Other information: Corporate & Investment Banking

Highlights

- Leadership position in green and sustainable loans.

- Good performance of net interest income.

- Net attributable profit impacted by lower net trading income and higher impairments on financial assets.

Business activity (1)

(Year-on-year change at constant exchange rates. Data as of 30-06-2019)

(1) Excluding repos.

Gross income/ATAs

(Percentage. Constant exchange rates)

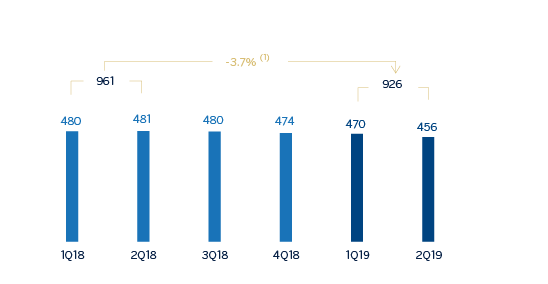

Operating income

(Millions of euros at constant exchange rates)

(1) At current exchange rate: -8.0%.

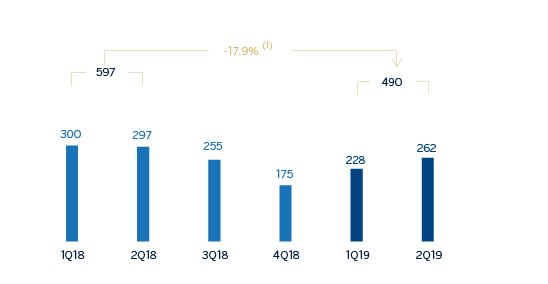

Net attributable profit

(Millions of euros at constant exchange rates)

(1) At current exchange rate: -19.0%.

Financial statements and relevant business indicators (Millions of euros and percentage)

| Income statement | 1H19 | ∆% | ∆% (1) | 1H18 |

|---|---|---|---|---|

| Net interest income | 769 | 14.9 | 20.1 | 669 |

| Net fees and commissions | 344 | (8.8) | (7.1) | 377 |

| Net trading income | 365 | (27.0) | (25.0) | 500 |

| Other operating income and expenses | (27) | 46.5 | 38.7 | (18) |

| Gross income | 1.451 | (5.1) | (1.8) | 1.528 |

| Operating expenses | (525) | 0.7 | 1.7 | (522) |

| Personnel expenses | (236) | 3.6 | 4.1 | (228) |

| Other administrative expenses | (226) | (5.7) | (3.9) | (239) |

| Depreciation | (64) | 16.4 | 15.8 | (55) |

| Operating income | 926 | (8.0) | (3.7) | 1.007 |

| Impairment on financial assets not measured at fair value through profit or loss | (77) | n.s. | n.s. | 9 |

| Provisions or reversal of provisions and other results | 17 | n.s. | n.s. | (21) |

| Profit/(loss) before tax | 866 | (12.9) | (10.0) | 994 |

| Income tax | (211) | (19.8) | (17.6) | (263) |

| Profit/(loss) for the year | 655 | (10.4) | (7.3) | 732 |

| Non-controlling interests | (166) | 30.7 | 50.3 | (127) |

| Net attributable profit | 490 | (19.0) | (17.9) | 605 |

- (1) Figures at constant exchange rates.

| Balance sheets | 30-06-19 | ∆% | ∆% (1) | 31-12-18 |

|---|---|---|---|---|

| Cash. cash balances at central banks and other demand deposits | 4,841 | (4.8) | (5.4) | 5,087 |

| Financial assets designated at fair value | 108,378 | 17.3 | 16.8 | 92,391 |

| Of which Loans and advances | 37,486 | 30.0 | 30.0 | 28,826 |

| Financial assets at amortized cost | 67,297 | 3.3 | 3.8 | 65,167 |

| Of which loans and advances to customers | 58,069 | (1.1) | (0.6) | 58,720 |

| Inter-area positions | - | - | - | - |

| Tangible assets | 75 | 161.0 | 161.7 | 29 |

| Other assets | 1,889 | (13.3) | (15.3) | 2,179 |

| Total assets/liabilities and equity | 182,481 | 10.7 | 10.6 | 164,852 |

| Financial liabilities held for trading and designated at fair value through profit or loss | 94,045 | 28.5 | 28.4 | 73,163 |

| Deposits from central banks and credit institutions | 16,398 | (15.8) | (16.5) | 19,464 |

| Deposits from customers | 33,970 | (21.1) | (21.2) | 43,069 |

| Debt certificates | 2,986 | 54.6 | 54.0 | 1,931 |

| Inter-area positions | 27,298 | 38.3 | 39.6 | 19,742 |

| Other liabilities | 4,097 | (5.8) | (6.5) | 4,348 |

| Economic capital allocated | 3,687 | 17.6 | 16.8 | 3,136 |

- (1) Figures at constant exchange rates.

| Relevant business indicators | 30-06-19 | ∆% | ∆% (1) | 31-12-18 |

|---|---|---|---|---|

| Performing loans and advances to customers under management (2) | 57,289 | (2.6) | (2.1) | 58,796 |

| Non-performing loans | 1,107 | 45.3 | 49.0 | 762 |

| Customer deposits under management (2) | 33,945 | (14.4) | (14.2) | 39,642 |

| Off-balance sheet funds (3) | 1.306 | 31.6 | 31.4 | 993 |

| Efficiency ratio (%) | 36 | 34 |

- (1) Figures at constant exchange rates.

- (2) Excluding repos.

- (3) Includes mutual funds. pension funds and other off-balance sheet funds.

Activity

Unless expressly stated otherwise, all the comments below on rates of change, for both activity and results, will be given at constant exchange rates. These rates, together with changes at current exchange rates, can be found in the attached tables of financial statements and relevant business indicators. In addition, the quarterly variations are from the quarter ending with respect to the previous quarter.

The most relevant aspects of the evolution of the area's activity in the first half of 2019 were:

- Margin pressure and excess liquidity in the market persists. Lending activity (performing loans under management) fell by 2.1% compared to the end of December 2018 and remained flat year-on-year (down 0.4%).

- Customer funds fell 13.1% in the first half of 2019 (down 6.8% year-on-year), mainly due to the decline in time deposits.

- During the first half of 2019, BBVA was one of the most active financial institutions in sustainability and digitalization, two processes that the Bank wants to continue to promote together with its customers.

- In sustainable finance, the Bank was involved in 19 green transactions and/or transactions linked to a sustainability criteria (ESG scores, environmental and social indicators), certified by renowned independent consultants, compared to a total of 23 transactions in the whole of 2018. In addition to Spain, where a second green bond was issued, BBVA led major transactions in the United Kingdom, France, Portugal, Belgium and China in various sectors including hotelier, energy (gas and electricity), recycling and automotive components, among others. Of these 19 transactions, 11 were led by BBVA as a sustainability coordinator.

- In terms of innovation, following the recognition of financing via blockchain in 2018, BBVA was a pioneer in linking a company's degree of digitization to its bank financing with the so-called digital loan or D-loan. The syndicated loan, placed in Asia and led by BBVA, is the first of its kind worldwide, and demonstrates that the Bank remains at the forefront of innovative solutions for its customers.

Results

CIB registered net attributable profit of €490m in the first half of 2019, down 17.9% year-on-year. The most relevant aspects of the year-on-year changes in the income statement for Corporate & Investment Banking are summarized below:

- Net interest income increased (up 20.1% year-on-year) as a result of a strong performance in all geographic areas (especially Spain, Rest of Eurasia, Turkey and South America).

- Net fees and commissions continued to fall due to a decreasing number of one-off transactions (down 7.1% year-on-year, up 3.1% compared to the first quarter of 2019).

- NTI decreased by 25.0% year-on-year, mainly in Spain, due to the fall in interest rates to record lows, which was partially offset by the strong performance in South America and, to a lesser extent, Turkey thanks to a very positive first quarter.

- As a result, gross income fell slightly in the first half of 2019 (down 1.8% year-on-year, down 1.6% in the quarter).

- Efficient management of operating expenses, which increased by 1.7% year-on-year (up 0.7% compared to the first quarter of 2019) associated, in part, with investment in various technology projects.

- Impairment on financial assets increased, mainly due to higher loan-loss provisions from specific customers in Spain, Eurasia, the United States and South America, which was partially offset by lower provisions in Mexico and Turkey.