Customers

The best customer experience

Financial institutions are experiencing a technological revolution. Users and consumers are adapting to digital interaction in all aspects of their lives. They want their financial institutions to update and allow them to access their finances any time, any place.

At BBVA we have been preparing for success in this new environment. Our goal is to be the best Bank for our customers. That is why we aim to become an organization driven by data and information, which offers new and better products and services adapted to each customer's needs and expectations.

But the transformation of the financial industry is not only based on the digitalization of financial services; it also has to remodel the customer experience. Because digital innovation helps people manage their money better.

To address these new challenges, BBVA has set up a new global unit called Customer Solutions. Its objectives are to:

- Lead the creation of simple, intuitive and transparent products through a different definition of users and their experience, with a design focused on mobile devices and using customer-centric techniques.

- Develop global products using scalable technology that can be easily adapted to different geographical areas.

- Boost personalized contextual experiences through intelligent data engines (big data).

- Rigorously use analytics for decision-making across customers' life cycles, meeting both their current and future needs.

BBVA has set up a new global unit called Customer Solutions, geared to providing the best customer experience

Thus, we are committed to a model in which it is the customers who choose how they want to receive a service at any time and for each need, whether digital, remote or in person; allowing them to manage their financial life better, with tools, information, products and services that contribute real added value.

BBVA's goal is to be "the most recommended Bank, with the best customer experience, adapting ourselves to our customers and making all the channels available to them."

BBVA's customer-centric strategy ensures a high recurrence of earnings and a stable business.

At BBVA we believe in a model of relating to our customers in which they choose how they want to interact with the Bank

IReNe and feedback

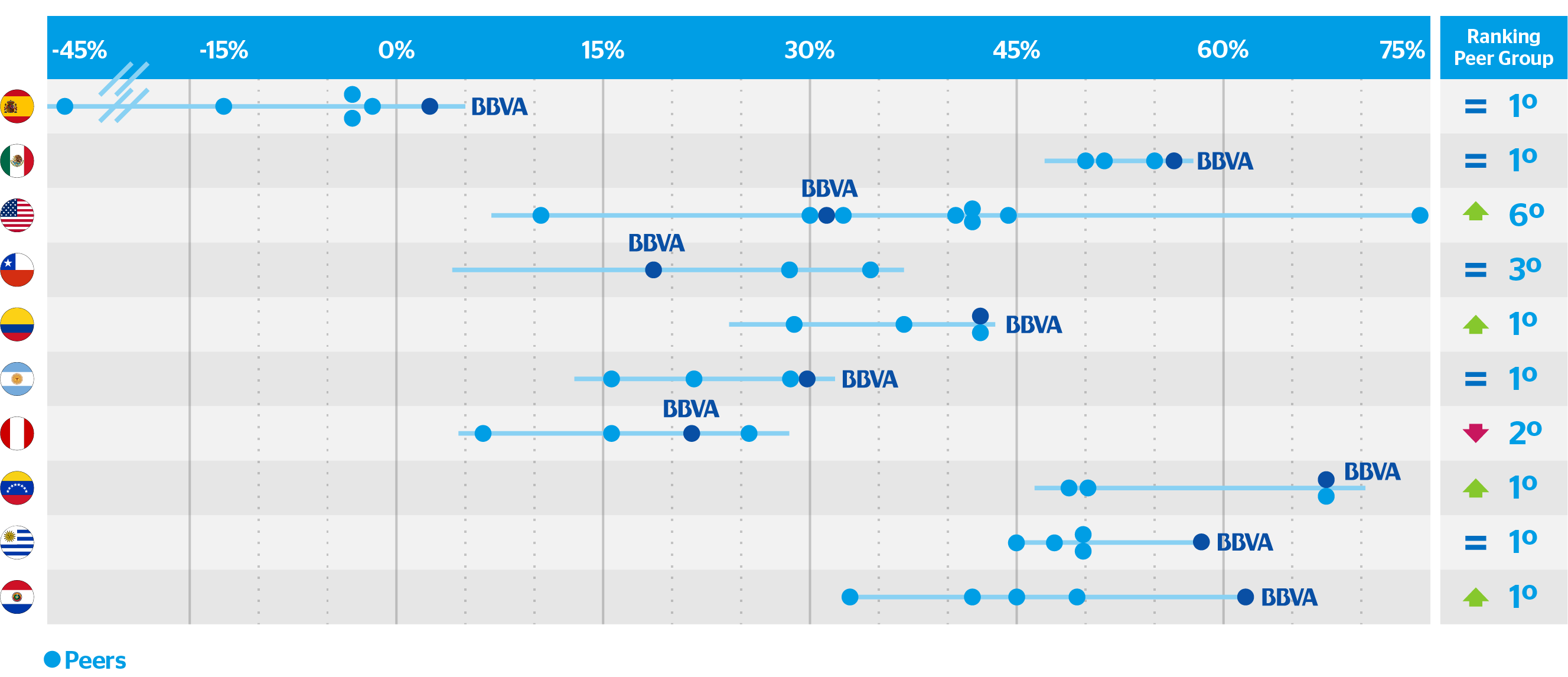

Over the last four years, the Customer Experience areas have consolidated the implementation of a global methodology based on customer recommendations, called IReNe (Net Recommendation Index). Progress is being made in the way we listen to our customers, giving us an in-depth understanding of their needs.

This methodology and its surveys give us an understanding of BBVA's competitive situation and our position with respect to our competitors in terms of recommendations in each country.

IReNe, a global methodology based on customer recommendations; digital feedback, a platform designed to understand our customers' needs

Net promoter score by geography

In 2015, BBVA has been a model in the financial sector with respect to customer experience and levels of recommendation, because in 80% of the countries where we have a footprint, we are in first or second place on the IReNe ranking in our market peer group.

In addition, we have begun to use a digital feedback platform to understand our customers' needs. Thus, at the product and service creation stage, we collect customer opinions quickly and efficiently, allowing us to learn from customer experience in real situations. Below we analyze the results to identify factors and trends. Every idea that arises is an opportunity we can incorporate into our designs, and in this way we meet our customers' needs and expectations.

In short, we turn real customer experiences into ideas. We create this different experience that distinguishes us from our competitors and turn our customers into brand advocates.

Quality initiatives in 2015

Thanks to the IReNe methodology, we know the assessment by type of customer and relationship channel, so we have the elements we need to establish quality plans and integrate the customers' priorities into the Group's transformation projects.

The efforts made by all the areas continue to be geared toward a determined and continuous execution of the quality plans and actions that BBVA has implemented. They are having an effect on increasing customer satisfaction and recommendations, with the aim of offering customers the best experience in banking services.

Initiatives to improve the quality perceived by our customers are giving very good results

The following table sums up the most important initiatives:

| Spain | Implementation of the program “Calidad en Red Banco 10”. |

|---|---|

| Launch of digital feedback in BBVA.es for all the relevant servicing, recruitment and new function processes. | |

| Mexico | Implementation of the customer feedback methodology in the commercial network through daily online surveys, which allow an evaluation to be made of customers’ most recent (less than 48 hours) experience with BBVA. |

| Launch of digital feedback, in the Bancomer.com, Bancomer Móvil and WIBE products. | |

| Argentina | Improvement in claims processing, with an impact on customer experience. |

| Implementation of the "VIP Segment Experience" care and service model. | |

| Chile | Implementation of the Customer Experience Model. |

| Improvement plan in strategic products. | |

| Colombia | Implementation of the customer feedback methodology in the commercial network through daily online surveys, which allow an evaluation to be made of customers' most recent (less than 48 hours) experience with BBVA. |

| Implementation of the customer service process on social networks. | |

| New requests, complaints and claims management tool, "rapidez de respuesta". | |

| Paraguay | "En Sintonía 2.0" culture of quality program. |

| New CRM for complaints, with improvement plans at resolution service level. | |

| Peru | Implementation of the customer feedback methodology in the commercial network through daily online surveys, which allow an evaluation to be made of customers' most recent (less than 48 hours) experience with BBVA. |

| Reengineering in the complaints management model. | |

| Methodology of Internal IReNe surveys that evaluate the staff and branch network support areas. | |

| Uruguay | Coaching model: the network and those responsible for customer experience. |

| Optimization of the complaints management process (internalization, improvement of response times and quality). | |

| Cards: delivery of cards, state of accounts and improvement of experience. | |

| Venezuela | Permeability of service quality in central areas (BBVA experience-Internal IReNe). |

Complaints and claims management

Customer complaints and claims are an excellent starting point for improving BBVA Group's processes because they tell us exactly which areas need to be changed to make life easier for our customers. The current economic situation, growth of the business in other regions and more demanding financial rules and regulations for financial institutions are all forcing us to make a bigger effort to handle our customers' requests or disagreements.

Our customers' complaints and claims indicate ways we can make their lives easier

At BBVA we understand that a complaint is any kind of disagreement (financial or not) with one of the Bank's products or services by a customer in the terms established in the regulations in force in that country, as registered by the Bank and to which a response has to be made within a specific time.

Since 2007, the Global Quality Department has published a corporate report on the management of complaints and claims that arise within the Group. The process was moved to the intranet/wiki format and this year a special effort has been made to create a specific site in order to obtain all the information needed for periodic reporting and monitoring of this matter.

Spain, Mexico and South America. Main indicators of complaints

| 2015 | 2014 | |

|---|---|---|

| Average time for settling complaints (days) | 11 | 12 |

| Number of claims settled by First Contact Resolution (FCR) (%) | 30 | 14 |

| Number of claims before the banking authority (for each billion euros of activity) | 21 | 131 |

This site is for internal use and is organized into a number of aspects. First, it deals with the different fields in the area of complaints, but from a more dynamic approach. Second, it always tries to contribute value to internal customers that can be passed on to external customers.

In BBVA Group, the different complaints units are constantly evolving with the aim of improving and optimizing their management models. The Contact Center is still the main channel for receiving and managing claims for some countries in South America; and cards, particularly credit cards, are the product that receives most claims.

There is also a growing awareness of the need to collect and deal with informal customer complaints or claims, with the aim of having this rich information available in order to analyze the root causes and establish action plans to deal with them in time.

We are improving our processes so that we can quickly pass on everything we have learned in relating to our customers within the Organization

The following are the conclusions of the complaints management process in BBVA:

• We have identified in depth the root causes of problems.

• We have improved customer experience with the closing of the IReNe process cycle.

• The Bank's digital transformation process has been supported by sharing customer insights (IReNe, feedback, complaints and claims, etc.).

• And activity continues to be reported periodically at the Group level in order to share best practices.

Appendix CL1 - Average time for settling complaints by country

Appendix CL2 - Number of claims settled by FCR

Appendix CL3 - Number of claims before the banking authority

Customer protection

Operational and technological risk management

In 2015, as part of the organizational reconfiguration of the Engineering area, a control function called Engineering Risk & Corporate Assurance has been set up, with the aim of developing and maintaining the control model, as well as managing active risks related to business and technological processes, within the framework of the Corporate Assurance model.

As part of the business process control model, in 2015 the operational control function has focused on implementing a new scheme of standardized control in all the Group's companies and businesses, with the focus on the most relevant processes and risks. At the same time, significant progress has been made in managing the main operational weaknesses.

In terms of technological risk, the Group has continued to make progress on the three pillars that make up this discipline: information security, technological fraud management and IT risk management.

It is worth highlighting the effort made this year in terms of adapting the levels of information protection to the new challenges arising from the Group's digital strategy.

At the same time, in 2015 BBVA CERT (Computer Emergency Response Team) has consolidated its position as the nerve center of BBVA Group's cybersecurity and fraud strategy. CERT carries out all the monitoring, immediate response, limitation and investigation of incidents 24/7, supported by sound analytical and intelligence capabilities to handle cybersecurity or fraud threats.

In 2015, BBVA has made major progress in the management of operational and technological risks related to customer protection

BBVA has a continuous cybersecurity monitoring and improvement plan in place called the Cyber Trust Program. It provides a dynamic, structured and standardized response to the challenges that arise in the current cyberthreat scenario. A number of projects have been developed as an integral part of the Cyber Trust Program over the last five years. They aim to secure internal and external (perimeter protection) channels and communications, as well as the management of access by customers through robust authentication processes and mechanisms, such as two-factor authentication. More recently, projects have been implemented designed to protect the applications developed for access by customers to the different technological channels.

In addition, a technological risk measurement methodology has been developed and implemented in 2015, based on indicators linked to the international Cobit 5.0 standard. BBVA has also initiated a process of adopting the standard issued by NIST (National Institute for Standards and Technologies) relating to cybersecurity, as a framework of reference for management and control.

Lastly, in the area of business continuity improvements continue to be made to the different procedures for recovering content in the case of low-probability but very high-impact events. In this respect, work has been done in 2015 to update and improve the plans through technical and crisis management tests that also allow training of the people involved in these situations. Some of these plans have been fully or partially activated during the year, as in the following cases: the eruption of the volcano Calbuco on the border between Chile and Argentina; the threat posed by Hurricane Patricia in Mexico; and minor seismic movements that nevertheless affected operations in the state of Mérida (Venezuela) and the north of Chile.

Regarding personal data protection in Spain, some improvements have been conducted during 2015. These improvements were noted in the action plans based on the biennial audits on the security measures demanded by the Royal Decree 1720/2007 of 21 december, which were carried out during 2014 in the BBVA Group companies in Spain with no significant shortcomings.

Furthermore, the process of adapting, improving and standardizing the personal data protection activities that must be carried out in each jurisdiction where BBVA Group operates was also continued in 2015. The adaptation and implementing activities that have been conducted in BBVA Colombia and BBVA Continental are especially relevant in order to comply with the new regulatory requirements established in Colombia and Peru.

Transparent, Clear and Responsible Communication

The project for Transparent, Clear and Responsible Communication (TCR) has the goal of helping our customers to make informed decisions over the whole life cycle of their relations with the Bank. As well as taking care of their interests, we want to set ourselves apart from our peers as the clearest and most transparent Bank for our customers in each market, while increasing consideration and recommendations.

We consider this initiative to be a key element for generating an excellent customer experience and for driving sales, especially in digital channels, thus complying with two of the Bank's strategic priorities.

What does being TCR mean in the relation with our customers?

-

Transparency: means providing all relevant information to the customer, and maintaining a balance between benefits, costs and risks.

-

Clarity: means that the customer easily understands from the start the information or process we are communicating. Clarity is closely related to language and also to the structure and organization of information; and in digital channels it is linked to navigation.

-

Responsibility: means looking after the customer’s interests in the short, medium and long term.

In 2015, BBVA continued and strengthened its work on the initiatives it had already been carrying out in 2014:

TCR product leaflets

They describe the products not only in terms of advantages but also the costs and risks involved in them, with a clear language and a glossary of the inevitable technical words and phrases used. They are tested in advanced, and given to customers when they show an interest in a product, before they buy it.

The project was implemented in Spain and Mexico in 2014; and in 2015 the implementation was completed in Argentina, Chile, Colombia, Peru, Venezuela and the United States. In all there are more than 377 product leaflets implemented, meaning they are easily available to executives or branch managers. They cover at least 80% of the contracts in each of these countries.

For 2016, the challenge we have set ourselves is to ensure they are provided on a regular basis.

TCR contracts

This initiative involves reworking current customer contracts and structuring them more intuitively with language that is easy to understand.

In 2014, the legal services teams drew up and tested the first contracts using TCR criteria.

In 2015, these teams drafted TCR contracts for the five most commonly sold products in each geographical area. In the United States, Argentina, Chile and Peru, these contracts have already been fully implemented. In the other geographical areas, work on implementation is still being carried out. In all there are 22 products regulated by TCR contracts.

For 2016, the challenge is to implement TCR contracts for at least 80% of the contracts in all the geographical areas. In addition, in 2016 a guide will be introduced for drafting and distributing TCR contracts, more focused on distribution through digital channels.

TCR communication: a key element in generating a differential customer experience

TCR advertising

The aim of this initiative is for the Group's advertising communication to be transparent, clear and responsible. To this end, in 2014 we prepared a TCR Advertising Communication Code, which is a self-regulation document that contains the principles to be followed in the Group's entire advertising communication.

The Code entered into force on January 1, 2015 and must be complied with by all the Group's communication and marketing teams. It was presented by the Group Executive Chairman in April 2015 on the 20th anniversary of Autocontrol, the Association for Self-Regulation of Commercial Communication.

Workshops have been organized to extend knowledge and compliance at the global level, especially for the marketing teams, legal services, product managers and advertising agencies. They learn how to use the Code in practice. Over 200 people have taken part in these workshops and have rated them with an average score of 4.8 out of 5. An email address has also been made available in each geographical area to which employees can send queries, questions or suggestions for improvement. Lastly, an online test has been implemented for which the marketing teams of all the geographical areas have been signed up with the aim of ensuring it is known and read by all the employees.

Digital TCR

Most of BBVA's digital content and solutions are produced under the Agile methodology. To guarantee that the groups working with this methodology are producing TCR documents, we have carried out the following actions in 2015:

- Drafting of a checklist of the 15 most important TCR principles in digital channels, explaining each of the principles with examples of good and bad practices.

- TCR and human-centered design training workshops for members of the scrums who work on solutions and/or content for customers. Some 395 people have taken part in these workshops, with an average recommendation score of 4.6 out of 5.

- Direct support for some of these working groups.

The challenge in 2016 is to ensure that the TCR checklist is always part of the work routine of these working groups.

Metrics

In 2015, we have also improved the way in which we measure whether we are TCR for our customers. We have done this by incorporating a question in the local Net Promoter Score (NPS) open-market surveys that allows us to position ourselves with respect to our peers. We have also included questions relating to TCR in the questionnaires that measure the quality of service provided by managers and the quality of the contracting process. We have also analyzed customer behavior and perceptions in our digital channels, especially the Internet.

Financial Literacy

Financial literacy (FL) is one of the strategic priorities of BBVA Group's Responsible Business Plan and is constructed through the Global Financial Literacy Plan. Our goal in this area is to promote the development of the financial skills that allow society to make informed decisions to improve its financial well-being and be more aware of the existing risks and opportunities.

Together with TCR Communication, at BBVA we work to ensure that financial literacy is part of our day-to-day relationship with our customers, and of our products and services, in order to ensure they are better explained and understood. As well as financial literacy workshops, we work hard to make training content available through the mass media, conveying clearly presented messages, mainly through social networks and through our local websites in Spain, Chile, Colombia, Mexico and Venezuela.

At BBVA we create our own programs to promote financial literacy at the global level, but adapting them to the environment and local economic reality. They must be targeted at a diverse audience, including children, young people and adults.

We must not forget the growing importance of businesses, especially SMEs, which play a crucial role in the development of the economic and business fabric across our global footprint. At BBVA we target initiatives at this group in order to strengthen the capabilities of people who work in these organizations and boost the growth of small businesses, providing financial, business and management training to entrepreneurs whose projects generate social impact and are sustainable.

At BBVA we work to help people make better financial decisions

Main progress in 2015

The investment in the development of the Global Financial Literacy Plan was 12.4 million euros and reached 1.53 million beneficiaries.

BBVA Group. Beneficiaries of the Global Financial Literacy Plan

| 2015 | 2014 | 2013 | |

|---|---|---|---|

| Children and young people | 1,108,755 | 1,009,430 | 1,093,071 |

| Adult | 368,055 | 244,543 | 226,462 |

| SMEs | 59,398 | 41,474 | 20,016 |

| Total beneficiaries Financial Literacy | 1,536,208 | 1,385,447 | 1,339,549 |

| Total number of workshops | 1,076,452 | 1,010,681 | 1,000,039 |

| Total investment in FL (million euros) | 12,448,665 | 17,427,972 |

13,558,503

|

We have a long-term commitment to financial literacy, with over 42 million euros invested and over 4.2 million participants in the various programs since 2013

Financial literacy is on the agenda of public bodies and regulators, so we have a major institutional commitment. In 2010, we began our partnership with the Organization for Economic Cooperation and Development (OECD) to make the PISA financial literacy test possible. With over 30 million young people aged 15, 4,000 participating schools and 26,000 children assessed, the results of the 2012 PISA financial literacy test showed broad scope for improvement in most participating countries.

In 2014, the agreement between BBVA and OECD was renewed to continue to promote this financial culture test.

The fieldwork for the second PISA financial literacy test in 16 countries was carried out in 2015. Among the countries where BBVA operates, Spain, the United States, Chile and Peru have p<articipated. With a contribution of €1,630,000 we are maintaining our commitment to the advocacy and promotion of collective initiatives.

Appendix EF1- Number of beneficiaries by geographical area 2015

Financial literacy for children and young people

At BBVA we promote financial literacy to improve financial culture and the values related to the responsible use of money in order to prepare children and young people for their future.

The programs are developed by educational experts through workshops in schools, and in some countries through online courses, with cross-curricular material available for teachers and educators. In the case of children aged 6 to 14, the workshops promote the development of values associated with the use of money (effort, solidarity, savings, etc.) and the acquisition of financial culture skills in line with the PISA Financial Literacy Report. For young people aged 14 to 18, the programs are focused on knowledge of basic financial concepts and planning of their personal economy.

We promote financial literacy as a cross-curricular subject to increase the financial culture and the values associated with the responsible use of money in order to prepare children and young people for their future

Of particular note is the Valores de Futuro (Future Values) initiative that was created in Spain in 2009, and extended to Portugal and later to Mexico, in 2012. In 2015, Valores de Futuro involved 4,548 schools and 967,612 students in Spain. In Mexico, 16,523 school students took part in the Valores de Futuro workshops. The program is focused on group awareness workshops (over 60) in the classroom, given by teachers and in some cases with the participation of volunteers from BBVA.

For the second year in a row, BBVA Bancomer has won the "Children's Financial Literacy Program of the Year" award of the EIFLE Awards (Excellence in Financial Literacy Education) by the Institute for Financial Literacy for its Valores de Futuro initiative, which demonstrated exceptional innovation, dedication and commitment to financial literacy.

In 2015, a collective initiative promoted by the Spanish Banking Association (AEB) was carried out for the first time in Spain, with the participation of 15 financial institutions. The financial literacy program Tus Finanzas Tu Futuro (Your Finances, Your Future) is aimed at promoting financial competence among young Spanish people aged between 13 and 15. It benefited 6,750 students in 93 schools across Spain.

The financial literacy program for children “Valores de Futuro” has consolidated as a referent in Spain and in Mexico with more than 984,135 beneficiaries in 4,579 schools

In Chile, the Liga de Educación Financiera BBVA (BBVA Financial Literacy League) for young people aged between 14 and 17 has benefited 7,760 young people by promoting a didactic and interactive game with which they can learn and practice responsible financial concepts and behavior.

The financial literacy program Becas de Integración BBVA Francés (BBVA Francés Integration Scholarships), which was launched in 2012 in Argentina, has increased the number of participating schools each year, thanks to the involvement of volunteers from BBVA. In 2015, 235 schools were visited and over 1,452 students experienced the workshops that promote responsibility and the administration of money with the aim of including young people in the financial system.

In collaboration with the American Bankers Association, BBVA Compass has run the financial literacy programs for children and young people called Teach Children to Save and Get Smart About Credit. This is a program that, thanks to the collaboration of volunteers from participating banks, helps young people to develop saving habits. In 2015, there were 27,920 beneficiaries. In addition, BBVA Compass continues its partnership with EverFi (the leading educational technology company focused on learning) and Junior Achievement, for the development of the BBVA Compass Future Builders Program. This program invites students to make decisions in real-life scenarios to achieve better goals for saving and planning. In 2015, 38,378 young people benefited from the program.

Financial literacy for adults

The financial literacy initiatives for adults aim to help them make informed decisions through workshops, seminars and tools, on-site and online, on matters related to their financial life cycle.

Financial literacy for adults contributes to informed decision-making and, thus, promotes consistent savers and responsible debtors

Adelante con tu Futuro (Forward with your Future) is an initiative that is worth highlighting. It was created in Mexico in 2008 and has already been extended to Chile, Colombia, Paraguay, Uruguay and Venezuela.

This financial literacy program run by BBVA Bancomer has the largest infrastructure of any financial literacy program in Latin America, with 20 fixed classrooms, 15 mobile classrooms, 15 mobile teams and 100 instructors. The content is aligned with the life cycle of people and provides them with the tools they need to better manage their finances at different stages of their lives. It has 10 free workshops: saving, saving for retirement, credit cards, credit health, mortgages, life insurance, investment funds, electronic banking, stock market literacy and economics and banking. Adelante con tu Futuro has run over 3 million on-site and online workshops, benefiting more than 1,200,000 people since its launch in 2008.

In other countries such as Chile and Colombia, initiatives have consolidated during 2015 that foster financial literacy at the workplaces of companies and institutions that are customers of BBVA through workshops for the company employees. This program is also run in Mexico. Over 34,000 people have participated in these workshops in 2015.

Adelante con tu Futuro has benefited more than 1 million people since 2008. We have increased the range of programs, some of them consolidating their position, such as Mi Jubilación

BBVA Compass offers the Money Smart initiative for adults in collaboration with the Federal Deposit Insurance Corporation (FDIC). This program is designed to help people, whether bank users or not, to acquire financial knowledge and use banking services effectively. It is run with the collaboration of employees from BBVA Compass and community organizations. In 2015, 19,481 people benefited from this program. As part of the initiative, BBVA Compass has made the successful completion of a course in the Money Smart program a requirement for first-time mortgage applicants.

The Mi Jubilación (My Retirement) initiative, launched in 2013 in Spain and Portugal, has consolidated its position in 2015 as a model for information related to retirement and pensions. This is evidenced by the number of visits received on its website, at over 130,000 in 2015 (up 46% on the figure for 2014), and the number of people who have used the advice tools, with over 150,000 simulations (up 125% on 2014). Work is continuing in the strategic part of Mi Jubilación on three lines related to retirement and pensions:

- Economic research on pension reform issues, through the BBVA Pensions Institute.

- Contribution to the pension dialog, with proposals that guarantee the future of pensions.

- Financial literacy for society, providing information and knowledge about pensions in order to make informed financial decisions.

In 2015, the digital presence was extended through the website www.actibva.com for increasing information and awareness of financial skills that make society more aware of financial risks and opportunities, as well as able to take informed and effective decisions to improve personal financial well-being.

Business training

Businesses, especially SMEs, play a crucial and increasingly important role in the development of the economic and business fabric in the countries across our global footprint.

Financial literacy for SMEs:

We support the development of financial skills through training workshops on subjects related to financial decisions in the area of SMEs to allow them to improve their financial stability, access to finance and growth, with efficient credit management, cash flow and other financial resources.

It is worth highlighting the financial literacy programs for SMEs in Mexico, which since 2012 have provided entrepreneurs and micro-businesses, whether customers or not, with support through on-site and online workshops: interactive videos and practical exercises. They also have instructors skilled in boosting financial viability and solvency with the correct use of cash, supporting growth through identification of types of credit and their appropriate use, and explaining the advantages of interest-rate hedges for businesses.

We promote financial literacy for SMEs and entrepreneurs to support their development, sustainability and social impact

Training for growth:

Business training initiatives are targeted at boosting the growth and development of SMEs so that they can have a future. These initiatives are based on value solutions that include:

- Training programs for comprehensive management of companies; specific workshops given by business schools and developed in a networking environment; and support for SMEs.

- Programs aimed at speeding up the growth of SMEs, working on their strategic projects through a specific program given by leading local universities.

- Programs supporting social enterprises to consolidate and extend their economic and social impact through a complete training program, strategic support and finance.

In Spain, the training program under the Yo Soy Empleo -YSE- (I am employment) initiative, launched in 2013, continued in place. New on-site training sessions for SMEs and self-employed workers were developed in 2015, given by the top business schools in Spain at no cost for the companies involved.

In 2015, the regional training for growth program Camino al Éxito –CaE- (Path to Success) was consolidated in South America, specifically in Argentina, Chile, Colombia, Peru, Paraguay, Uruguay and Venezuela. This regional program has allowed companies to access courses designed to address their needs, given by top local universities and business schools. In 2015, a total of 728 SMEs took on-site courses in South America. At the end of the program, over 425 of the companies taking part had developed a strategic project that can lay the foundations for their growth. Camino al Éxito has made use of a digital platform with more than 28,196 users registered, who have had access to a broad catalog of online content, with training clips for finance, leadership, and people and business management. In addition, Camino al Éxito rewarded and recognized the best SME growth projects through the Camino al Éxito awards, held at the local level and for the region of South America as a whole.

In recent years, together with the Financial Literacy workshops, BBVA Bancomer has developed a broad range of skills training that aims to support SMEs with major growth potential through cognitive tools and management and administrative skills, that allow them to consolidate and make their projects grow. In 2015, two important programs have been implemented. One of them gives access to a diploma from Universidad Anáhuac after more than 110 hours of blended training in which 911 companies took part; and the other is an on-site program aimed at a segment of SMEs with high potential, given by IPADE (considered the most prestigious business school in Mexico), which has benefited more than 71 medium-sized companies.

Since 2013, BBVA Compass has offered the Money Smart program for SMEs, through 10 training modules that provide knowledge of organizational basics and business management for entrepreneurs and startups. With 31,682 companies benefiting in 2015, the program has consolidated its position as a lever for the development of SMEs.

Of particular note are initiatives adapted to the local environment, such as the Women Entrepreneur Executive School program, implemented in 2012 by Garanti Bank in Turkey for training women entrepreneurs through the Boğaziçi University Lifelong Learning Center. As part of the program, women entrepreneurs receive 100 hours of training on subjects such as business creation, innovation and sustainable management. Since 2015, initiatives have been developed in collaboration with various local organizations to boost the process of digitalization in Turkish SMEs.

Appendix EF4 - Training for business

In the area of support for social enterprises, in 2015 we continued boosting the growth and consolidation of innovative social enterprises through Momentum Project. This is a program carried out in coordination with top business schools and involves the participation of BBVA executives who provide a pro-bono strategic mentoring service.

The program was set up in 2011 and is currently available in 3 countries: Spain, Mexico and Peru. Since it was launched, 92 companies have participated in the comprehensive training, strategic mentoring, visibility, financing and follow-up program for participating entrepreneurs, to consolidate and boost their social impact.

A total of 1,544,441 people have benefited worldwide.

In Spain, BBVA has financed 18 companies out of the 56 participants in Momentum Project since 2011, with investment of more than €5m.