On January 1, 2014, the CRD-IV package entered into force, made up of a Directive (Directive 2013/36/EU) and a Regulation (Regulation 575/2013/EU). It represents the implementation at European level of the recommendations of the Basel Committee, known as Basel III. The Directive must be transposed by the Member States, while the Regulation is directly applicable. The two instruments replace Directive 2006/48/EC, of June 14, relating to the taking up and pursuit of the business of credit institutions, and Directive 2006/49/EC, of June 14, on the capital adequacy of investment firms and credit institutions, of the European Parliament and of the Council. Between them they constitute what we will below cite as the Solvency Regulations.

On the domestic front, with the aim of adapting to this new regulatory environment, the government passed the Law on regulation, supervision and solvency (Law 10/2014 of June 26). This law and its implementing regulations repeal the following: Law 13/1985, of May 25, on the investment ratios, bank capital and reporting requirements of financial intermediaries; Royal Decree 216/2008 of February 15, on the capital of financial institutions; and certain articles of the Bank of Spain Circular 3/2008 of May 22.

In accordance with Regulation 575/2013/EU, financial institutions have to publish certain "Information of Prudential Relevance" with the content required in Part 8 of the Regulation. The requirements laid out in the Regulation are directly applicable to Member States. This report has therefore been drawn up in keeping with these requirements.

In accordance with the policy defined by the Group for drawing up the Information of Prudential Relevance, the content of this report refers through December 31, 2014 and was approved by the Group’s Audit and Compliance Committee at its meeting held on February 23, 2015, having previously been reviewed by the External Auditor. This review has not revealed any material discrepancies concerning compliance with the reporting requirements laid down in Part 8 of Regulation 575/2013/EU.

Regulatory environment in 2014

Legal changes in the Community area

European Commission / European Parliament / European Council

In December 2010 the Committee on Banking Supervision published the document "Basel III: A global regulatory framework for more resilient banks and banking systems," in order to improve the sector's ability to withstand the impacts arising from financial and economic crises.

Since then, the European Union has worked to incorporate these Basel recommendations. After two years of negotiations, the so-called CRD-IV was published on June 27, 2013 in the Official Journal of the European Union. CRD-IV consists of a Directive that replaces capital Directives 2006/48 and 2006/49 and a common Regulation (575/2013). These Directives require transposition, while the Regulation is directly applicable.

Transposition to national law began on November 29, 2013 with the publication of the Royal Decree-Law 14/2013 adapting Spanish law to the European Union law with respect to the supervision and solvency of financial institutions. It has continued with the approval of the Law on the regulation, supervision and solvency of financial institutions.

This Law recasts the main laws governing the regulation and discipline of credit institutions into a single text. It is a single legal text that not only transposes the law recently issued by the European Union, but also integrates the Spanish laws regulating these matters.

Since January 1, 2014, the BBVA Group has applied the criteria established in the European Directive and Regulation and the Spanish legislation implementing them.

The new regulations require institutions to have a higher and better quality capital level, increase capital deductions and review the requirements associated with certain assets. Unlike the previous framework, the minimum capital requirements are complemented with requirements for capital buffers and others relating to liquidity and leverage.

The capital base under CRD-IV consists mainly of the following elements:

TABLE 1: Calculation of the Capital Base according to CRD IV

| CET 1 | Common Equity Tier I |

|---|---|

| + | Capital |

| + | Reserves |

| + | Non-controlling interests up to limit when calculating |

| - | Goodwill and other intangible assets |

| - | Treasury stock |

| - | Loans financing treasury stock |

| - | DTAs for loss carry forwards |

| - | DVA |

| - | Prudent Valuation |

| - | Limits applicable to Financial Institutions + Insurance Companies + DTAS for temporary differences |

| T1 | Tier I |

| + | AT1 and preferred securities that meet calculation criteria |

| + | Remaining non-controlling interests not assessed in CET1 |

| - | Goodwill and other intangible assets for the part not deducted in CET1 |

| Total T1 | CET1 +T1 |

| T2 | Tier II |

| + | Subordinated debt under new criteria |

| + | Preferred securities not assessed in T1 |

| + | Generic Provision |

| - | Remaining non-controlling interests not assessed in CET1 and T1 |

| Capital Base | Tier I + Tier II |

The most relevant aspects affecting common equity and risk-weighted assets are summarized below.

The main impacts affecting common equity Tier I (CET1) arise in the limit used when calculating non-controlling interests and the deductions for significant and non-significant financial holdings, insurance companies and deferred taxes. Thus, deferred taxes from loss carry forwards, the provision deficit on expected loss for IRB models and the debt valuation adjustment (DVA) of derivatives will now be deducted directly from CET1.

In the calculation of the Additional Tier 1, only issues convertible into shares or redeemable at the option of the authority and subject to capital ratio triggers are calculated.

There are stricter requirements for risk-weighted assets, mainly for counterparty risk in derivatives and exposures within the financial sector.

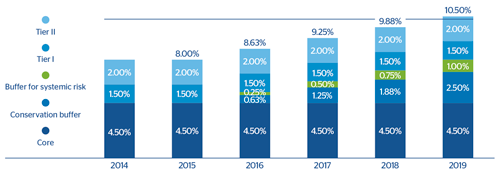

The gradual adaptation schedule detailed below has been established for compliance with the new capital ratios:

CHART 1: Schedule for gradual adaptation to CRD IV

As of December 31, 2014, according to the new CRD-IV requirements that took effect in 2014, BBVA Group's fully-loaded CET1 ratio stood at 10.4%, well over the minimum CET1 that will be required in 2019 (7%), demonstrating the Group's comfortable capital position. The phased-in CET1 ratio according to the new CRD-IV rules stood at 11.9%as of December 31, 2014.

These requirements may be increased by the counter-cyclical capital buffer requirement, the systemic bank capital buffer requirement and the systemic risk buffer requirement, should they apply and be in force (mainly starting in 2016).

The capital requirement for systemic banks is established based on the bank's systemicity, which is determined based on a number of variables that include: the bank's size, interconnection with the financial system, substitutability of the services it offers, complexity and cross-border activity.

The systemic risk capital requirement aims to prevent and mitigate possible effects associated with risks in the system that are not cyclical, as well as macroprudential risks, when the materialization of such risks may have a negative impact on the financial system itself or on the real economy.

BBVA Group is currently considered a global systemic entity according to the list prepared by the Financial Stability Board (FSB). Of the 5 possible tranches, with requirements ranging from 1% to 3.5%, BBVA Group is in the first of these tranches, with an additional requirement of 1% as a global systemic entity, applicable in fourths from 2016 to 2019.

However, as of the date referred to by the data in this report, none of those additional capital requirements for conservation, applied, i.e: the capital conservation requirement, the anticyclical capital requirement and the systemic risk requirement were 0%.

In order to provide the financial system with a metric that serves as a backstop to capital levels, irrespective of the credit risk, a measure complementing all the other capital indicators has been incorporated into Basel III and transposed to the Solvency Regulations. This measure, the leverage ratio, can be used to estimate the percentage of the assets financed with Tier 1 capital.

Although the book value of the assets used in this ratio is adjusted to reflect the bank's current or potential leverage with a given balance-sheet position, the leverage ratio is intended to be an objective measure that may be reconciled with the financial statements.

In recent months, the industry has made a significant effort to standardize both the definition and calculation of the leverage ratio and the minimum level that should be required from financial institutions to collateral that adequate levels of leverage are maintained. Although this definition and the calibration will enter into force in 2018, BBVA estimates and tracks this measure, as reported in section 10 of this report.

Other relevant changes

- Single Supervisory Mechanism (SSM): The European Central Bank(1), as the body responsible for ensuring the security and soundness of the European banking system, and for extending financial integration and stability in the euro zone, has begun a process aimed at setting up a new single financial supervision system made up of the ECB and the national competent authorities of the participating European Union countries (hereinafter, the NCAs).

With the aim of collateraling greater transparency in the balance-sheets of the affected entities, in 2014 the ECB carried out a comprehensive assessment of the entities before assuming full responsibility for supervision on November 4, 2014.

The Comprehensive Assessment, which concluded in October 2014, was based on the following pillars:

- An Asset Quality Review to improve the transparency of bank positions through an examination of the quality of the assets, including their adequacy and the assessment of the related collaterals and arrangements.

- Stress Tests aimed at determining the resilience of the banks' balance sheets.

According to the ECB exercise, BBVA had a CET1 capital level of 10.6% for the baseline scenario and 9.0% for the adverse scenario in December 2016, above the minimum levels required.

(1) http://www.ecb.europa.eu/home/html/index.en.html

The ratio for the adverse scenario is above the average for the banks analyzed by the ECB (8.3%).

BBVA would have a fully loaded CET1 capital level of 8.2% in 2016 under the adverse scenario.

The SSM, which began to operate officially in November 2014, represents a step toward greater harmonization at European level. The ECB is responsible for the effective and coherent operation of the SSM. It supervises the operation of the system through a distribution of competences between the ECB and the NCAs, as established under the SSM Regulation. To collateral effective supervision, credit institutions are classified as "significant" or "less significant". The former are supervised directly by the ECB, while the NCAs are responsible for the supervision of the latter.

The SSM is responsible for the prudential supervision of all the credit institutions in the participating Member States. The three main objectives of the SSM are to:

- collateral the security and solidity of the European banking system;

- strengthen financial integration and stability;

- achieve a uniform supervision.

The ECB directly supervises all the entities classified as significant (some 120 groups), with the assistance of the NCAs. They include BBVA Group. Day-to-day supervision is carried out by the joint supervisory teams (JSTs) made up of NCA and ECB staff.

The NCAs will continue to supervise directly the less significant banks, numbering around 3,500, under the supervision of the ECB.

EBA Revision of Pillar III

In January 2015 the EBA published its "guidelines on materiality, proprietary and confidentiality and on disclosure frequency." These technical guidelines define the processes and criteria that institutions must follow to identify material, confidential or proprietary information under Pillar III. In addition, the guidelines aim to specify what institutions must report prudential information with a frequency of less than a year, as well as the details of the information to be reported by them. None of these recommendations are in force at the date of this report.

Details of all the regulatory changes (IFRS) included within the framework of consolidation for accounting purposes are included in Note 2.3 of the Group's Annual Financial Statements.

Legal changes at international level

In 2013 the debate on the need for structural reforms in the system became increasingly significant. This debate has adopted different approaches in the different geographical regions.

In the United States, the Volcker Rule came into effect, aimed at restricting proprietary trading activities by U.S. banking institutions, i.e. trading with derivatives or other financial instruments not financed by deposits, in order to obtain a profit. In 2014 BBVA made progress in the process of implementing the Volcker Rule.

On January 29 2014, the European Commission (EC) announced its proposal for structural reform, which would impose new restrictions on the structure of European banks. The proposal aims to collateral the harmonization of divergent national initiatives in Europe.

However, the EC goes beyond national legislation in many European countries and opts for a mixed solution that establishes:

- The prohibition of proprietary trading, similarly to the aforementioned Volcker Rule; and

- A mechanism to require the separation of commercial activities, following the model of the banking reform in the United Kingdom.

The proposal is twofold, as it imposes both the prohibition of proprietary trading operations and investments in hedge funds and the separation of commercial activities.

The EC's reform is stricter than most of the national initiatives in countries like France, Germany or the U.S., as it goes beyond the recommendations of the High-Level Expert Group set up by the EC itself, which recommends a separation of proprietary trading operations, but not the prohibition of commercial activities.

The scope of the banks subject to the reform is very wide. All European global systemically important Banks (G-SIB) and institutions that carry out significant commercial activities, i.e. around 29 European banks, will be subject to this new regulation.

Basel Revision of Pillar III

In addition to the recommendations made by the EBA, the Basel Committee is in the process of revising the Pillar III framework. This process is expected to be complete in December 2015. The main aim of the revision is to improve the comparability and consistency of information. The proposal is to make greater use of templates:

- Mandatory templates for quantitative information that are considered essential for the analysis of regulatory capital requirements. They must be filled out by all the banks as specified.

- Templates with a more flexible format for qualitative information, considered valuable for the market but not essential for evaluating capital requirements. They may be filled out by banks according to an established format or following their own formats.