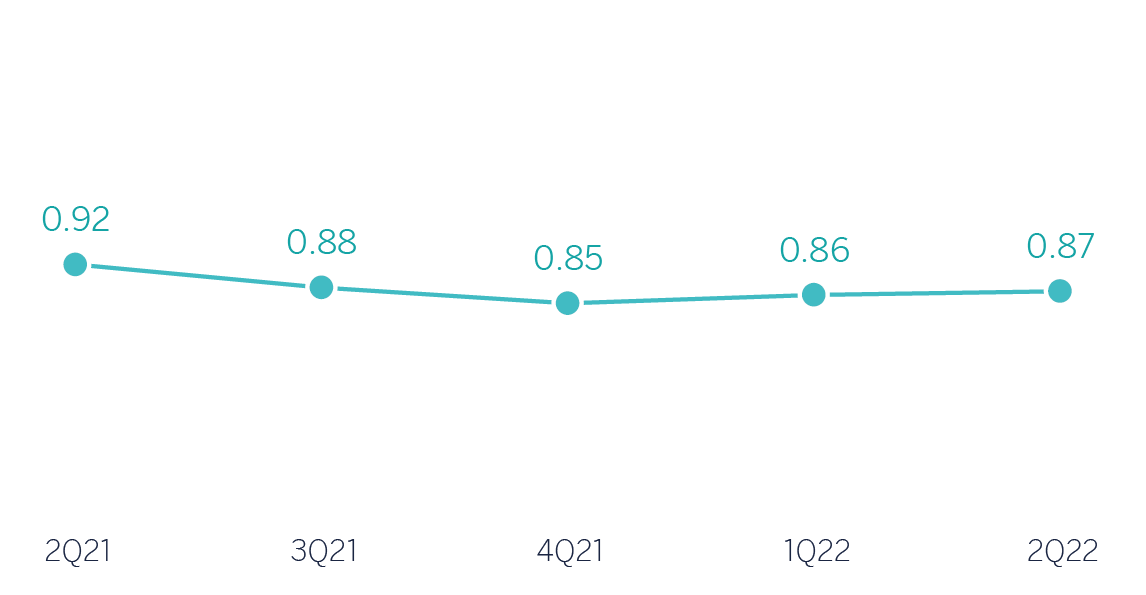

Net interest income/AVERAGE TOTAL ASSETS

(Percentage)

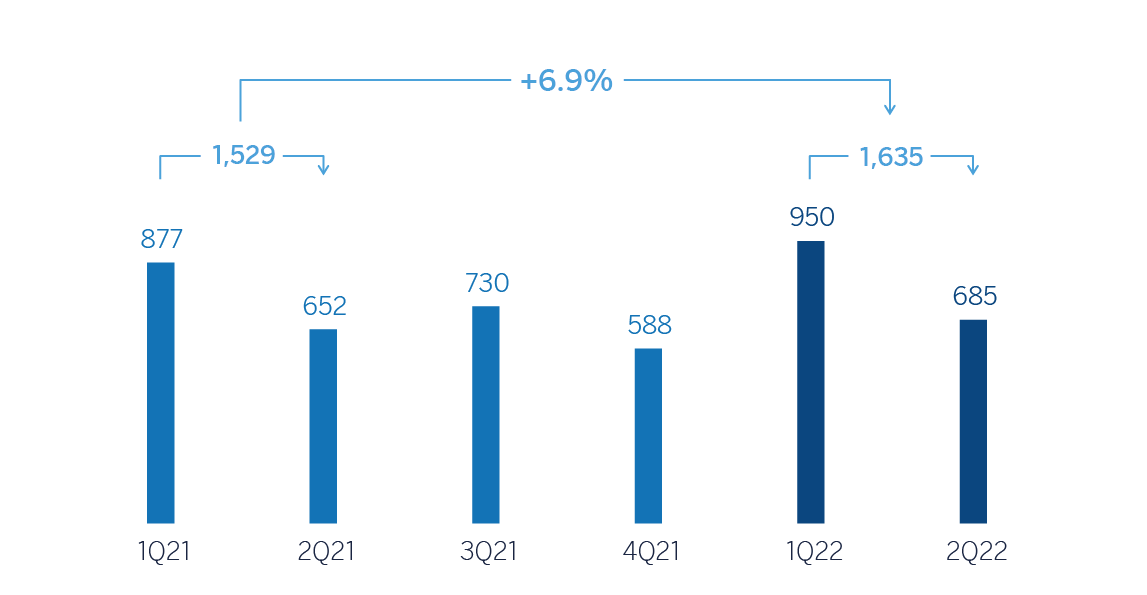

Operating income (Millions of euros)

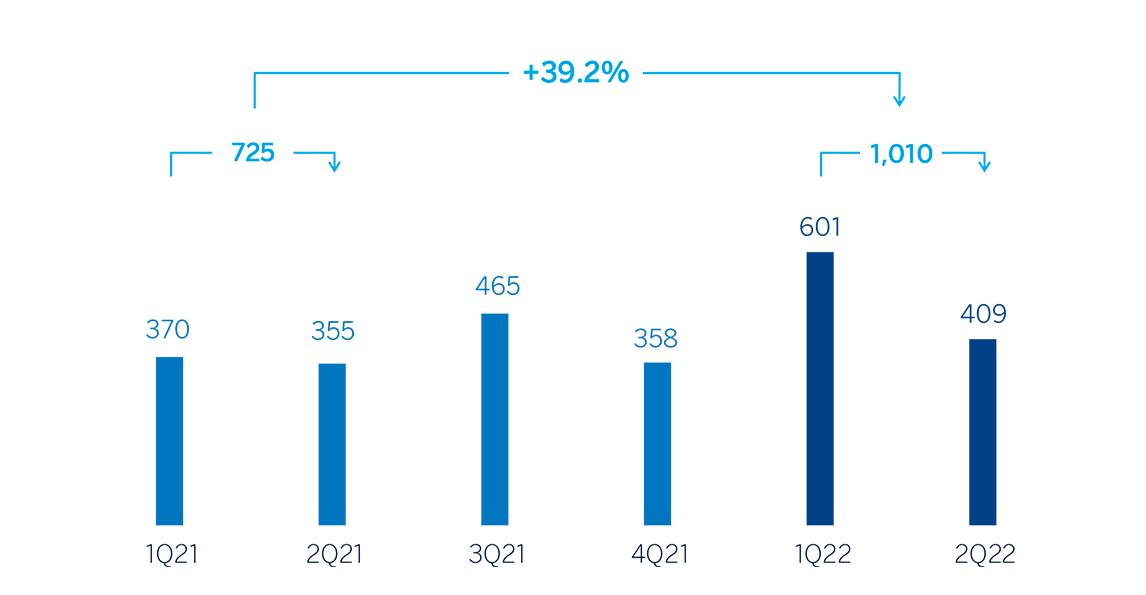

Net attributable profit (LOSS)(1) (Millions of euros)

(1) Excludes the net impact arisen from the purchase of offices in Spain in 2Q22.

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1H22 | ∆% | 1H21 (1) |

|---|---|---|---|

| Net interest income | 1,763 | 0.1 | 1,761 |

| Net fees and commissions | 1,110 | 4.6 | 1,061 |

| Net trading income | 288 | 11.2 | 259 |

| Other operating income and expenses | (92) | 98.9 | (46) |

| Of which: insurance activities (2) | 194 | 7.9 | 180 |

| Gross income | 3,069 | 1.1 | 3,035 |

| Operating expenses | (1,434) | (4.8) | (1,506) |

| Personnel expenses | (768) | (9.7) | (851) |

| Other administrative expenses | (457) | 5.1 | (435) |

| Depreciation | (209) | (4.9) | (220) |

| Operating income | 1,635 | 6.9 | 1,529 |

| Impairment on financial assets not measured at fair value through profit or loss | (193) | (43.7) | (343) |

| Provisions or reversal of provisions and other results | (27) | (86.6) | (202) |

| Profit (loss) before tax | 1,414 | 43.7 | 985 |

| Income tax | (403) | 56.2 | (258) |

| Profit (loss) for the period | 1,012 | 39.2 | 727 |

| Non-controlling interests | (2) | 36.7 | (1) |

| Net attributable profit (loss) excluding non-recurring impacts | 1,010 | 39.2 | 725 |

| Net impact arisen from the purchase of offices in Spain | (201) | - | - |

| Net attributable profit (loss) | 808 | 11.5 | 725 |

- (1) Restated balances. For more information, please refer to the “Business Areas” section.

- (2) Includes premiums received net of estimated technical insurance reserves.

| Balance sheets | 30-06-22 | ∆% | 31-12-21 |

|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 37,732 | 43.0 | 26,386 |

| Financial assets designated at fair value | 140,377 | (3.6) | 145,546 |

| Of which: Loans and advances | 41,721 | (17.6) | 50,633 |

| Financial assets at amortized cost | 204,749 | 2.6 | 199,646 |

| Of which: Loans and advances to customers | 176,109 | 2.9 | 171,081 |

| Inter-area positions | 39,466 | 16.2 | 33,972 |

| Tangible assets | 2,973 | 17.3 | 2,534 |

| Other assets | 6,714 | 25.6 | 5,346 |

| Total assets/liabilities and equity | 432,012 | 4.5 | 413,430 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 89,119 | 9.5 | 81,376 |

| Deposits from central banks and credit institutions | 62,815 | 14.7 | 54,759 |

| Deposits from customers | 211,023 | 2.1 | 206,663 |

| Debt certificates | 36,805 | (3.7) | 38,224 |

| Inter-area positions | - | - | - |

| Other liabilities | 17,745 | (3.6) | 18,406 |

| Regulatory capital allocated | 14,505 | 3.6 | 14,002 |

| Relevant business indicators | 30-06-22 | ∆% | 31-12-21 |

|---|---|---|---|

| Performing loans and advances to customers under management (1) | 173,268 | 3.0 | 168,235 |

| Non-performing loans | 8,378 | (0.9) | 8.450 |

| Customer deposits under management (1) | 210,533 | 2.2 | 205,908 |

| Off-balance sheet funds (2) | 86,828 | (7.7) | 94,095 |

| Risk-weighted assets | 109,821 | (3.5) | 113,797 |

| Efficiency ratio (%) | 46.7 | 51.7 | |

| NPL ratio (%) | 4.0 | 4.2 | |

| NPL coverage ratio (%) | 61 | 62 | |

| Cost of risk (%) | 0.20 | 0.30 |

- (1) Excluding repos.

- (2) Includes mutual funds, customer portfolios and pension funds.

Macro and industry trends

Economic activity has been quite dynamic in the first half of the year, despite the war in Ukraine. However, this has put upward pressure on energy and food prices, contributing to a rise in inflation to 10.2% in June. According to BBVA Research, GDP is expected to grow by 4.1% this year, unchanged from the previous forecast. Although GDP fell short of expectations in the first quarter, the latest data points to a better-than-expected performance in the second quarter. The interest rate hikes by the ECB and the global and European slowdown are expected to moderate the economy, and GDP growth in 2023 would be around 1.8%. Inflation will remain high and above the ECB target of 2%, especially in 2022 but also in 2023 (averaging around 7,9% in 2022 and 3.2% in 2023).

With regard to the banking system, credit to the private sector increased slightly by 0.6% year-on-year as of April 2022, following an overall decrease of 0.1% in 2021. The non-performing loan ("NPL") ratio continued to fall and stood at 4.19% in April 2022, 34 basis points lower than April 2021 and 10 basis points better than end-2021. The system also maintains comfortable solvency and liquidity levels.

Activity

The most relevant aspects related to the area's activity during the first half of 2022 were:

- Lending activity (performing loans under management) was higher than at the end of 2021 (+3.0%), due largely to the growth in business segments, especially loans to SMEs (+7.6%) and companies (+4.2%), to institutions belonging to the public sector (+9.8%) and higher consumer balances (+4.1%, including credit cards).

- Total customer funds decreased -0.9% compared to 2021 year-end. In the first half of the year, off-balance sheet funds recorded a decrease of 7.7%, mainly due to the negative effect of the markets evolution. For its part, the balance of customer deposits under management increased by 2.2% between January and June with the following breakdown by product: demand deposits grew by 3.4%, compensating for the drop in time deposits (-10.1%).

The most relevant of the evolution of the area's activity in the second quarter of 2022 has been:

- Lending activity was above the previous quarter (+2.5%), fostered by the growth in public sector institutions (+11.9%), business segments (+3.5%) and consumer loans (+3.4%, including credit cards).

- With regard to asset quality, the NPL ratio decreased 14 basis points in the quarter to 4.0% mainly due to the increase in activity, supported by a slight reduction in non-performing loans. In terms of coverage, the ratio remained stable in the quarter at 61%.

- Total customer funds remained stable between April and June (+0.2%). By products, growth in demand deposits (+2.5%) and reduction in off-balance sheet funds (-4.4%), affected by the unfavorable evolution of the markets, and in time deposits (-1.0%).

Results

Spain generated a net attributable profit of €1,010m during the first half of 2022, up 39.2% from the result achieved during the first half of the previous year, due to the strength of the gross income, driven by commissions and the significant reduction in personnel expenses, as well as lower loan-loss provisions and provisions. This result does not include the net impact of €-201m from the purchase of offices from Merlin. If this impact is taken into account, the cumulative attributable result of the area at the end of June 2022 stands at €808m, 11.5% above the attributable result for the same period of the previous year.

The most notable aspects of the year-on-year changes in the area's income statement at the end of June 2022 were:

- Net interest income registered a slight year-on-year increase of 0.1%, mainly as a result of better performance of the portfolios. The area's net interest income increased by 5.2% between April and June, mainly due to a better investment performance, reflecting a more favorable interest rate environment.

- Fees and commissions had a positive performance (+4.6% year-on-year), mainly favored by a greater contribution from fees and commissions associated with banking services and, to a lesser extent, from insurance revenues.

- NTI at the end of June 2022 was 11.2% above the one achieved in the same period of the previous year, due in part to the greater contribution of the Global Markets area.

- The other operating income and expenses line compares negatively to the first half of the previous year, mainly due to the higher contribution to the SRF, which offset the good performance of the insurance business.

- Operating expenses were lower than at the end of the first half of 2021 (-4.8% in year-on-year terms), mainly due to lower personnel expenses as a result of the staff reduction.

- As a result of gross income growth and the declined expenses, the efficiency ratio stood at 46.7%, representing a significant improvement compared to the 49.6% recorded at the end of June 2021.

- Impairment on financial assets was 43.7% below the first half of 2021, due to the good performance of the underlying asset in the first half of 2022. As a result, the accumulated cost of risk at the end of June 2021 stood at 0.20%.

- The provisions and other results line closed the first half of the year at €-27m, which positively compares with last year, due to, among other factors, the higher results from real estate assets and lower provisions for off-balance sheet risks compared to the same period in 2021.

In the second quarter of 2022, Spain generated a net attributable profit of €409m (-31.9% compared to the previous quarter). The recurring income grew between April and June, even if the evolution has been mainly affected by the contribution to the SRF made in the quarter together with a lower NTI. If the net impact of the purchase of offices from Merlin is included, the area's net attributable profit stands at €208m.