Global Risk Management

BBVA Group’s risk management function. General risk management and control model

BBVA Group's risk management function aims to preserve the Bank's solvency by supporting the definition of its strategy and ensuring sustainable business development. It is a single, independent and global function whose general principles are:

- The risks assumed must be compatible with the target solvency level and must be identified, measured and assessed. Monitoring and management procedures and sound control and mitigation systems must likewise be in place.

- All risks must be managed in an integrated way during their life cycle. They must be treated differently depending on their type and with active portfolio management based on a common variable: economic capital.

- The risk infrastructure must be adequate in terms of human resources, tools, databases, information systems and procedures, so that there is a clear definition of roles and responsibilities, to ensure efficient allocation of resources between the corporate area and the risk units in the geographical and/or business areas.

- It is each business area’s responsibility to propose and maintain its own risk profile both independently and within the corporate action framework, using a risk infrastructure appropriate to the established model.

The risk management function's aim: to preserve solvency and ensure sustainable business development

BBVA has a general risk management and control model (hereinafter “the model”) that is appropriate to its business model, its organization and the geographical areas in which it operates. This enables it to carry out its activity within the framework of the risk management and control strategy and policy defined by the Bank's corporate bodies and adapt itself to a changing economic and regulatory environment, addressing management both globally and adapted to the circumstances at any given time. This model is applied comprehensively throughout the Group and consists of the basic elements listed below:

- Governance and organization.

- Risk appetite.

- Decisions and processes.

- Evaluation, monitoring and reporting.

- Infrastructure.

BBVA promotes the development of a risk culture that ensures consistent application of the risk management and control model in the Group and guarantees that the risk management function is understood and internalized at all Organization levels.

BBVA has a risk management and control model in place that is applied comprehensively in the Group

BBVA Group. Risk function management framework

Goal: to preserve the Group's solvency, supporting its strategy and ensuring a sustainable business growth.

Governance and organization

Risk appetite

Decisions and processes

Assessment, monitoring and reporting

Infrastructure

Integrated management system structured around five pillars

A detailed explanation of each of the aforementioned basic elements of the model can be found in the Consolidated Annual Accounts, the Management Report and the Auditors' Report.

Credit risk

1) Introduction

The credit risk has its origin in the probability that one of the parties to a contract may breach its obligations for reasons of insolvency or inability to pay, causing a financial loss to the other party. It is the most important risk for the Group and includes counterparty risk, issuer risk, settlement risk and country risk management.

2) Credit risk quantification methodologies

The Bank quantifies its credit risk using two main metrics: expected loss (EL) and risk economic capital (REC). The expected loss reflects the average value of the estimated losses and is considered the cost of the business, while economic capital is the amount of capital needed to cover unexpected losses (i.e. if actual losses are higher than expected losses).

These risk metrics are combined with information on profitability in the value-based management framework, incorporating the profitability-risk binomial into the decision-making process, from the definition of business strategy to the approval of individual loans, price setting, assessment of non-performing portfolios, incentives to the different areas in the Group, etc.

The expected loss and the economic capital are the two main metrics to quantify the credit risk in BBVA

There are three risk parameters that are essential in the process of calculating the EL and REC metrics: the probability of default (PD), loss given default (LGD) and exposure at default (EAD). They are generally estimated using the available historical information and are assigned to transactions and customers according to their particular characteristics.

The expected loss and the economic capital are obtained, mainly, from three parameters: PD, LGD and EAD

Probability of default (PD)

PD is a measure of credit rating that is assigned internally to a customer or a contract with the aim of estimating the probability of non-compliance within a year. It is obtained through a process using scoring and rating tools.

The internal tools used for the calculation of PD are scoring and rating

a) Scoring

These tools are statistical instruments designed to estimate the probability of default according to the features of the contract-customer binomial. They are focused on management of retail credit: consumer finance, mortgages, credit cards of individuals, SME’s, etc.

An adequate management of the reactive, behavioral, proactive and bureau tools by the Group means that updated risk parameters can be obtained and are adapted to economic reality. This results in precise knowledge of the credit health of transactions and/or customers.

Scoring is used for the retail segment. There are different types of scoring: reactive, behavioral, proactive and bureau

b) Ratings

The risk assumed by BBVA in the wholesale customer portfolio is classified in a standardized way by using a single master scale in economic terms for the whole Group that is available in two versions: a reduced one with 22 degrees and an extended one with 34. The master scale allows discrimination amongst credit quality levels, taking into account geographical diversity and the different types of risk in the different wholesale portfolios in the countries where the Group operates.

The information provided by the rating tools is used when deciding on accepting transactions and reviewing limits.

Some of the wholesale portfolios managed by BBVA are low default portfolios, in which the number of default events is low (sovereign risks, corporations, etc.). To obtain PD estimates in these portfolios, the internal information is supplemented by external data, mainly from external rating agencies and the databases of external suppliers.

c) The economic cycle in PD

The latest financial crisis has revealed the importance of a proper anticipation in risk management. In this context, excess cyclicality of risk measurements has been identified as one of the causes of the instability of the metrics of financial institutions. BBVA has always been committed to estimating average cycle parameters that mitigate the effects of economic-financial turbulence in credit risk measurement.

Rating is used for the wholesale segment, in which default events are predicted at the customer level rather than at the contract level

The probability of default varies according to the cycle: it is greater during recessions and lower during expansions. In general, financial institutions do not have internal information on defaults covering a sufficiently long period of time to serve as an observation of the behavior of portfolios over a complete cycle. That is why adjustments have to be made to the internal data. The adjustment process to translate the default rates obse rved empirically into average default rates is known as cycle adjustment. The cycle adjustment uses sufficiently long economic series related to the default of portfolios, and their behavior is compared with that of the default events in the Entity’s portfolios. Any differences between past and future economic cycles may also be taken into account, thus resulting in a certain prospective approach.

Loss given default (LGD)

Loss given default (LGD) is another of the key metrics used in quantitative risk analysis. It is defined as the percentage exposure at risk that is not expected to be recovered in the event of default.

BBVA basically uses two approaches to estimate LGD. The most common one is known as "workout LGD", in which estimates are based on the historical information observed by the Entity, by discounting the flows observed throughout the recovery process of the contracts that have been in default at some point. In portfolios with a low rate of default (low default portfolio, or LDP), there is insufficient historical experience to make a robust estimate using the workout LGD method, so external sources of information have to be combined with internal data to obtain a representative rate of loss given default.

LGD estimates are carried out by segmenting operations according to different factors that are relevant for its calculation, such as the default period, seasoning, the loan-to-value ratio, type of customer, score, etc. The factors considered may be different according to the portfolio being analyzed.

In the BBVA Group, different LGDs are attributed to the outstanding portfolio (default and non-default), according to combinations of all the significant factors, depending on the features of each product and/or customer.

Lastly, it is important to note that LGD varies with the economic cycle. Hence, two concepts can be defined: long-run LGD (LRLGD) and LGD at the worst moment in the cycle, or downturn LGD (DLGD).

LRLGD represents the average long-term LGD corresponding to an acyclical scenario that is independent of the time of estimation. DLGD represents the LGD at the worst time of the economic cycle, so it should be used to calculate economic capital, because the aim of EC is to cover possible losses incurred over and above those expected.

Loss given default (LGD) is a key metric in quantitative risk analysis. It also has other internal management purposes. For example, for proper price discrimination

Every estimate of loss given default (LGD, LRLGD and DLGD) is performed for each portfolio, taking into account all the aforementioned factors. However, no LRLGD or DLGD estimates are made in portfolios in which the loss given default is not significantly sensitive to the cycle, as they are recovery processes that cover extended periods of time in which the isolated situations of the economic cycle are mitigated.

In addition to being a basic input for quantifying losses (both expected and capital losses), LGD estimates have other internal management purposes. For example, LGD is an essential factor to discriminate prices, in the same way that it can determine the approximate value of a defaulted portfolio in the hypothetical event of outsourcing recoveries or defining which potential recovery actions have the highest priority.

Exposure at default (EAD)

Exposure at default (EAD) is another of the inputs required to calculate expected loss and capital. It is defined as the outstanding debt at the time of default.

The exposure of a contract tends to be the same as its balance, although for products with explicit limits, such as cards or credit lines, exposure should include the potential increase in the outstanding balance from a reference date to the time of default. The EAD is therefore obtained by adding the risk already drawn on the transaction to a percentage of undrawn risk. This percentage of the undrawn balance that is expected to be used before default occurs is known as the credit conversion factor (CCF). Thus, the EAD is estimated simply by calculating this conversion factor. In addition, the relevance of adding to EAD the possibility of using an additional percentage of the limit for transactions that exceed it on a reference date is assessed, according to the risk policy for each product.

The estimate of these conversion factors also includes distinguishing factors that depend on the characteristics of the transaction.

In order to obtain CCF estimates for low-default portfolios, the LDPs, external studies and internal data are combined, or behavior similar to other portfolios is assumed and their CCFs are assigned in this way.

a) The portfolio model and concentration and diversification effects

Credit risk for the global portfolio of the BBVA Group is measured through a portfolio model where the effects of concentration and diversification are considered. Its purpose is to study the entire loan book as a whole, by analyzing and capturing the effect of interrelations between the various portfolios.

In addition to enabling a more comprehensive calculation of capital needs, this model is a key tool for credit risk management, as it establishes loan limits based on the contribution of each unit to total risk in a global, diversified setting.

The EAD adds the risk already drawn to a percentage (CCF) of undrawn risk

The portfolio model considers that risk comes from various sources (it is a multi-factor model). This feature implies that economic capital is increasingly sensitive to geographic diversification, a crucial aspect in a global entity like BBVA.

The tool is also sensitive to the concentration that may exist in certain credit exposures, such as the Institution’s large customers. Apart from geography, industry factors are now key to business concentration analyses.

3) Credit risk in 2015

At the close of 2015, the main variables related to the Group's credit risk management have been positive. The year-on-year increase in credit risk and non-performing loans, as well as the performance of the main risk indicators, have been affected, mainly, by the incorporation of CX and the the effects resulting from the purchase of an additional 14.89% stake in Garanti. On a comparable basis, i.e. excluding CX and taking Turkey on a like-for-like comparison (25.01% stake in Garanti and integration in the proportion corresponding to this percentage), the general tone remains positive.

- The Group's credit risk increased by 19.5% since December 2014.

Favorable and outstanding trend in the main risk indicators

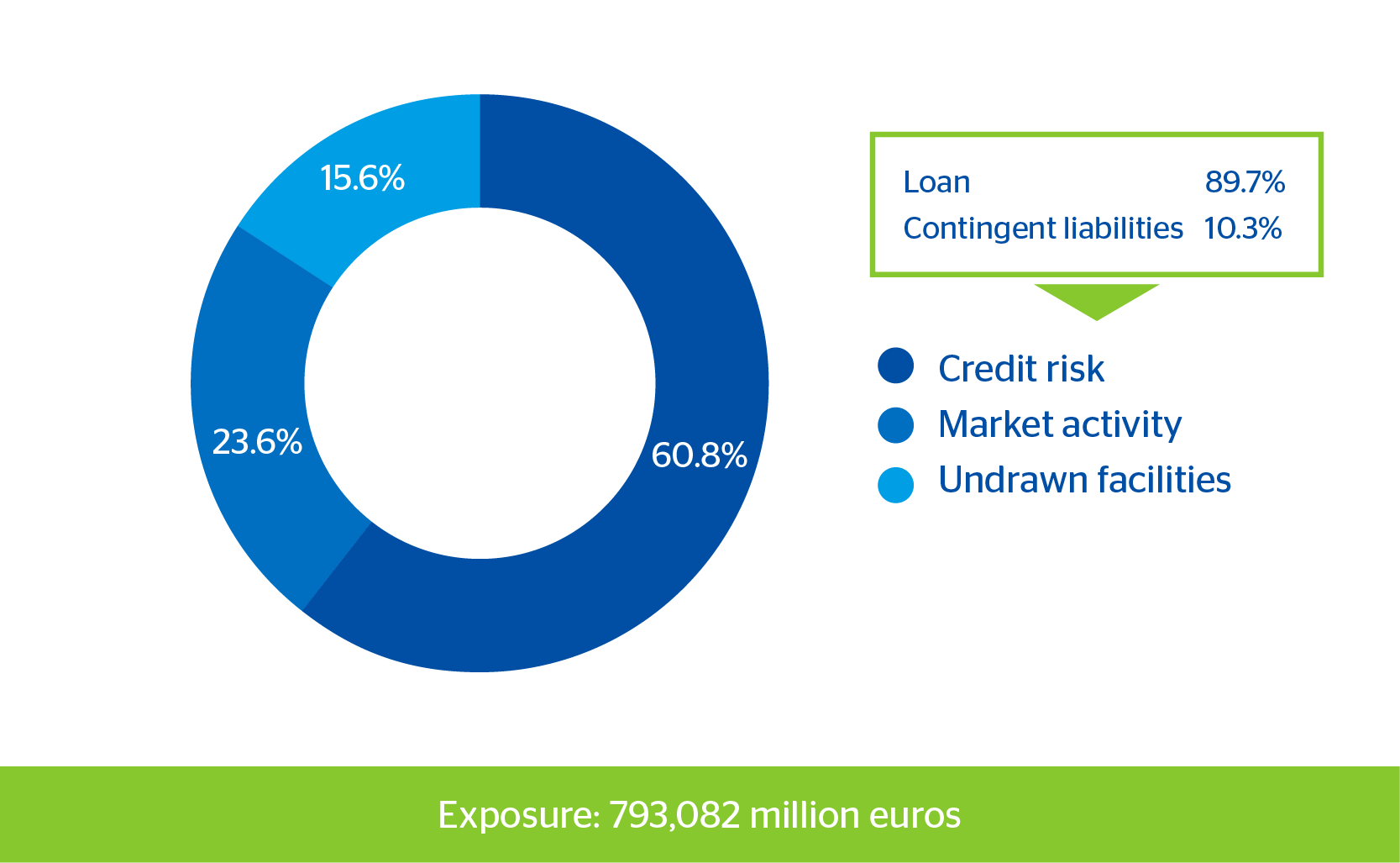

BBVA Group. Exposure to credit risk. Breakdown by types of risk (31-12-2015)

BBVA Group. Exposure to credit risk (gross). Breakdown by business areas (31-12-2015)

| Banking activity in Spain | 43.2% |

| Turkey | 15.1% |

| Real-estate activity in Spain | 2.6% |

| United States | 13.3% |

| Rest of Eurasia | 4.8% |

| Mexico | 10.3% |

| South America | 10.6% |

Risk: 482,518 million euros

BBVA Group. Exposure to loans and advances to customers (gross). (31-12-2015)

| Individuals | 47.6% |

| Corporates and businesses | 32.9% |

| Institutions | 6.9% |

| Global customers | 12.6% |

- The balance of non-performing loans amounts to €25,996m; €3,494m come from CX. Additionally, excluding the Garanti effect, there has been a year-on year decline of 11.1% in non-performing loans, with declines across all the geographical areas, although there was a notable reduction in Spain in banking activity and real-estate activity.

BBVA Group. Variation in non-performing assets

(Million euros)

| 2015 | 2014 | 2013 | |

| Beginning balance | 23,590 | 26,243 | 20,603 |

| Entries | 9,473 | 9,074 | 18,027 |

| Recoveries | (6,959) | (7,265) | (7,840) |

| Net variation | 2,514 | 1,809 | 10,187 |

| Write-offs | (5,003) | (4,754) | (3,856) |

| Exchange rate differences and other | 4,895 | 291 | (691) |

| Period-end balance | 25,996 | 23,590 | 26,243 |

BBVA Group. Evolution in non-performing loans by business areas

(Million euros)

| Banking activity in Spain | Real-estate activity in Spain | The United States | Turkey | Mexico | South America | Rest of Eurasia | ||||||||

| 2015 | 2014 | 2015 | 2014 | 2015 | 2014 | 2015 | 2014 | 2015 | 2014 | 2015 | 2014 | 2015 | 2014 | |

| Beginning balance | 11,385 | 12,480 | 7,770 | 9,259 | 459 | 513 | 474 | 390 | 1,385 | 1,469 | 1,220 | 1,108 | 872 | 957 |

| Entries | 621 | 514 | (491) | (661) | 226 | 32 | 249 | 107 | 1,549 | 1,418 | 548 | 591 | (184) | 33 |

| Write-offs | (1,856) | (1,546) | (1,143) | (975) | (152) | (139) | (38) | (33) | (1,503) | (1,549) | (365) | (407) | (58) | (70) |

| Exchange rate differences and other | 3,695 | (63) | 342 | 148 | 51 | 54 | 1,365 | 10 | (148) | 47 | (228) | (72) | (43) | (49) |

| Period-end balance | 13,844 | 11,385 | 6,478 | 7,770 | 584 | 459 | 2,050 | 474 | 1,283 | 1,385 | 1,175 | 1,220 | 587 | 872 |

BBVA Group. Gross additions to NPL

(Million euros)

Total gross additions

2014: 9,074

Total net additions

2014: 1,809

2015: 9,473

2015: 2,514

BBVA Group. NPL recoveries

(Percentage)

- As a result, the NPL ratio closes the year at 5.4% (5.8% in Dec-2014) and the coverage ratio at 74% (64% a year before).

- Loan-loss provisions have increased by 28.0% since the close of 2014.

BBVA Group. NPL and coverage ratios

(Percentage)

| December 2013 | December 2014 | December 2015 | |

| Tasa de cobertura | 60 | 64 | 74 |

| Tasa de mora | 6.8 | 5.8 | 5.4 |

- Lastly, there has been an improvement in the cost of risk compared with the cumulative figure of December 2014.

BBVA Group. Cost of risk by business areas

Percentage

| Total Group | Spain | The United States | Turkey | Mexico | South America | Rest of Eurasia | |

| 2014 | 1.25 | 1.03 | 0.16 | 1.16 | 3.45 | 1.46 | 0.31 |

| 2015 | 1.06 | 0.75 | 0.25 | 1.24 | 3.28 | 1.26 | 0.02 |

Note: Spain includes real-estate activity.

Expected losses

Expected losses not attributed in the performing portfolio, adjusted to the economic cycle average, stood at €3,746m as of the close of December 2015, a year-on-year decrease of 2.3% using comparable data. In attributable terms, and not including the non-performing portfolio, as of December 2015 this heading totals €3,092m, 0.1% higher than the previous year, using comparable data.

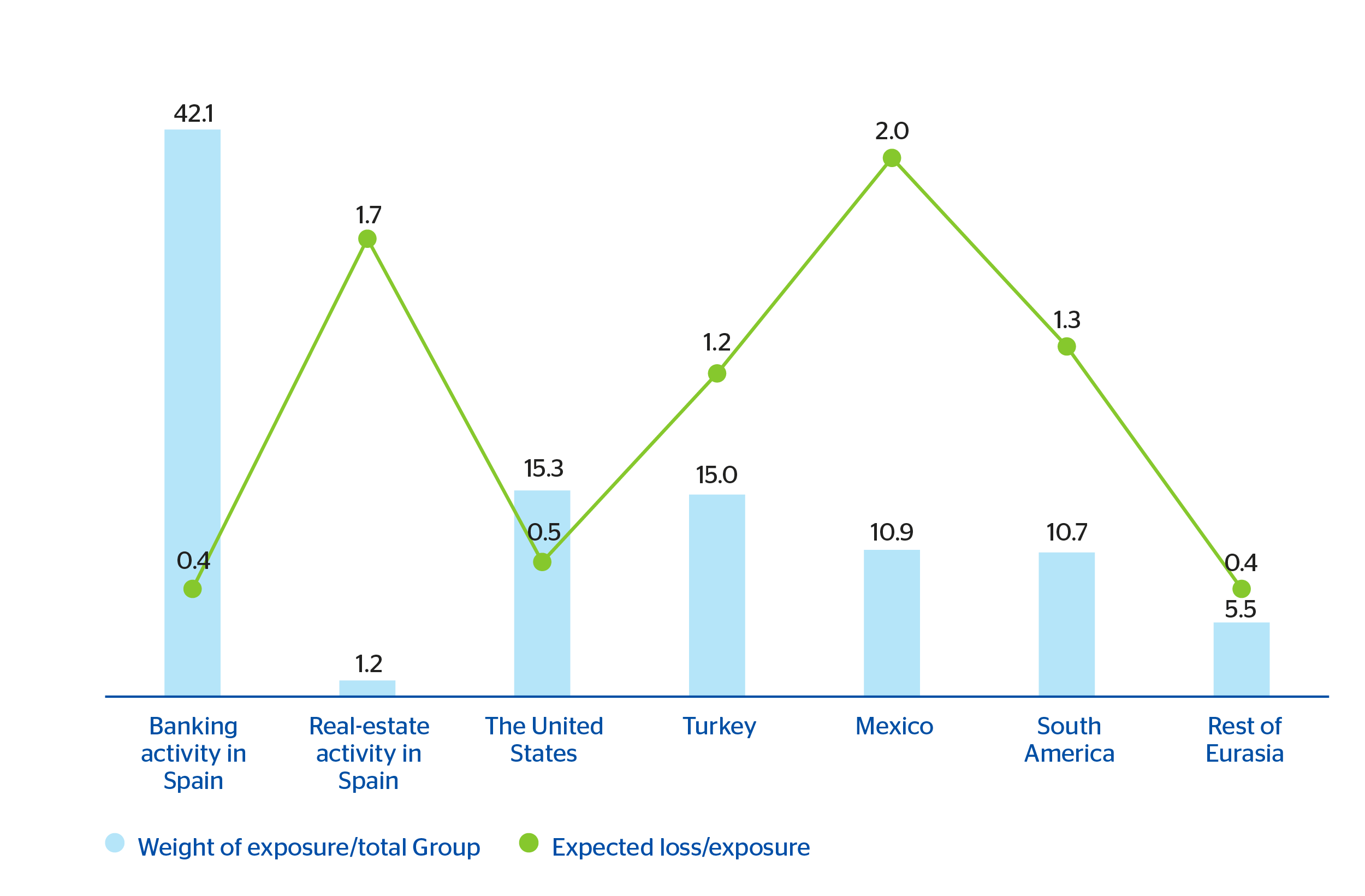

The chart below shows expected losses by business areas as of the close of December 2015.

BBVA Group. Consolidated expected losses (balances not in default) by business areas

(Percentage over exposure. Figures as of 31-Dec-2015)

The expected losses of the Group's main portfolios at the close of December 2015 are also shown below.

BBVA Group. Consolidated expected losses (balances not in default) by portfolio

(Percentage over exposure. Figures as of 31-Dec-2015)

A detailed explanation of the aforementioned risk can be found in the Consolidated Annual Accounts, the Management Report and the Auditors' Report and in the Pillar III Report.

Market risk

Market risk in trading book

Introduction

This type of risk originates as a result of movements in the market variables that impact the valuation of traded financial products and assets.

The main risks generated can be classified as follows:

- Interest-rate risk: This arises as a result of exposure to the movement of the different interest-rate curves involved in trading. Although the typical products that generate sensitivity to these movements are those in the money market (deposits, interest-rate futures, call money swaps, etc.) and traditional interest-rate derivatives (swaps and interest-rate options such as caps, floors, swaptions, etc.), practically all the financial products have exposure to interest-rate movements due to the effect that such movements have on their valuation through the financial discount.

- Equity risk: This arises as a result of movements in share prices. This risk is generated in spot positions in shares, as well as any derivative products whose underlying asset is a share or an equity index. Dividend risk is a sub-risk of equity risk, as being an input for any equity option, its variation may affect the valuation of positions and it is a factor that generates risk on the books.

- Exchange-rate risk: This is caused by movements in the exchange rates of the different currencies in which a position is held. As in the case of equity, this risk is generated in cash currency positions, and in any derivative product whose underlying is an exchange rate. In addition, the quanto effect (operations in which the underlying asset and the nominal are denominated in different currencies) means that certain transactions in which the underlying asset is not a currency generating an exchange-rate risk that has to be measured and monitored.

- Credit spread risk. Credit spread is an indicator of an issuer's asset quality. This risk occurs due to variations in the levels of asset quality of both corporate and government issues, and affects both the positions in bonds and credit derivatives.

- Volatility risk: This occurs as a result of changes in the levels of implied price volatility of the different market instruments on which derivatives are traded. This risk, unlike the others, is exclusively a component of trading in derivatives.

The metrics developed to control and monitor market risk in BBVA Group are aligned with best practices in the market and are implemented consistently across all the local market risk units.

Market risk may be of various kinds: interest-rate, equity, exchange-rate, credit spread and volatility risk

Measurement procedures are established in terms of the possible impact of negative market conditions on the trading portfolio of the Group's Global Markets units, both under ordinary circumstances and in situations of heightened risk.

The standard metric used to measure market risk is Value at Risk (VaR), which indicates the maximum loss that may occur in the portfolios at a given confidence level (99%) and time horizon (one day). This statistical value is widely used in the market and has the advantage of summing up in a single metric the risks inherent to trading activity, taking into account how they are related and providing a prediction of the loss that the trading book could sustain as a result of fluctuations in equity prices, interest rates, foreign exchange rates and commodity prices.

The analysis of market risk takes into consideration the following risks: credit spread, basis risk between several instruments, volatility risk or correlation risk.

Management structure

The current management structure includes the monitoring of:

- Market risk limits, consisting of a scheme of limits based on VaR, economic capital (calculated based on VaR measurements) and VaR sub-limits.

- Stop-loss orders (i.e. orders to cease or limit losses) for each of the Group's business areas.

The global limits are approved annually by the Executive Committee (EC) at the proposal of the market risk unit, following presentation to the GRMC and in the Risk Committee (RC). This limits structure is developed by identifying specific risks by type, trading activity and trading desk. The market risk unit maintains consistency between the limits. This control structure is supplemented by limits on loss and a system of alert signals to anticipate the effects of adverse situations in terms of risk and/or result.

Market risk in 2015

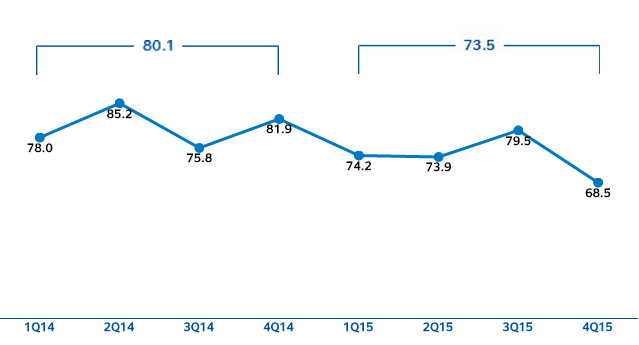

The Group’s market risk remains at low levels compared with the aggregates of risks managed by BBVA, particularly in terms of credit risk. This is due to the nature of the business and the Group’s policy of minimal proprietary trading. In 2015, the average VaR was €25 million, slightly higher than in 2014, with a maximum level for the year on March 4 of €30 million. The changes in BBVA Group’s market risk in 2015, measured as VaR (without smoothing), with a 99% confidence level and a 1-day horizon, are shown below, expressed in million euros.

Market risk in BBVA remains relatively low

BBVA Group. Market risk evolution in 2015

(VaR in euros)

By type, the main risk factor in the Group continues to be linked to interest rates, with a weight of 48% of the total at the end of 2015 (this figure includes spread risk); which implies that it has reduced its relative weight compared with the close of 2014 (67%). Foreign exchange risk accounts for 21% and has increased its proportion compared with the same date last year (12%), while equity risk and volatility and correlation risk have increased, with a weight of 32% at the close of 2015 (versus 20% at the close of 2014).

BBVA Group. Market risk by risk factors in 2015

(Million euros)

| VaR by risk factors | Interest/spread risk | Interest-rate risk | Equity risk | Vega / Correlation risk | Diversification effect(1) | Total |

| 2015 | ||||||

| Average VaR | 24 | |||||

| Maxium VaR | 32 | 5 | 3 | 9 | (18) | 30 |

| Minimum VaR | 20 | 6 | 3 | 9 | (17) | 21 |

| End-of-period VaR | 21 | 9 | 3 | 11 | (20) | 24 |

(1) The diversification effect is the difference between the aggregation of each risk factor, individually measured, and the total VaR figure which refflects the implicit correlation among all the variables and scenarios used in the measurement.

By geographical areas, 44.3% of the market risk corresponds to the trading floors of the Global Markets units in Europe, New York, Asia and BBVA Compass, and 55.7% to the Group’s banks in Latin America, of which 40.4% is in Mexico.

The change in average daily VaR over 2015 compared with 2014 is basically due to Global Markets Mexico and Global Markets Europe, New York and Asia, which have increased their average risk by 14 % and 5%, respectively. This increase is partially offset by the reduction in the Global Markets units in South America (14%).

BBVA Group. Market risk by geographical area

Average 2015. Percentage

A detailed explanation of this risk can be found in the Consolidated Financial Statements, the Management and Auditors’ Reports and in the Pillar III Report, specifically of the quantification methodology and the validation of the internal market risk model.

Credit risk in trading book

The credit risk assessment in OTC financial instruments is made by means of a Monte Carlo simulation, which calculates the current exposure of the counterparties and their possible future exposure to fluctuations in market variables.

The model combines different credit risk factors to produce distributions of future credit losses and thus allows a calculation of the portfolio effect; in other words, it incorporates the term effect (the exposure of the various transactions presents potential maximum values at different points in time) and the correlation effect (the relationship between exposures, risk factors, etc. is normally different from 1). It also uses credit risk mitigation techniques such as legal netting and collateral agreements.

Credit risk in trading book also decreases in 2015

The maximum credit risk exposure in derivatives with counterparties in the Group as of 31-Dec-2015 stood at €49,350 million, an increase of 4% on 2014 year-end. Excluding contractual arrangements of netting and collateral, the net exposure in derivatives stands at €16,705 million as of 31-Dec-2015, which means a 7% reduction against the same figure of last year.

Maximum exposure to credit risk in derivatives at BBVA, S.A. is estimated at €35,535 million (compared with €39,185 in the previous year). BBVA S.A.’s overall reduction in terms of exposure due to netting and collateral agreements is €24,306 million.

Therefore, the net risk in derivatives at BBVA, S.A. as of December 31, 2015 is €11,229 million (compared with €11,203 million the previous year).

The table below shows the distribution by sectors and by products of the amounts of the maximum credit risk exposure in financial instruments in BBVA, S.A. Exposure continues to be mainly concentrated in financial institutions (44%) and in corporates (52%).

Net counterparty risk by type of product and sector. Maximum exposure at BBVA, S.A. (excluding intra-group counterparties)

(Million euros)

| Units | Derivates | Deposits | Repos | Other | Total |

| Financial sector | 4,834 | 0 | 202 | (36) | 5,000 |

| Corporate | 3,859 | - | - | 0 | 3,859 |

| Branches | 2,152 | 0 | - | 0 | 2,152 |

| Sovereign | 384 | 58 | 0 | 0 | 442 |

| TOTAL | 11,229 | 58 | 202 | (36) | 11,453 |

And the following table shows the distribution by maturities of the maximum exposure amounts in financial instruments. Maturity index is 3.8 years.

Maturity vector by rating and tranches at BBVA, S.A. (excluding intra-group counterparties)

(Millon euros as of 31-12-2015)

| Up to 3 months | Up to 12 months | Up to 3 years | Up to 5 years | Up to 10 years | More than 10 years | |

| AAA | - | - | - | - | 46 | 76 |

| AA | 509 | 105 | 101 | 112 | 112 | 155 |

| A | 290 | 858 | 715 | 357 | 708 | 528 |

| BBB | 138 | 165 | 489 | 369 | 857 | 634 |

| Non investment grade | - | 388 | 520 | 457 | 667 | 244 |

| NR | - | - | - | 5 | 17 | 5 |

| D | - | 12 | 14 | 8 | 13 | 7 |

| TOTAL | 938 | 1,528 | 1,839 | 1,308 | 2,419 | 1,647 |

The counterparty risk assumed in this activity involves entities with a high credit rating (A- or higher in 48% of cases).

Distribution of maximum exposure by ratings at BBVA, S.A (Excluding intra-group counterparties)

By geographical areas, the maximum exposure of BBVA, S.A. is in counterparties in Europe (84%) and the United States (9%), which together account for 92% of the total.

Geographical distribution of maximum exposure at BBVA, S.A (Excluding intra-group counterparties)

(Percentage)

Structural risks

Introduction

Structural risks (SR) in BBVA include the risks managed on the Group's balance sheet that arise from the Bank's structural exposure to various market risk factors and conditions in the financial environment. This generic classification includes the risks related to asset and liability management and, in addition, the structural exchange-rate risk and structural equity risk, i.e.:

- Structural interest-rate risk, whose management aims to maintain BBVA Group's exposure to market interest-rate fluctuations at levels consistent with its strategy and risk profile. This risk follows the Group's decentralized management model. The Balance Sheet Management unit, through the Assets and Liabilities Committee (ALCO), designs and executes the defined strategies, respecting the tolerances established within the risk appetite framework.

BBVA's structural risks in 2015 have decreased in relation to previous years in terms of economic capital

- Structural exchange-rate risk is inherent in the activity of international banking groups which, like BBVA, carry out their business in different geographical areas and in different currencies. At Group level, this risk arises basically through exposure to changes in exchange rates in BBVA Group's companies abroad that consolidate on the Group's balance sheet and whose functional currency is not the euro. Managing this risk is based on a simulation model of scenarios to quantify the changes in value that can occur with a given confidence level and a predetermined time horizon. The balance sheet management unit, through the Assets and Liabilities Committee (ALCO), designs and executes the strategies to carry out, being supported by the internal risk metrics according to the corporate model. It also carries out hedging operations with the goal of minimizing the impact on capital of changes in exchange rates, according to their projected trend.

- Structural equity risk, which originates from the possible negative impact derived from the loss of value of investments in industrial and financial companies with medium and long-term investment horizons. The corporate GRM area is responsible for the measurement and effective monitoring of structural equity risk by estimating the sensitivity and the capital necessary to cover possible unexpected losses due to variations in the value of the companies comprising the Group’s investment portfolio, at a confidence level that corresponds to the Institution’s target rating, and taking into account the liquidity positions and the statistical behavior of the assets under consideration.

The main aspects of structural risk management in BBVA Group in terms of purpose, governance and management are described below.

| Structural risk management | Structural interest-rate risk | Structural exchange-rate risk | Structural equity risk |

|---|---|---|---|

| Purpose | To preserve net interest income, contributing to the generation of recurrent earnings, and optimize the Bank's economic value in the face of variations in market interest rates. | To minimize potential negative impacts of fluctuations in exchange rates on the Group's equity, solvency and earnings in relation to its strategic international investments. | To optimize the planned profitability according to the assigned tolerance, in each structural portfolio with positions in non-strategic industrial and financial companies, with medium and long-term investment horizons. |

| Governance | The Executive Committee approves the system of limits and alerts, following review by the Global Risk Management Committee and the Risk Committee. This approval transposes the tolerances approved by the Board of Directors into the management metrics of each risk. | ||

| GRM prepares the proposal for the system of limits and alerts as well as performing structural risks’ control and monitoring. Their functions include: Designing the measurement models and systems, developing the policies on corporate management, information and control, and preparing the risk measurements that underpin the Group's management | |||

| GRM regularly reports the management metrics to both the management and administration bodies: ALCO, Risk Committee and the Executive Committee. | |||

| Responsible for management | ALCO is the body that evaluates the implementation of the actions according to the proposals of the Balance Sheet management unit belonging to the Finance area. It designs and executes the strategies to be implemented, in accordance with the tolerances set out in the risk appetite framework. | Finance units implement strategies, managing their exposure in accordance with the limits set for the management metrics. | |

| Control and management variables | Deviations from the budgeted net interest income (going concern dynamic model) and deviations from economic value (economic capital). | Solvency ratio, earnings and equity (economic capital). | Economic capital, exposure and earnings. |

| Management Model | Decentralized and independent in each balance sheet management unit/liquidity management unit associated with the different geographical areas. | Consolidated for BBVA Group. | At management portfolio level of holding companies. |

The elements shown in the above table are regulated in the relevant corporate management policies approved by the Executive Committee for each risk. Moreover, procedures are in place based on and developing these policies, guaranteeing that the processes in all management aspects are consistent with the established principles. With the implementation of a decentralized model for structural interest-rate risks, each of the balance sheet management units (BSMUs) are managed on an individual basis, in accordance with the corporate policy, and with specific control mechanisms.

The contribution of structural risks to the Group's map of capital at risk has decreased compared with the previous year. It is worth noting that the risk arising from equity exposures lost weight in 2015, while the weight of structural interest-rate risk has increased.

Structural interest-rate risk

Structural interest-rate risk (SIRR) is related to the potential impact that variations in market interest rates have on an entity's net interest income and equity. In order to properly measure SIRR, BBVA takes into account the main sources that generate this risk: repricing risk, yield curve risk, option risk and basis risk, which are analyzed from two complementary points of view: net interest income (short term) and economic value (long term). The accompanying chart shows the gaps in BBVA's structural balance sheet in euros, i.e. the risk that arises from different maturities or repricing of the assets and liabilities in the banking book.

Maturity and repricing gaps of BBVA’s structural balance sheet in euros

(Millon euros)

| 1-3 M. | 3-6 M. | 6-9 M. | 9-12 M. | 2 years | +3 years | |

| Earnings | 25,155 | 23,539 | -2,564 | -3,241 | -1,737 | -55,953 |

The chart below shows the profile of sensitivities to net interest income and value of the main entities in BBVA Group.

Appropriate balance sheet management has kept BBVA's exposure to interest-rate fluctuations at moderate levels, consistent with the Group's target risk profile

BBVA Group. Structural interest-rate risk profile

NIIS: Net interest income sensitivity (in percentage) of the franchise to +100 basis points.

EVS: Economic value sensitivity (in percentage) of the franchise to +100 basis points.

Size: Core capital to each franchise.

In 2015, accommodative monetary policies have remained in place with the aim of boosting demand and investment, with interest rates in Europe and in the United States remaining at all-time lows. In Latin America, the slowdown in growth and the upward pressure on inflation in most countries have prompted many central banks (including those in Chile, Peru and Colombia) to hike interest rates, despite the environment of economic slowdown.

BBVA Group's positioning has a positive sensitivity in its net interest income to interest rate hikes, while in terms of economic value the sensitivity is negative to interest rate increases, except for the euro balance sheet. Mature markets, both Europe and the United States, show greater sensitivity in terms of their projected net interest income against a parallel shock of interest rates. However, in 2015 this negative sensitivity to cuts has been confined by the limited downward trend in interest rates. In this interest-rate environment, appropriate management of the balance sheet has maintained BBVA's exposure at moderate levels, in accordance with the Group's target risk profile.

Structural exchange-rate risk

In BBVA Group, structural exchange-rate risk arises from the consolidation of holdings in subsidiaries with functional currencies other than the euro. Its management is centralized in order to optimize the joint handling of permanent foreign currency exposures, taking into account the diversification.

In 2015, the most notable aspect in the foreign-exchange markets has been the strength of the United States dollar and the weakness of the currencies of emerging economies, which have depreciated noticeably against the dollar, affected by the slump in commodity prices, particularly of oil, and the uncertainty surrounding the growth of those economies following the change in the Fed's monetary policies and the slowdown in China. This has led to an upturn in volatility in the foreign-exchange markets. Also worth mentioning is the more unfavorable performance of the Argentinean peso and the Venezuelan bolivar fuerte, affected by the imbalances in both economies. In this context, the Group's structural exchange-rate risk has been moderate in 2015 due to the sale of the stakes in the Citic Group and the increase in hedging, focused on the main exposures. Thus, the risk mitigation level of the book value of BBVA Group's holdings in foreign currency has remained on average at 70% at the end of the year and coverage of earnings in foreign currencies in 2015 has reached 46%.

CET1 ratio sensitivity to a 1% appreciation of the euro exchange rate with respect to other currencies

(Basis points)

Structural exchange-rate risk in BBVA has been moderate in 2015 due to the sale of the stakes in the Citic Group and the increase in hedging, focused on the main currencies that have an impact on the Group's financial statements

Structural equity risk

In 2015, the good performance of the European stock exchanges in the first half of the year has slowed down sharply in recent months, affected by the slump in oil prices and the uncertainty surrounding global growth. This shifting trend has resulted in a worsening of the capital gains accumulated in the Group's investments in equity.

Structural equity risk, measured in terms of economic capital, has decreased significantly, due mainly to the sale of the stakes in Citic Group.

A detailed explanation of each of the aforementioned risks can be found in the Consolidated Financial Statements, the Management Report and the Auditors’ Report and in the Pillar III Report.

BBVA's structural equity risk has decreased noticeably, due mainly to the sale of the stakes in Citic Group

Liquidity and funding risk

The main aspects of the management of liquidity and funding risks in BBVA Group in terms of purpose, governance and management are described below.

| Management | Liquidity risk | Funding risk |

|---|---|---|

| Purpose | In the short term, to meet the payment commitments on time and in an appropriate manner, without having to resort to funding under burdensome terms or under conditions that may damage the Institution's reputation. | In the medium and long term, to ensure that the Group’s funding structure is appropriate and that its evolution is suitable regarding the economic situation, the markets and the regulatory changes, in accordance with the established risk appetite. |

| Governance | The Executive Committee approves the system of limits and alerts, following review by the Global Risk Management Committee and the Risk Committee. This approval transposes the tolerances approved by the Board of Directors into the management metrics of each risk. | |

| GRM prepares the proposal for the system of limits and alerts and performs structural risks control and monitoring. Its functions include designing the measurement models and systems, developing the policies on corporate management, information and control, and preparing the risk measurements that underpin the Group's management. | ||

| GRM regularly reports the management metrics to both the management and administration bodies. | ||

| Responsible for management |

ALCO is the body that makes the decisions to act according to the proposals of the balance sheet management unit belonging to the Strategy and Finance area, which designs and executes the strategies to be implemented, in accordance with the tolerances set out in the risk appetite framework. | |

| Control and management variables |

Availability of collateral to hedge against the risk of wholesale markets closing (basic capacity). | Funding of the loan portfolio through stable customer funds (loan-to-stable customer deposits ratio) and reliance on short-term funding. |

| Management model | Decentralized and independent in each balance sheet management unit/liquidity management unit associated with the different geographica areas. | |

Three core elements: to achieve an adequate volume of stable customer funds; proper diversification of the wholesale funding structure; and availability of sufficient collateral to address the risk of wholesale markets closing

In 2015, both long and short-term wholesale funding markets remained stable thanks to the positive trend in sovereign risk premiums and the setting of negative rates by the ECB for the marginal deposit facility. During the year 2015, the ECB has made, every quarter, targeted longer-term refinancing operations (TLTRO) in order to boost credit while improving the financial conditions for the European economy as a whole. At these auctions, BBVA took €8,000 million in 2015 as a whole.

The situation in the rest of the LMUs outside Europe has also been very positive, as the liquidity position has once again been reinforced in all the geographical areas in which the Group operates.

BBVA continues to maintain an adequate funding structure in the short, medium and long term, diversified by products

In this context of improved access to the markets, BBVA has maintained its objective of strengthening the funding structure of the different Group franchises on the basis of increasing their self-funding from stable customer funds while guaranteeing a sufficient buffer of fully available liquid assets, diversifying the various sources of funding available, and optimizing the generation of collateral for dealing with stress situations in the markets. The exposure to liquidity risk has been kept within the risk appetite and the limits approved by the Board of Directors.

A detailed explanation of the liquidity and funding risk can be found in the Consolidated Annual Accounts, the Management Report and the Auditors' Report and in the Pillar III Report.

Operational risk

Introduction

Operational risk arises from the possibility of human error, inadequate or faulty internal processes, system failures and/or as a result of external events. This definition includes legal risk, but excludes strategic and/or business risk and reputational risk.

Operational risk is inherent in all banking activities, products, systems and processes. Its origins are diverse (processes, internal and external fraud, technology, human resources, commercial practices, disasters, providers).

Operational risk management framework

Operational risk management, which is integrated into the global risk management structure of BBVA Group, is based on the following levers of value generated by the advanced measurement approach (AMA):

Operational risk management principles

The operational risk management principles (detailed in the Consolidated Annual Accounts, the Management Report and the Auditors' Report) reflect BBVA Group's vision of this risk. They are based on the events resulting from this risk have an ultimate cause that should always be identified and managed to reduce its impact.

Irrespective of the adoption of all the possible measures and controls for preventing or reducing both the frequency and severity of operational risk events, BBVA ensures at all times that sufficient capital is available to cover any expected or unexpected losses that may occur.

Three lines of defense in operational risk management

Operational risk management in BBVA is designed and coordinated by the Corporate Operational Risk Management (GCRO) unit, which is part of GRM, and by the Operational Risk Management (GRO) units, located in the risks departments of the different countries (Country GRO). The business or support areas, in turn, have operational risk managers (Business GRO) who report to the Country GRO and are responsible for implementing the model in the day-to-day activities of the areas. This gives the Group a view of risks at the process level, where risks are identified and prioritized and mitigation decisions are made.

Lastly, the control of operational risk management is reinforced by an internal audit process that independently verifies compliance and tests the Group's controls, processes and systems.

Committee structure

Each business and support unit has one or more GRO committees that meet on a quarterly basis. These committees analyze operational risks and take the appropriate mitigation decisions.

In addition, a system called Corporate Assurance has been designed as one of the components of the Group's internal control model. It undertakes a general monitoring of the main control weaknesses submitted to the Corporate Assurance Operating Committee (OCA) at country level, and to the Global Corporate Assurance Committee (CGCA) at holding level.

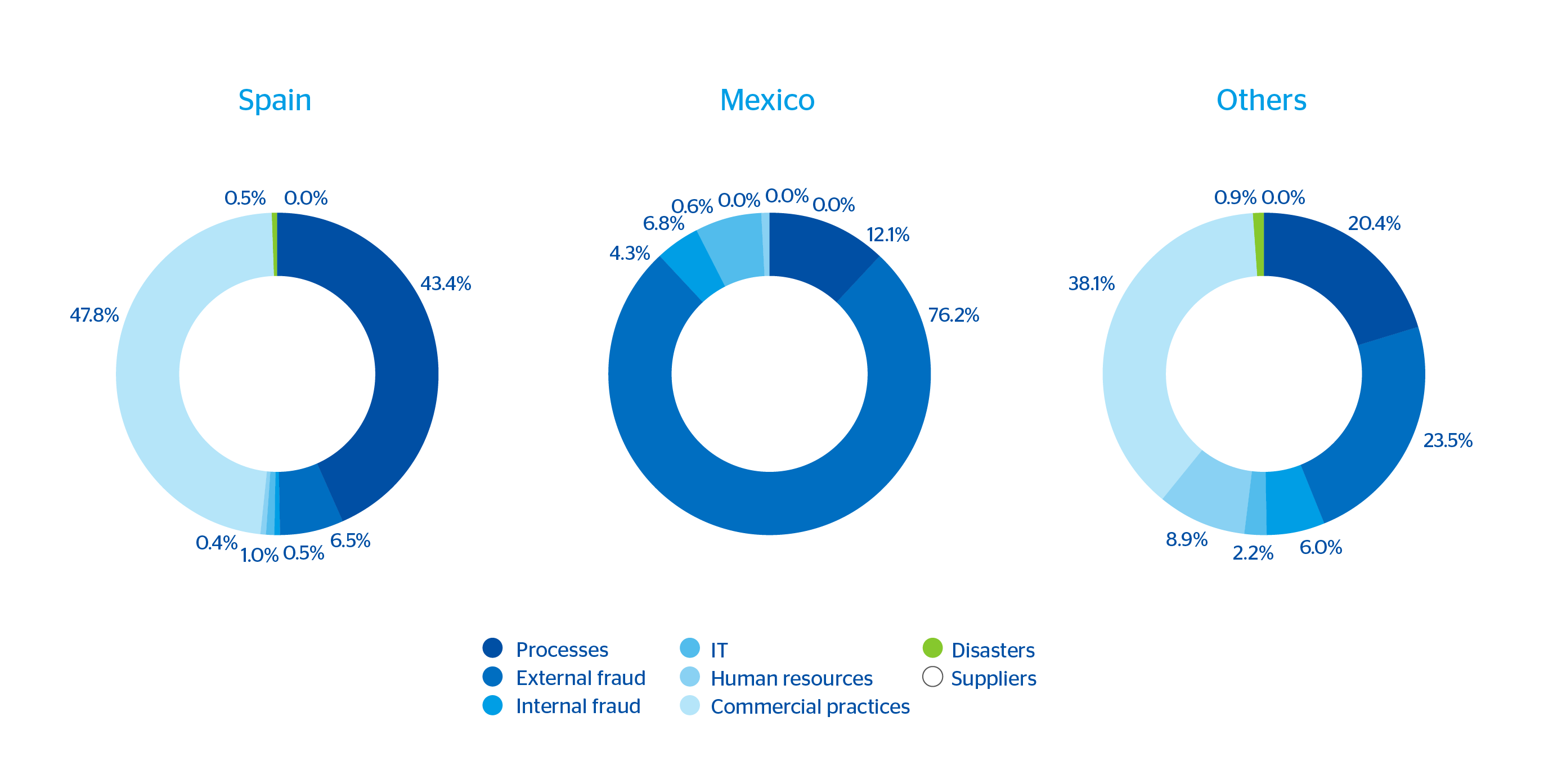

The Group's operational risk profile

The charts below provide a historical distribution of operational risk losses in the different geographical areas where BBVA operates, classified by type of risk.

Historical distribution of losses by type of risk

Operational risk capital in 2015

The methodology used by BBVA to calculate capital using advanced internal models (AMA) is the so-called loss distribution approach (LDA), considered the most robust from a statistical point of view among those permitted by the Basel Committee. This methodology is fed by three data sources: the Group's internal operational loss database, events occurring in the domestic and international financial sector (external database), and simulated events (also called scenarios). BBVA’s application of AMA models has been approved for Spain and Mexico.

The capital resulting from the application of the advanced models is corrected by factors related to the country environment and by internal control factors, based on the variation of metrics on changes in operational risks.

Economic capital by operational risk

(Millon euros)

| Risk class | Capital | Method |

| Spain | 668 | AMA |

| Mexico | 373 | AMA |

| Turkey (1) | 517 | Basic |

| Others (2) | 906 | Standard |

| TOTAL | 2,464 |

(1) Turkey includes the information for Garanti Bank and all its subsidiaries.

(2) Portugal, the United States, Argentina, Chile, Colombia, Peru, Paraguay, Uruguay, Venezuela and Switzerland.

Social, environmental and reputational risks

As a financial institution, BBVA has an impact on the environment and society directly through the consumption of natural resources and its relationship with stakeholders, and indirectly through our credit activity and the projects we finance. These impacts lead to direct, indirect and reputational risks.

These extra-financial risks may affect the credit profile of borrowers or the projects financed, and therefore the quality of the risk assumed and, in short, the repayment of loans.

To manage such risks, BBVA takes into account environmental, social and reputational aspects in its risk management, alongside traditional financial variables.

Their integration into risk management is consistent with the principle of prudence that governs BBVA's activity and is focused on different lines of action.

Social and environmental risk management

Equator Principles

The energy, transport and social services infrastructures that boost economic development and create jobs can have an impact on the environment and society. BBVA is committed to managing the finance of these projects in order to avoid and reduce negative impacts and boost their economic, social and environmental value.

All the decisions on project finance are based on the criterion of return adjusted to principles. Placing people at the core of the business implies dealing with stakeholder expectations and the social demand to fight against climate change and respect human rights.

In line with this commitment, BBVA adhered to the Equator Principles (EP) in 2004. Based on the International Finance Corporation's (IFC) Policy and Performance Standards on Social and Environmental Sustainability and the World Bank's Environmental, Health and Safety guidelines, the Equator Principles are a set of standards for managing the environmental and social risks in project finance. These principles have set the benchmark for responsible finance. Once more in 2015, BBVA has contributed to their development and dissemination as a member of the EP Association Steering Committee and the working groups in which it takes part.

The Corporate & Investment Banking (CIB) Reputational Risk team takes on responsibility for analyzing the financed projects, representing the Bank before stakeholders, being accountable to senior management and designing and implementing the management system, proposing the adoption of best practices and contributing toward training and communication on matters related to the EP. In 2015, representatives of the Reputational Risk team took part in training sessions given by the IFC, OECD and IAIA on the best environmental and social risk practices.

In the risk analysis and decision-making processes, BBVA assesses and takes into consideration not only financial aspects, but also social, environmental and reputational factors

Project analysis involves subjecting each transaction to a process of environmental and social due diligence that starts with assigning a category (A, B or C) which reflects the project's level of risk. The documentation submitted by the customer and the independent advisors is reviewed, allowing the level of compliance with the requirements established in the EP to be graded in accordance with the project category. Finance agreements incorporate the customer's environmental and social obligations, which are monitored by a specialist CIB team.

Initial review

- Selection of independent advisor

- Project classification

Due diligence

- Review of the Environmental and Social Impact Assessment

- Environmental and Social Due Diligence Report

Approval

- Sanction by the CIB Reputational Risk Department

- Inclusion of conditions in the approval of the Risks Committee

Financial close

- Preparation of an Action Plan

- Environmental and social clauses in the finance contract

Monitoring

- Monitoring reports by the independent advisor

- Report on the environmental and social impact of the project

To guarantee integrity in BBVA's application of the EP, their management is integrated into the internal transaction structuring and admission processes and is subject to regular checks by the Internal Audit Department.

For BBVA, the EP are the basis for applying best practices in responsible finance and the framework for dialog with customers and stakeholders in the projects we finance.

BBVA's best practices in environmental and social risk management include:

- Elimination of the minimum threshold of US$ 10 million established by the IFC, reviewing all operations under the EP, regardless of the amount.

- Application of the EP beyond their mandatory scope, incorporating project bonds, assignment of credit rights, asset finance and project-linked guarantees.

- Review of projects at the operation phase, as well as new projects.

- List of preferred independent advisors.

- Public information broken down by project.

BBVA Group. Details of Equator Principles operations

| 2015 | 2014 | 2013 | |

|---|---|---|---|

| Number of operations | 26 | 44 | 28 |

| Total amount (million euros) | 24,557 | 170,265 | 7,934 |

| Amount financed by BBVA (million euros) | 1,933 | 1,867 | 719 |

Appendix RI1 - Classification of finance and advisory projects according to the EP

Ecorating and training in social and environmental risks

The Ecorating tool is used to rate the risk portfolio of SMEs from an environmental point of view. This is done by assigning a level of credit risk to each customer in accordance with a combination of several factors such as location, polluting emissions, consumption of resources, potential to affect the environment or applicable legislation. In 2015, the environmental risk of 216,976 customers was rated in Spain, with a total exposure volume of €98,914m.

Spain. Eco rating data 2015

| Environmental risk level |

Volume (million euros) |

Customers |

|---|---|---|

| Low | 86,003 | 177,459 |

| Medium | 12,683 | 38,976 |

| High | 228 | 541 |

| TOTAL | 98,914 | 216,976 |

As regards training, in 2015 BBVA continued to award grants to risk analysts to complete the Environmental and Social Risks Analysis Online Training Program provided by the United Nations Environment Program Finance Initiative (UNEP FI) and delivered by INCAE Business School. Over the year, four of the Group's risk analysts have received the 30-hour online training.

Reputational risk management

Since 2006, BBVA has had a methodology in place for identifying, evaluating and managing reputational risk. Through this methodology, the Bank regularly defines and reviews a map in which it prioritizes the reputational risks it faces, together with a set of action plans to mitigate them.

This prioritization is carried out according to two variables: the impact on stakeholder perceptions and the strength of BBVA's resilience to risk.

This reputational exercise is carried out in each country, and the integration of all of them leads to a consolidated view of the Group.

In 2015, progress was made in defining a more solid governance model, the methodology has been improved and a software tool has been developed for its management.

According to this new governance model, two groups have been defined as responsible for the design and implementation of the methodology to identify and promote reputational risk management: one at the global level and the other locally. In both cases, they are made up of the managers of Internal Risk Control & Operational Risk, Compliance, Communications and Responsible Business.

Two types of key functions are involved in the implementation of the methodology:

- The Responsible Business and Communications teams, responsible for identifying risks and assessing their impact.

- The assurance providers, responsible for assessing and mitigating the risks identified. They come from very different areas because reputational risks are very varied in origin.

Each of these functions must report about the reputational risk management within its scope of action through the reporting channels it uses normally. The aggregate view of the reputational risks is reported according to local regulatory requirements.

Responsible lending

BBVA has incorporated the best practices of responsible lending and consumer credit granting and has policies and procedures that contemplate these practices.

Specifically, the Corporate Retail Credit Risk Policy (approved by the Executive Committee of the Board of Directors of the Bank on April 3, 2013) and Specific Rules derived from it establish policies, practices and procedures in relation to responsible granting of loans and consumer credit.

The summary of these policies are available in the BBVA Financial Statements.