Following the agreement reached in July 2013 for the sale of the Group’s banking business in Panama, the assets and liabilities of this unit have been reclassified as “non-current assets held for sale” and “liabilities associated with non-current assets held for sale”. The comments on the rates of change in activity in the area are therefore affected by this reclassification.

Performing loans in South America closed September with a balance of €45,661m, a year-on-year growth of 17.3%. In line with previous quarters, there has been a notable performance of lending in the individual segment, which has risen over the same period by 21.5%, boosted by the positive performance of consumer finance (up 20.9% year-on-year), credit cards (up 44.1%) and mortgages (up 14.9%).

This increased activity continues to be subject to rigorous risk admission policies applied by the Group in the region. As a result, the risk indicators have remained stable. The NPA ratio at the close of September remains at 2.2% and the coverage ratio at 137% (136% at the close of the first half of 2013).

Customer deposits under management maintain their high rate of growth, up 27.1% year-on-year, and with a balance as of 30-Sep-2013 of €54,984m. This growth is basically the result of a further rise of 44.5% in current and savings accounts. With growth rates above the market average in the area, the year-on-year market share of total on-balance-sheet funds increased by 24 basis points to the close of July 2013 (the latest available data). If the mutual funds managed by the banks in the area are included, the customer funds managed by South America increase to €57,931m (up 25.6% year-on-year).

By countries, the highlights of banking activity are as follows:

- In Argentina the loan book increased (27.9% year-on-year) above the rate reported by the system as a whole. As a result, there has been an increase of 23 basis points in market share over the 12 months (data as of the close of July 2013, the latest available information). By portfolio, consumer finance and credit cards performed outstandingly well, and increased their market share by 18 basis points, as did mortgage loans, which gained 35 basis points in the same period. On-balance-sheet customer funds grew at a similar rate as performing loans, at 27.1% on the close of September 2012.

- Chile posted a major increase in the mortgage loan book, with a year-on-year increase in market share of 39 basis points, according to the latest available information as of the close of July 2013. Performing loans in the unit increased over the 12 months by 7.6%. On-balance-sheet customer funds have once more increased by 14.2%. Current and savings accounts performed particularly well and increased their market share by 3 basis points over the last 12 months.

- Colombia’s sustained growth in activity has outperformed the system as a whole. As a result, it has gained market share in both lending (up 11 basis points compared with the figure at the close of July 2012) and, in particular, customer funds (up 149 basis points). As in previous quarters, as a result of the area’s strategy of focusing on the retail segment, most lending growth is related to the consumer portfolio and credit cards (a gain of 100 basis points in market share over the last 12 months). This rise in on-balance-sheet customer funds, is due to a combination of positive performance by current and savings accounts (up 132 basis points) and time deposits (up 168 basis points).

- In Peru, lending has grown by 14.2% year-on-year, thanks to mortgage loans, the segment with the highest growth rate (up 20.6%), followed by the consumer finance portfolio (up 6.4%). On the liabilities side, there has been a year-on-year growth of 16.1% in on-balance-sheet customer funds, with a very favorable performance by current and savings accounts (up 23.2%).

- Venezuela: loans have increased by 53.3% and on-balance-sheet customer funds by 70.3% on the figures at the close of September 2012. On-balance-sheet funds have gained 12 basis points of market share year-on-year (also with data for the close of July 2013) thanks to the boost from current and savings accounts, which gained 11 basis points over the last year.

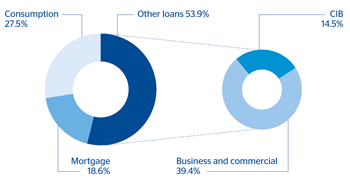

South America. Performing loans breakdown(September 2013) |

South America. Deposits from customers breakdown(September 2013) |

|---|---|

|

|