Innovation and technology: the digital transformation

The digital transformation

BBVA has been aware for some years that transformation involves adapting banking services to people's real lives. Consumers today rate convenience very highly, i.e. being able to make informed and well-advised decisions through face-to-face, remote (by phone or email) or digital channels, depending on their needs. This is demonstrated by the major investment in innovation and technology that BBVA has been making over recent years, with an annual average of around €800m since 2011.

1) Increase in the digital customer base

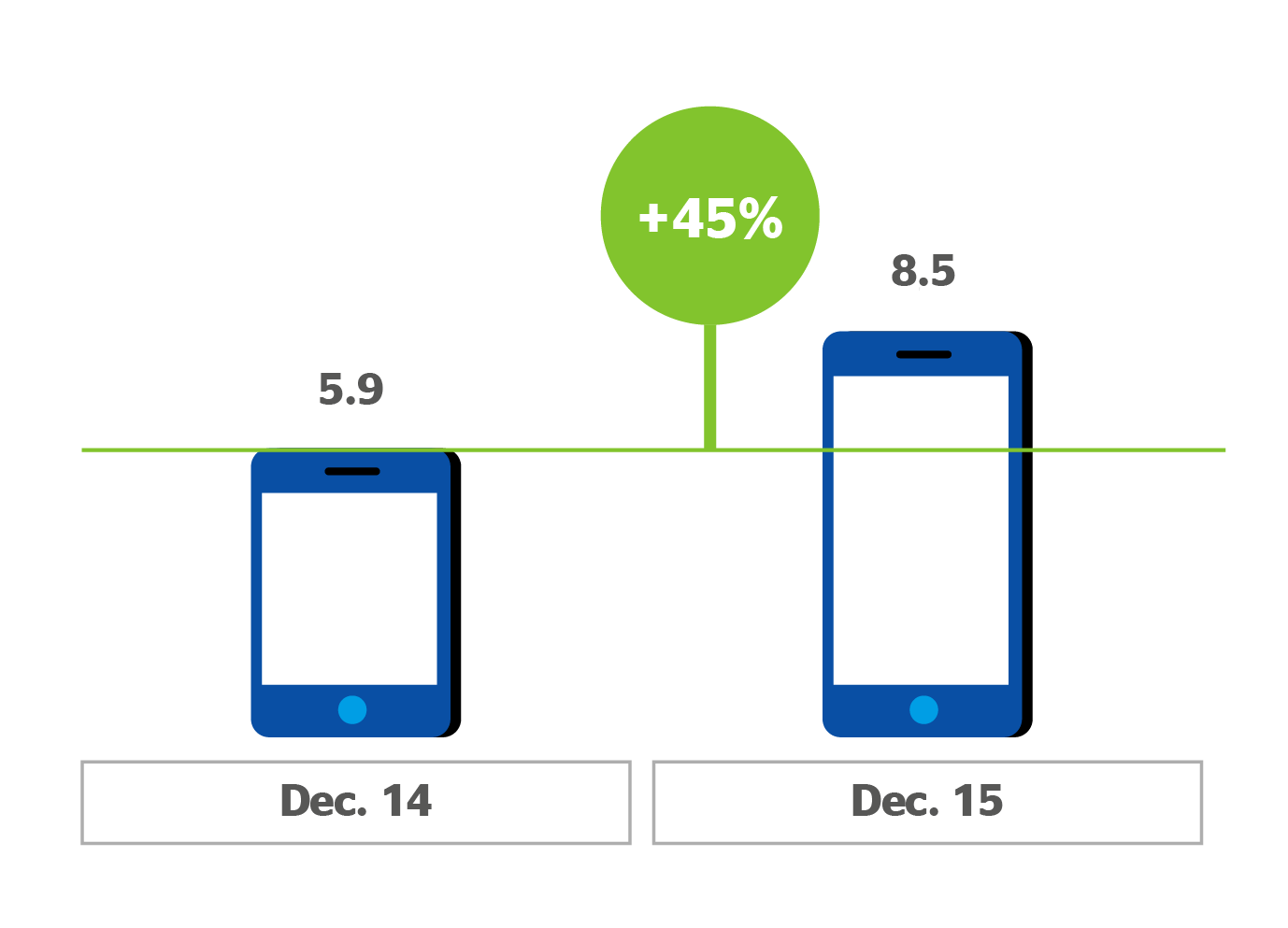

BBVA is continuing to expand the number of customers who interact with the Bank through digital channels. As of December 31, 2015, the Group had 14.8 million digital customers, that means a penetration of 33% and 19% up on last year, of whom 8.5 million are in mobile banking (up 45% on 2014).

BBVA Group. Digital customers (1)

(Million)

(1) Including Turkey.

In 2015 the digital customer base continued to increase

BBVA Group. Mobile customers (1)

(Million)

(1) Including Turkey.

They are customers who demand and carry out an increasing number of transactions.

BBVA Spain. Annual transactions

(Average transactions per customer)

More engaged

![]()

BBVA's app has had more than 4.2 million downloads and BBVA Wallet, the card management app, 2.3 million. The BBVA Contigo customized remote account management service has more than 600,000 customers Spain. In short, the functionalities developed through digital transformation make financial transactions more agile and simple, while also changing traditional banking concepts.

2) Transformation at the branch offices

BBVA's branch network has taken a leading role in the Bank's growth and transformation. It aims to adapt to the profile of customers by using a mix that combines face-to-face, remote or digital service in a 360º model. Beginning in November 2015, the managers of BBVA Contigo in Spain have been working integrated into the branch network teams. Branches also assist customers who have any queries so they can learn about the tools that will make their transactions easier.

In Mexico, the branch office rehabilitation and upgrading project, which has reached 1,400 branch offices in 2015, becomes a reality with the Bancomer Tower. The change in the comprehensive business model drives technological innovation with a view to improving customer experience.

Today, flexibility and convenience make mobile banking and the Internet the most highly rated channels among BBVA customers. But customers do not have to choose between self-service and the face-to-face channel: they can select face-to-face, remote or digital banking according to their needs at any given time. The new distribution model boosted by digital transformation means that activity in the branch, as measured by the number of transactions, continues to decline.

BBVA Spain. Branch activity

(Millions of transactions)

Flexibility and convenience make mobile banking and the Internet the most highly rated channels among BBVA customers

3) Progress in the development of new competencies

Within the Group's new organizational structure, approved in May 2015, are the New Core Competencies areas, which incorporate critical competencies to succeed in the new environment. Each of these areas has accomplished a number of milestones in 2015 to make progress in the development of these competencies.

Customer Solutions

In 2015, BBVA acquired the Californian design company Spring Studio, which specializes in user experience. The aim is to speed up the efforts to become the leading Bank in the digital environment through design and technology. This acquisition is another step by BBVA in the changing scenario of financial services, marked by new customer demands and the entry of digital competitors. BBVA believes that design is fundamental for the success of the business and has made this investment so that it can become one of its competitive features. As the number of customers that access their bank through cell phones, computers and tablets increases, the digital experience will be increasingly important in choosing one bank over others. Customer-centric design is key for innovation in the financial industry and BBVA is developing the best user experience across all its channels. Spring Studio has extensive experience in creating digital solutions for some of the most prestigious and innovative companies in the finance industry, e-commerce and technology. The company will now focus on BBVA's projects in the United States and South America.

Incorporating new design and user experience capabilities

Engineering

The Bank has created the Engineering area that not only manages technology operations but develops software and processes for customer solutions with a global approach. With the focus on digital transformation, in 2015 it structured its activity around the following lines of action:

- Developing the Group's technological architectures toward more standardized models, boosting the adoption of cloud computing (a paradigm that allows us to offer computing services through a network, usually the Internet).

- Transforming the Technology production function by incorporating elements of new technologies.

- Optimizing processes in search of improved customer experience, efficiency and operational control.

- Guaranteeing integrated management of security, as well as control of operations and information security.

- Facilitating the integration of Garanti and CX.

Leveraging the IT Platform to develop Open Platform and Big Data capabilities

a) Infrastructure

The increasing use of digital channels by customers has exponentially increased technological infrastructure processing needs. Increasing levels of customer digitization result in greater use of channels, which generates the need for an infrastructure with higher processing capacity.

Processing volume

Transactions a day in real time

Processing

capacity

in 2017:

+1,000 m

BBVA continues to make progress in its plan to build a network with four new next-generation data centers (two in Madrid and two in Mexico), which will operate in a crossed Business Recovery Services (BRS) model. In 2012, the first Data Processing Center (DPC) became operational in Madrid, and in 2015 the first entered into operation in Mexico (in Lake Esmeralda), with the highest security and reliability levels.

BBVA's DPC 1 in Madrid has obtained a Sustainable Building LEED® Gold certification, granted by the U.S. Green Building Council (USGBC), while the Madrid DPC 2 has obtained the Tier IV certification in construction from the Uptime Institute, as have rooms 1 and 2 of the Mexico DPC.

b) Architecture

Continuing the technological transformation process that BBVA began in 2007, optimization continues on core banking across the Bank's global footprint, and in the Corporate & Investment Banking business at the global level. The aim is to have modular technological platforms, available with a customer-centric vision. At the same time, progress has continued with migration and/or shutdown plans for old applications.

The data platforms have also continued to develop under the boost from the Informational Platform project, with particular emphasis on Spain and Mexico, incorporating into their capabilities new technologies for using Big Data. This development involves not only the incorporation of new technologies but also the shutdown of previous infrastructure and data operation applications.

Improvements have also been made in channels, particularly web (bbva.net) and mobile apps, which have incorporated new products and purchase functionalities such as one-click. There has also been an improvement in user experience with solid and innovative technological foundations, such as the use of the HTML5 language in the digital channel.

At the same time, a plan has been implemented for developing the architecture organized into two phases: The first involves boosting the adoption of cloud technologies. This will then give way to the following phase based on artificial intelligence (cognitive computing and automation). The aim of this plan is to have an architecture that allows the Group to reduce costs, promote the creation of reusable global components, increase processing capacity and reduce the time needed to integrate a new company into the Group.

c) Process transformation

There has also been progress on process transformation, providing many of them with a multi-channel capacity and aiming to increase the satisfaction level of customers and their loyalty. In 2015 a number of investments were made in projects including:

- Progress in implementing BBVA Wallet in Spain, Mexico, various parts of South America and Turkey (where it is called BonusFlas).

- The development and implementation of one-click strategies, which allow quick and easy product purchase.

- Complete renewal of banking websites in Chile and Uruguay and the implementation of the NetCash website for companies in Chile.

- The BBVA Provincial Onboarding project, which aims to improve customer experience, starting from the time the customer makes initial contact with the bank.

- Implementation of the Ekip platform for loans to retailers in Mexico and Chile.

- Development and implementation of the Digital Signature, both in Spain and Mexico and in countries in South America.

Global Marketing & Digital Sales

One of the strategic priorities of BBVA is to drive digital sales. This transformation of BBVA's relationship model with its customers brings its communication closer to them and offers new growth opportunities through both digital and remote sales. Thus, transformation has resulted in increased digital sales. In 2015, 19.2% of new consumer finance was granted through digital channels in Spain, 20.3% in South America and 29.6% in Mexico.

Exponential growing of digital sales and customer acquisition

Digital consumer loan sales

% of total consumers loans sold digitally

Spain

Mexico

South America

South America calculated as the average % of total consumer loans sold digitally in Argentine, Chile and Peru.

In turn, BBVA is investing in developing talent, capabilities, tools, methodologies and technologies to transfer best e-commerce practices and use these new tools and new models consistently and in a standard way across all the countries, and also in the development of the infrastructure to increase our ability to sell products through digital channels.

New Digital Businesses

Another strategic priority of BBVA is to create / associate with / acquire new business models. The new business models mean in practice that with the help of technology, new customer experiences can be introduced into the market that are not only better, but also cheaper. At BBVA we use different ways of building new business models or new businesses, adapted to each opportunity:

- In association with other companies, startups or even banks, with which we are working together on how we could use blockchain technology for quicker payment systems.

- By building our own applications, such as the online payment business Nimble, a virtual POS solution in Spain.

- Making investments, for which was created Propel Venture Partners (Propel). Its aim is to discover and help the most innovative financial services companies. Since its creation in 2012 it has invested in companies such as Personal Capital, Taulia, DocuSign, SumUp and the venture capital funds Ribbit Capital and 500 Startups. In 2015 it invested in Coinbase, the leading platform for transactions using the virtual bitcoin.

Fostering in-house innovation and accessing external innovation

- Building an ecosystem of developers, such as through the Open Talent competition for very interesting companies with which we can work to build new business models together.

BBVA has signed an agreement to enter into the capital of Atom in November 2015 with a stake of 29.5%. This is the first exclusively mobile bank in the United Kingdom and will begin operating in 2016. BBVA's investment will be used to contribute capital to develop the Atom project. BBVA will have the chance to participate in future rounds of finance and use its digital network to contribute knowledge and support to the development of Atom, whose aim is to offer a great user experience, using the best practices of the main digital companies and applying them to banking. Customers will be able to open an account through the Atom app, access their financial information easily and benefit from a great variety of unique tools to make the most out of their money. It is therefore a customer-centric bank, designed to meet customer needs and optimized for the mobile environment.

a) Open innovation model

BBVA continues to develop its open innovation model through BBVA Innovation Centers, which serve as open points of encounter for the innovation and entrepreneurial community. In 2015, another Innovation Center was opened in Mexico in the new Bancomer headquarters. Over the year, 187 events and activities were held, with more than 9,000 people taking part, to promote the entrepreneurial ecosystem, boost the development of innovative projects and make startups known from around the world. Of note was the event organized in Madrid with teachers from the Stanford d.school to teach the methodology of Design Thinking.

In the Living Lab (new open and collaborative innovation model) of the Innovation Centers we publicly share our vision of Digital Banking and some of the projects on which we have been working in this area to deal with changes in the financial sector. It is also a space for research with users, designed to improve our customers' digital experience by trying out ideas before they are launched commercially. The 3,000 people who visited the Living Lab in 2015 were mainly entrepreneurs, from business schools, the media and technological companies, as well as BBVA customers and employees.

The BBVA Innovation Center website and social networks, and the website for BBVAOpen4U.com developers, support and make known all the activities carried out, as well as generating and making available contents of the highest value to everyone.

Of particular note are the ebooks provided by Innovation Edge, a multi-platform publication that analyzes and presents new trends and progress in innovation. Each edition, published in English and Spanish, deals in depth with a subject related to the financial industry. They are available free to everyone. In 2015, a total of 26 books were published, which are also available for download on Amazon via Kindle.

BBVA's activities for entrepreneurs and open innovation include:

- The Innovachallenge Data Week for developers, a training conference that also presents the Innovachallenge MX project winners, with a program focused on creating applications using open-data APIs.

- The BBVABetatesters (more than 7,000 beta testers specializing in Fintech), who give us feedback on our new apps. It is a way of testing our ideas before they are finally launched. This community is growing constantly and so far more than 170 apps have been tested.

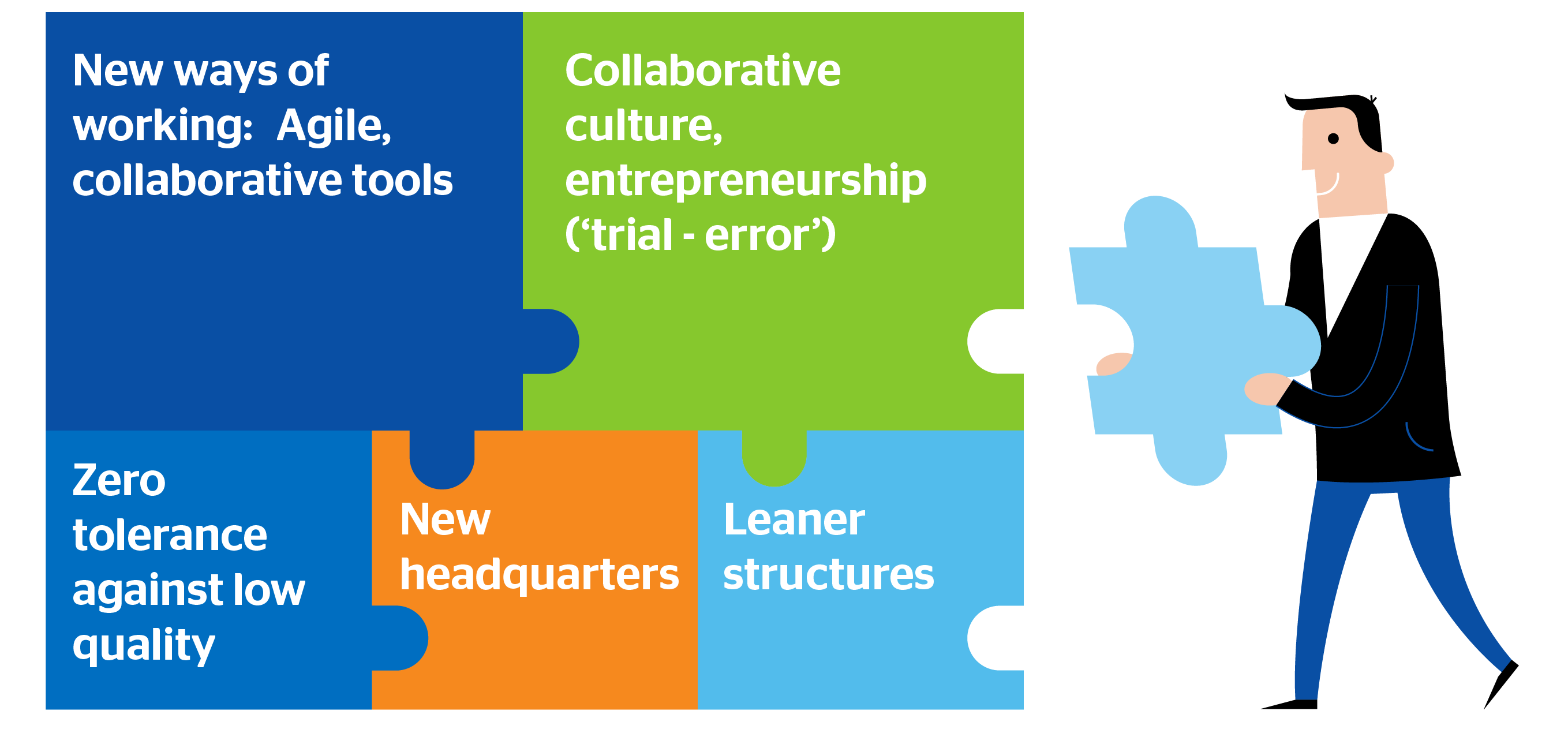

Talent & Culture

In 2015, the projects to build new corporate headquarters in Spain, Mexico and Chile were completed. The aim was to promote efficiency, corporate culture and digital transformation. To do so, new ways of working have been defined, requiring the implementation of technological equipment capable of meeting the new needs, and the creation of new spaces to foster collaboration, simplicity and improved user experience.

Cultural change

Transforming the organization internally by fostering a new culture