The advanced internal model quantifies capital at a confidence level of 99.9% following the LDA methodology (Loss Distribution Approach). This methodology estimates the distribution of losses by operational event by convoluting the frequency distribution and the loss given default distribution of these events.

The calculations have been made using internal data on the Group’s historic losses as its main source of information. To enrich the data from this internal database and to take into account the impact of possible events not yet considered therein, external databases (ORX consortium) have been used and the scenarios indicated in point 6.4.3.4 have also been included.

The distribution of losses is constructed for each of the different types of operational risk, which are defined as per Basel Accord cells; i.e. a cross between business line and risk class. In those cases in which there is not sufficient data for a sound analysis, it becomes necessary to undertake cell aggregations, and to do so the business line is chosen as the axis.

In certain cases, a greater disaggregation of the Basel cell has been selected. The objective consists of identifying statistically homogenous groups and a sufficient amount of data for proper modeling. The definition of these groupings is regularly reviewed and updated.

Solvency regulations establish that regulatory capital for operational risk is determined as the sum of individual estimates by type of risk, but allowing the option of incorporating the effect of the correlation among them. This impact has been taken into consideration in BBVA estimates with a conservative approach.

The model of calculating capital in both Spain and Mexico incorporates factors that reflect the business environment and situation of internal control systems. Thus the calculation obtained is higher or lower according to how these factors change in anticipating the result.

As regards other factors considered in the solvency regulations, current estimates do not include the mitigating effect of insurance.

The tables below show the operational risk capital requirements broken down according to the calculation models used and by geographical area, to provide a global vision of capital consumption for this type of risk:

TABLE 53: Regulatory capital for Operational Risk

(Millions of euros)

| Regulatory capital for operational risk | 2014 | 2013 |

|---|---|---|

| Advanced | 1,266 | 1,310 |

| Spain | 811 | 796 |

| Mexico | 455 | 514 |

| Standardized | 942 | 975 |

| Basic | 145 | 136 |

| BBVA Group total | 2,352 | 2,421 |

The main variations in the capital requirements for operational risk are due to:

- Advanced measurement approach (€44 million): Reduction in the requirements for the implementation of methodological changes in the AMA approach, taking into account scenarios instead of factors from the operational risk assessment tool (EVRO).

- Non-advanced approaches (€24 million): Decrease due to the combined effect of the exchange rate (mainly the devaluation of the Venezuelan currency) and the reduction in net interest income.

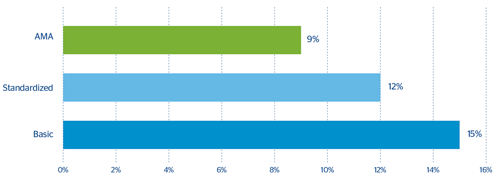

The percentages of capital required for each approach is summarized below; the average percentage of capital required on net interest income stands at 9.9%.

CHART 25: Capital required by approach