Spain

Highlights

- Growth in lending activity throughout the year

- Favorable performance of recurring income, driven by commissions

- Improvement in the efficiency ratio and outstanding gross income growth

- Decrease in impairment on financial assets, compared to a 2020 that was strongly affected by the pandemic, resulting in a lower cost of risk

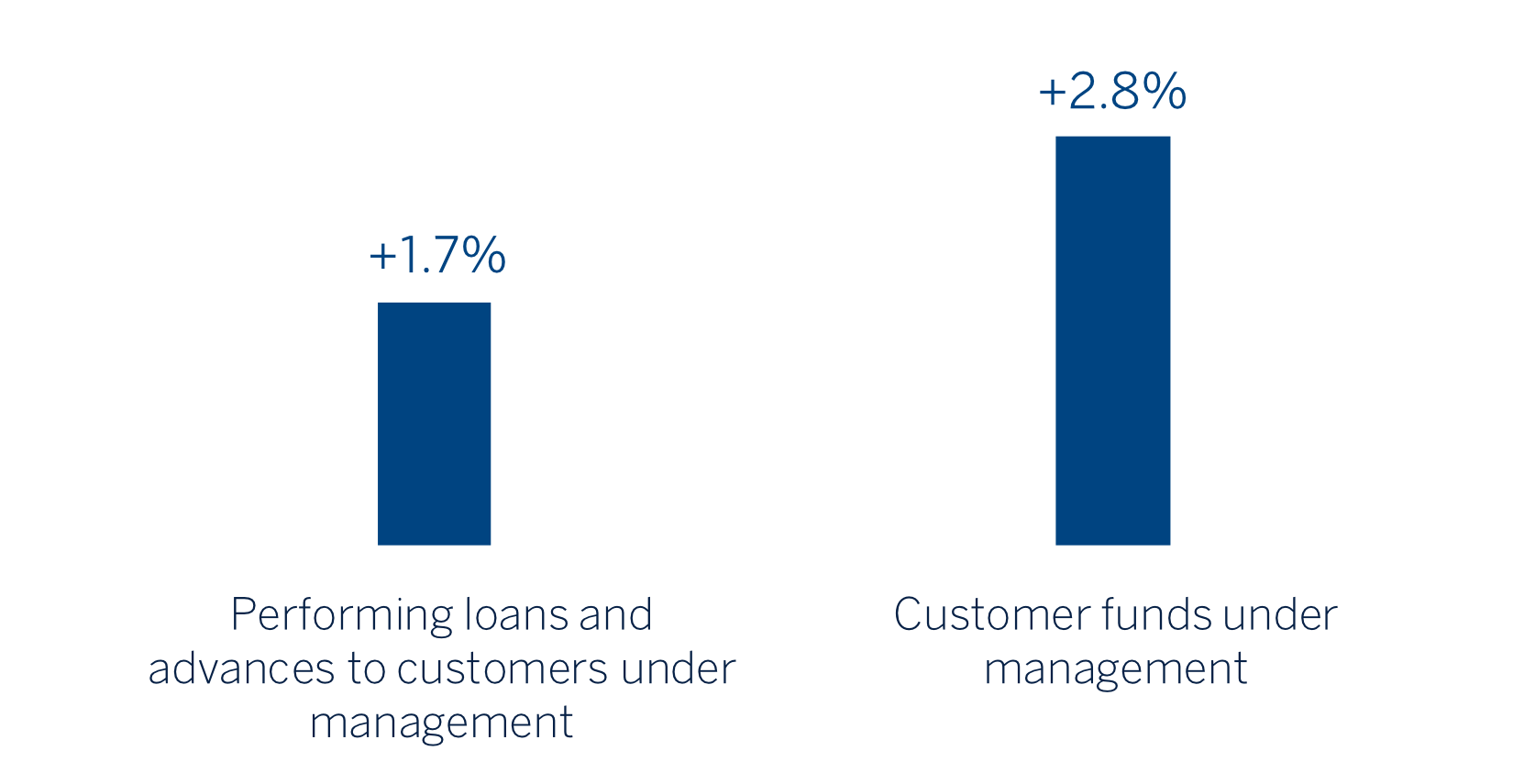

Business activity (1)

(VARIATION COMPARED TO 31-12-20)

(1) Excluding repos.

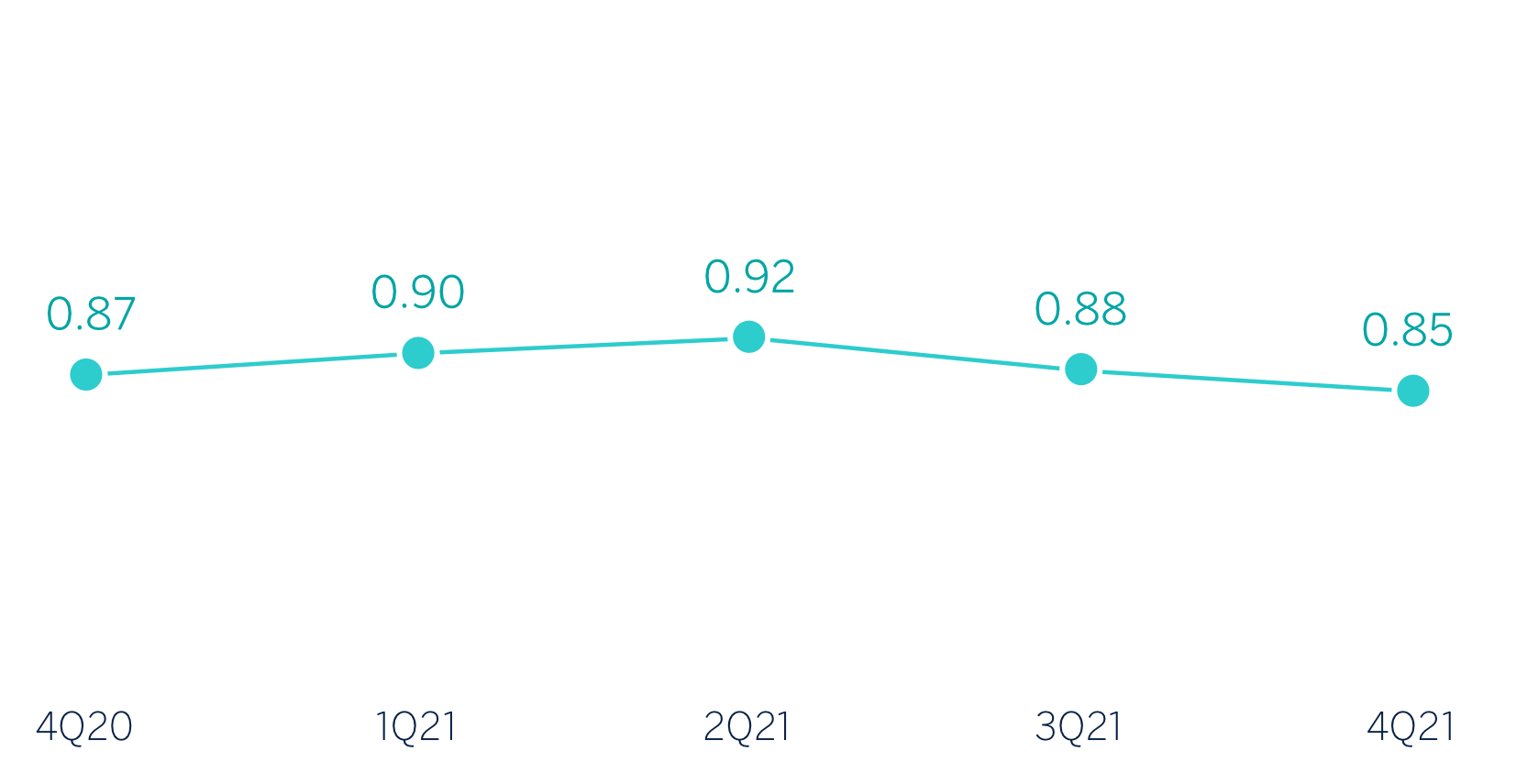

Net interest income/ATAs

(Percentage)

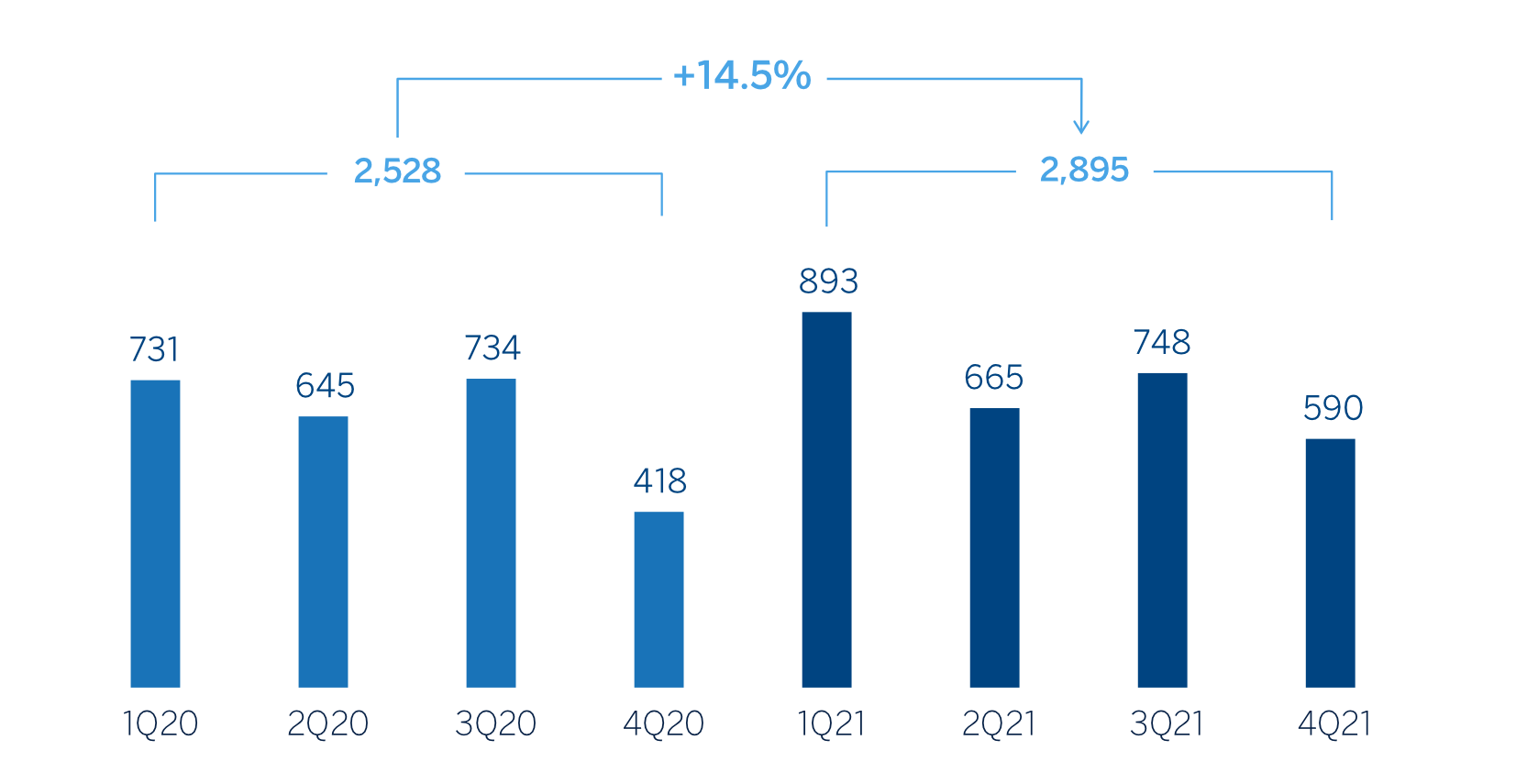

Operating income (Millions of euros)

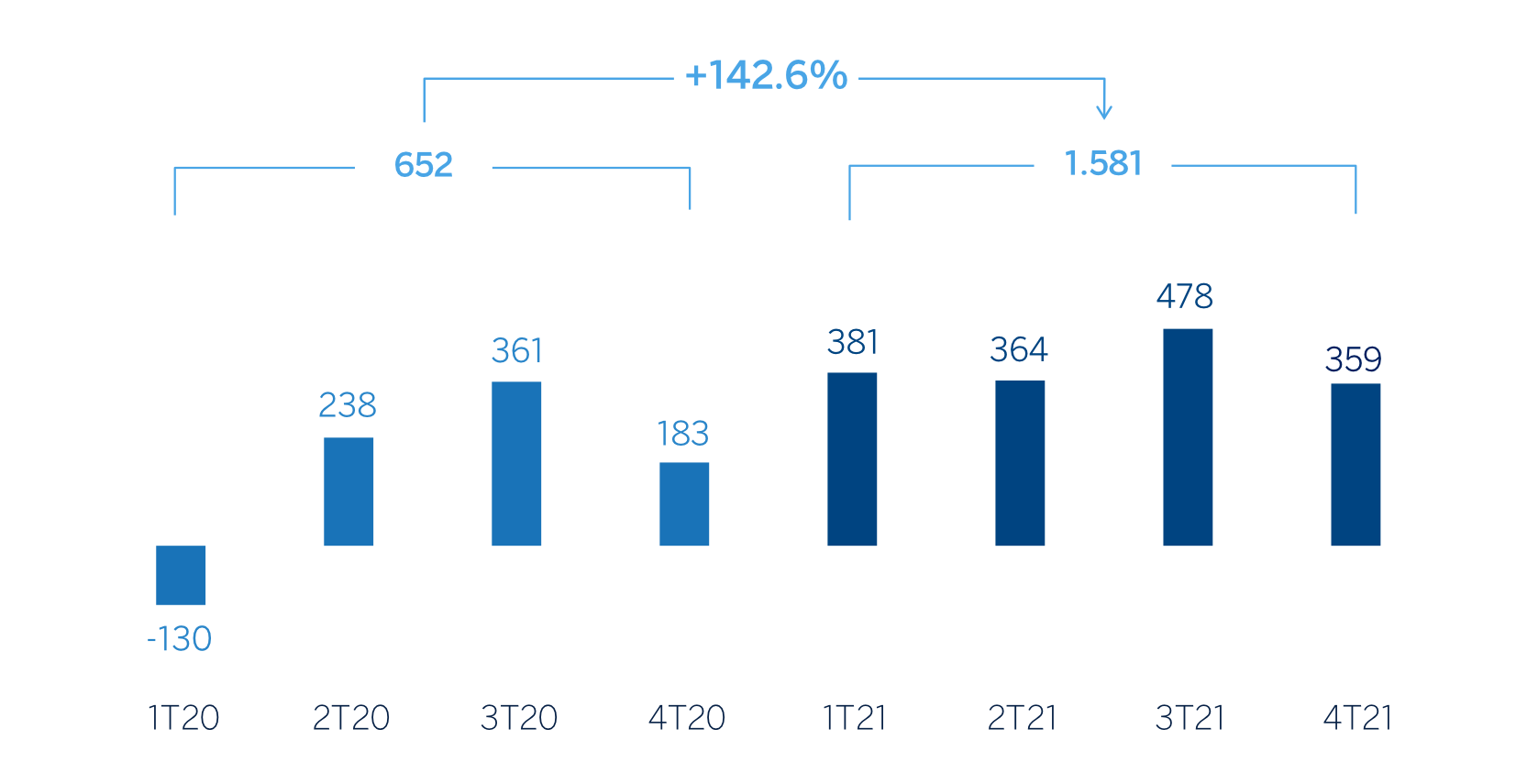

Net attributable profit (LOSS) (Millions of euros)

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 2021 | ∆% | 2020 |

|---|---|---|---|

| Net interest income | 3,502 | (1.8) | 3,566 |

| Net fees and commissions | 2,189 | 21.5 | 1,802 |

| Net trading income | 343 | 97.4 | 174 |

| Other operating income and expenses | (109) | n.s. | 25 |

| Of which insurance activities (1) | 357 | (23.2) | 465 |

| Gross income | 5,925 | 6.4 | 5,567 |

| Operating expenses | (3,030) | (0.3) | (3,039) |

| Personnel expenses | (1.738) | - | (1,738) |

| Other administrative expenses | (861) | 2.3 | (841) |

| Depreciation | (431) | (6.3) | (460) |

| Operating income | 2,895 | 14,5 | 2,528 |

| Impairment on financial assets not measured at fair value through profit or loss | (503) | (56.9) | (1,167) |

| Provisions or reversal of provisions and other results | (270) | (49.8) | (538) |

| Profit (loss) before tax | 2,122 | 157.9 | 823 |

| Income tax | (538) | 221,7 | (167) |

| Profit (loss) for the year | 1,584 | 141.6 | 655 |

| Non-controlling interests | (2) | (32.5) | (3) |

| Net attributable profit (loss) | 1,581 | 142,6 | 652 |

- (1) Includes premiums received net of estimated technical insurance reserves.

| Balance sheets | 31-12-21 | ∆% | 31-12-20 |

|---|---|---|---|

| Cash, cash balances at central banks and other demand deposits | 26,386 | (31.2) | 38,356 |

| Financial assets designated at fair value | 145,544 | 7.3 | 137,969 |

| Of which: Loans and advances | 50,631 | 78.9 | 28,301 |

| Financial assets at amortized cost | 199,663 | 0.8 | 198,173 |

| Of which: Loans and advances to customers | 171,097 | 1.8 | 167,998 |

| Inter-area positions | 34,005 | 28.4 | 26,475 |

| Tangible assets | 2,534 | (12.7) | 2,902 |

| Other assets | 5,346 | (18.2) | 6,535 |

| Total assets/liabilities and equity | 413,477 | 1.3 | 408,030 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 81,376 | 13.7 | 71,542 |

| Deposits from central banks and credit institutions | 54,759 | (6.8) | 58,783 |

| Deposits from customers | 206,663 | 0.1 | 206,428 |

| Debt certificates | 38,224 | (6.8) | 41,016 |

| Inter-area positions | - | - | - |

| Other liabilities | 18,453 | 8.8 | 16,955 |

| Regulatory capital allocated | 14,002 | 5.2 | 13,306 |

| Relevant business indicators | 31-12-21 | ∆% | 31-12-20 |

|---|---|---|---|

| Performing loans and advances to customers under management (1) | 168,251 | 1.7 | 165,511 |

| Non-performing loans | 8.450 | 1.3 | 8,340 |

| Customer deposits under management (1) | 205,908 | 0.0 | 205,809 |

| Off-balance sheet funds (2) | 70.072 | 11.7 | 62,707 |

| Risk-weighted assets | 113,825 | 9.0 | 104,388 |

| Efficiency ratio (%) | 51.1 | 54.6 | |

| NPL ratio (%) | 4.2 | 4.3 | |

| NPL coverage ratio (%) | 62 | 67 | |

| Cost of risk (%) | 0.30 | 0.67 |

- (1) Excluding repos.

- (2) Includes mutual funds and pension funds.

Macro and industry trends

The economic recovery continued in the fourth quarter of 2021, despite the negative impact on activity of the increased infections caused by new variants of the COVID-19. Activity indicators for the fourth quarter suggest a dynamism that could offset, at least partially, the impact on GDP in 2021 of the lower growth in the third quarter (2.6% quarterly) compared to the initial forecast by BBVA Research. According to estimates by BBVA Research, GDP would grow by around 5.1% in 2021, after a fall of 10.8% in 2020, and could increase by 5.5% in 2022 if European funds are used in a timely manner. Inflation continued to accelerate (in December 2021 it stood at 6.5%), driven mainly by energy prices, but will moderate in 2022, according to estimates by BBVA Research.

With regard to the banking system, with data as of the end of October 2021, the volume of lending to the private sector recorded a decline of 0.8% since December 2020, following growth of 2.6% in 2020. The NPL ratio continued to improve, reaching 4.36%, also at the end of October 2021 (4.51% at 2020 year-end). In addition, it should be noted that the system maintained comfortable levels of solvency and liquidity.

Activity

The most relevant aspects related to the area's activity during 2021 were:

- Lending activity (performing loans under management) was higher than at the end of 2020 (+1.7%) mainly due to growth in loans to SMEs (+10.2%), consumer loans (+9.1% including credit cards) and the increased activity of CIB in the fourth quarter of 2021 (+1.1 % year-on-year),

- With regard to asset quality, the non-performing loan ratio increased by 13 basis points in the quarter to stand at 4.2%, mainly due to the increase in non-performing loans, resulting from the reclassification due to the implementation of the aforementioned new definition of default. As a result of this increased balance of non-performing loans, the area's NPL coverage ratio is reduced to 62% as of December 31, 2021.

- Total customer funds increased (+2.8%) compared to 2020 year-end, supported by the favorable performance of off- balance sheet funds (+11.7%). For its part, the balance of customer deposits under management was stable during the year (0.0%), as the increase in deposits held by retail customers was offset by the decrease in the balances held by wholesale customers. By product, demand deposits grew by 7.4%, compensating for the drop in time deposits (-41.6%).

The most relevant aspects related to the area's activity in the fourth quarter of 2021 were:

- Lending activity (performing loans under management) was higher that in the previous quarter (+1.4%), with the same growth dynamics as reported in the year-on-year trend: growth in the SME segments (+3.7%), consumer loans and credit cards (+2.6 %) and, in particular, in CIB, which continued the upward trend of the previous quarter and grew by 5.8%.

- Total customer funds increased compared to the previous quarter (+3.5%), thanks to the seasonal growth in demand deposits (+5.0%), which compensated for the decrease in time deposits (-12.8%) and also supported by the favorable performance of off-balance sheet funds (+4.4%).

Results

Spain generated a net attributable profit of €1,581m during 2021, up 142.6% from the result posted in the previous year, mainly due to the increased provisions for impairment on financial assets as a result of the COVID-19 outbreak and the provisions made, in both cases in 2020, as well as the increased contribution from fees and commissions revenues and NTI in 2021.

The most notable aspects of the year-on-year changes in the area's income statement at the end of December 2021 were:

- Net interest income decreased by 1.8%, mainly due to the effect of the declining interest rates environment on the stock of loans and the lower contribution of the ALCO portfolios, which were partially offset by lower financing costs.

- Net fees and commissions continued to show a very positive performance (+21.5% year-on-year), mainly favored by a greater contribution from banking services, revenues associated with asset management and the contribution of insurance, in the latter case, by the bancassurance operation with Allianz.

- NTI showed at the end of December 2021 a significant year-on-year growth of 97.4%, mainly due to the results of the Global Markets unit.

- The other operating income and expenses line performed poorly compared to the previous year, due to the lower contribution from the insurance business in this line due to the bancassurance operation with Allianz and the higher contribution to the Single Resolution Fund.

- Operating expenses remained under control (-0.3% in year-on-year terms).

- As a result of gross income growth and contained expenses, the efficiency ratio stood at 51.1%, representing a significant improvement compared to 54.6% recorded at the end of December 2020.

- Impairment on financial assets recorded a significant reduction compared to the amount accumulated during 2020, mainly due to the negative impact of the worsening macroeconomic scenario caused by the pandemic following the outbreak of COVID-19 in March 2020, as well as the improvement of said scenario in 2021. For its part, the accumulated cost of risk remained on a downward trend and stood at 0.30% as of December 31, 2021.

- The provisions and other results line closed at €-270m, which was well below the €-538m recorded in the same period last year, which included provisions for potential claims.

In the fourth quarter of 2021, Spain generated a net attributable profit of €359m (-24.9% compared to the previous quarter). The performance is influenced by the contribution to the DGF made during the last three months of 2021, as well as by higher provisions for impairment on financial assets and growth in operating expenses. This was partially offset by higher fees and NTI together with an improved performance of the provisions and other results line.