7. Risk management

7.1 General risk management and control model

The BBVA Group has an overall control and risk management model (hereinafter 'the model') tailored to their business, their organization and the geographies in which it operates, allowing them to develop their activity in accordance with their strategy and policy control and risk management defined by the governing bodies of the Bank and adapt to a changing economic and regulatory environment, tackling risk management globally and adapted to the circumstances of each instance. The model establishes a system of appropriate risk management regarding risk profile and strategy of the Group.

This model is applied comprehensively in the Group and consists of the basic elements listed below:

- Governance and organization.

- Risk appetite.

- Decisions and processes.

- Assessment, monitoring and reporting.

- Infrastructure.

The Group encourages the development of a risk culture to ensure consistent application of the control and risk management Modell in the Group, and to ensure that the risk function is understood and assimilated at all levels of the organization.

7.1.1 Governance and organization

The governance model for risk management at BBVA is characterized by a special involvement of its corporate bodies, both in setting the risk strategy and in the ongoing monitoring and supervision of its implementation.

Thus, as developed below, the corporate bodies are the ones that approve this risk strategy and corporate policies for the different types of risk, being the risk function responsible for the management, its implementation and development, reporting to the governing bodies.

The responsibility for the daily management of the risks lies on the businesses which abide in the development of their activity to the policies, standards, procedures, infrastructure and controls, based on the framework set by the governing bodies, which are defined by the function risk.

To perform this task properly, the risk function in the BBVA Group is configured as a single, comprehensive and independent role of commercial areas.

Corporate governance system

BBVA Group has developed a corporate governance system that is in line with the best international practices and adapted to the requirements of the regulators in the countries in which its different business units operate.

The Board of Directors (hereinafter also referred to as "the Board") approves the risk strategy and supervises the internal control and management systems. Specifically, the strategy approved by the Board includes, at least, the Group's Risk Appetite statement, the fundamental metrics and the basic structure of limits by geographies, types of risk and asset classes, as well as the bases of the control and risk management model. The Board ensures that the budget is in line with the approved risk appetite.

On the basis established by the Board of Directors, the Executive Committee approves specific corporate policies for each type of risk. Furthermore, the committee approves the Group's risk limits and monitors them, being informed of both limits excess occurrences and, where applicable, the appropriate corrective measures taken.

Lastly, the Board of Directors has set up a Board committee specializing in risks, the Risk Committee. This committee is responsible for analyzing and regularly monitoring risks within the remit of the corporate bodies and assists the Board and the SC in determining and monitoring the risk strategy and the corporate policies, respectively. Another task of special relevance it carries out is detailed control and monitoring of the risks that affect the Group as a whole, which enables it to supervise the effective integration of the risk strategy management and the application of corporate policies approved by the corporate bodies.

The head of the risk function in the executive hierarchy is the Group’s Chief Risk Officer (“CRO”), who carries out its functions with independence, authority, capacity and resources to do so. He is appointed by the Board of Directors of the Bank as a member of its Senior Management, and has direct access to its corporate bodies (Board of Directors, Executive Standing Committee and Risk Committee), who reports regularly on the status of risks to the Group.

The Chief Risk Officer, for the utmost performance of its functions, is supported by a cross composed set of units in corporate risk and the specific risk units in the geographical and / or business areas of the Group structure. Each of these units is headed by a Risk Officer for the geographical and/or business area who, within his/her field of competence, carries out risk management and control functions and is responsible for applying the corporate policies and rules approved at Group level in a consistent manner, adapting them if necessary to local requirements and reporting to the local corporate bodies.

The Risk Officers of the geographical and/or business areas report both to the Group's Chief Risk Officer and to the head of their geographical and/or business area. This dual reporting system aims to ensure that the local risk management function is independent from the operating functions and that it is aligned with the Group's corporate risk policies and goals.

Organizational structure and committees

The risk management function, as defined above, consists of risk units from the corporate area, which carry out cross-cutting functions, and risk units from the geographical and/or business areas.

- The corporate area's risk units develop and present the Group's risk appetite proposal, corporate policies, rules and global procedures and infrastructures to the CRO, within the action framework approved by the corporate bodies, ensure their application, and report either directly or through the CRO to the Bank's corporate bodies.

Their functions include:

- Management of the different types of risks at Group level in accordance with the strategy defined by the corporate bodies.

- Risk planning aligned with the risk appetite principles defined by the Group.

- Monitoring and control of the Group's risk profile in relation to the risk appetite approved by the Bank's corporate bodies, providing accurate and reliable information with the required frequency and in the necessary format.

- Prospective analyses to enable an evaluation of compliance with the risk appetite in stress scenarios and the analysis of risk mitigation mechanisms.

- Management of the technological and methodological developments required for implementing the Model in the Group.

- Design of the Group's Internal Risk Control model and definition of the methodology, corporate criteria and procedures for identifying and prioritizing the risk inherent in each unit's activities and processes.

- Validation of the models used and the results obtained by them in order to verify their adaptation to the different uses to which they are applied.

- The risk units in the business units develop and present to the Risk Officer of the geographical and/or business area the risk appetite proposal applicable in each geographical and/or business area, independently and always within the Group's risk appetite. They also ensure that the corporate policies and rules approved consistently at a Group level are applied, adapting them if necessary to local requirements; they are provided with appropriate infrastructures for managing and controlling their risks; and they report to their corporate bodies and/or to senior management, as appropriate.

The local risk units thus work with the corporate area risk units in order to adapt to the risk strategy at Group level and share all the information necessary for monitoring the development of their risks.

The risk function has a decision-making process to perform its functions, underpinned by a structure of committees, where the Global Risk Management Committee (GRMC) acts as the highest committee within Risk. It proposes, examines and, where applicable, approves, among others, the internal risk regulatory framework and the procedures and infrastructures needed to identify, assess, measure and manage the material risks faced by the Group in its businesses. The members of this Committee are the Group's CRO and the heads of the risk units of the corporate area and of the most representative geographical and/or business areas.

The GRMC carries out its functions assisted by various support committees which include:

- Global Technical Operations Committee: It is responsible for decision-making related to wholesale credit risk admission in certain customer segments.

- Monitoring, Assessment & Reporting Committee: It guarantees and ensures the appropriate development of aspects related to risk identification, assessment, monitoring and reporting, with an integrated and cross-cutting vision.

- Asset Allocation Committee: The executive body responsible for analysis and decision-making on all credit risk matters related to the processes intended for obtaining a balance between risk and return in accordance with the Group's risk appetite.

- Technology and Methodologies Committee: It determines the need for new models and infrastructures and channels the decision-making related to the tools needed for managing all the risks to which the Group is exposed.

- Corporate Technological Risks and Operational Control Committee: It approves the Technological Risks and Operational Control Management Frameworks in accordance with the General Risk Management Model's architecture and monitors metrics, risk profiles and operational loss events.

- Global Market Risk Unit Committee: It is responsible for formalizing, supervising and communicating the monitoring of trading desk risk in all the Global Markets business units.

- Corporate Operational and Outsourcing Risk Admission Committee: It identifies and assesses the operational risks of new businesses, new products and services, and outsourcing initiatives.

Each geographical and/or business area has its own risk management committee (or committees), with objectives and contents similar to those of the corporate area, which perform their duties consistently and in line with corporate risk policies and rules.

Under this organizational scheme, the risk management function ensures the risk strategy, the regulatory framework, and standardized risk infrastructures and controls are integrated and applied across the entire Group. It also benefits from the knowledge and proximity to customers in each geographical and/or business area, and transmits the corporate risk culture to the Group's different levels.

Internal Risk Control and Internal Validation

The Group has a specific Internal Risk Control unit whose main function is to ensure there is an adequate internal regulatory framework in place, together with a process and measures defined for each type of risk identified in the Group, (and for other types of risk that could potentially affect the Group, to oversee their application and operation, and to ensure that the risk strategy is integrated into the Group's management. The Internal Risk Control unit is independent from the units that develop risk models, manage running processes and controls. Its scope is global both geographically and in terms of type of risk.

The Director of Group Internal Control Risk is responsible for the function, and reports its activities and work plans to the CRO and the Risk Committee of the Board, besides attending to it on issues deemed necessary.

For this purpose, the Risk area also has a Technical area independent from the units that develop risk models, manage running processes and controls, which gives the Risk Committee of the Board the necessary technical support to better perform their functions.

The unit has a structure of teams at both corporate level and in the most relevant geographical areas in which the Group operates. As in the case of the corporate area, local units are independent of the business areas that execute the processes, and of the units that execute the controls. They report functionally to the Internal Risk Control unit. This unit's lines of action are established at Group level, and it is responsible for adapting and executing them locally, as well as for reporting the most relevant aspects.

Additionally, the Group has an Internal Validation unit, also independent rom the units that develop risk models and of those who use them to manage. Its functions include, among others, review and independent validation, internally, of the models used for the control and management of the Group's risks.

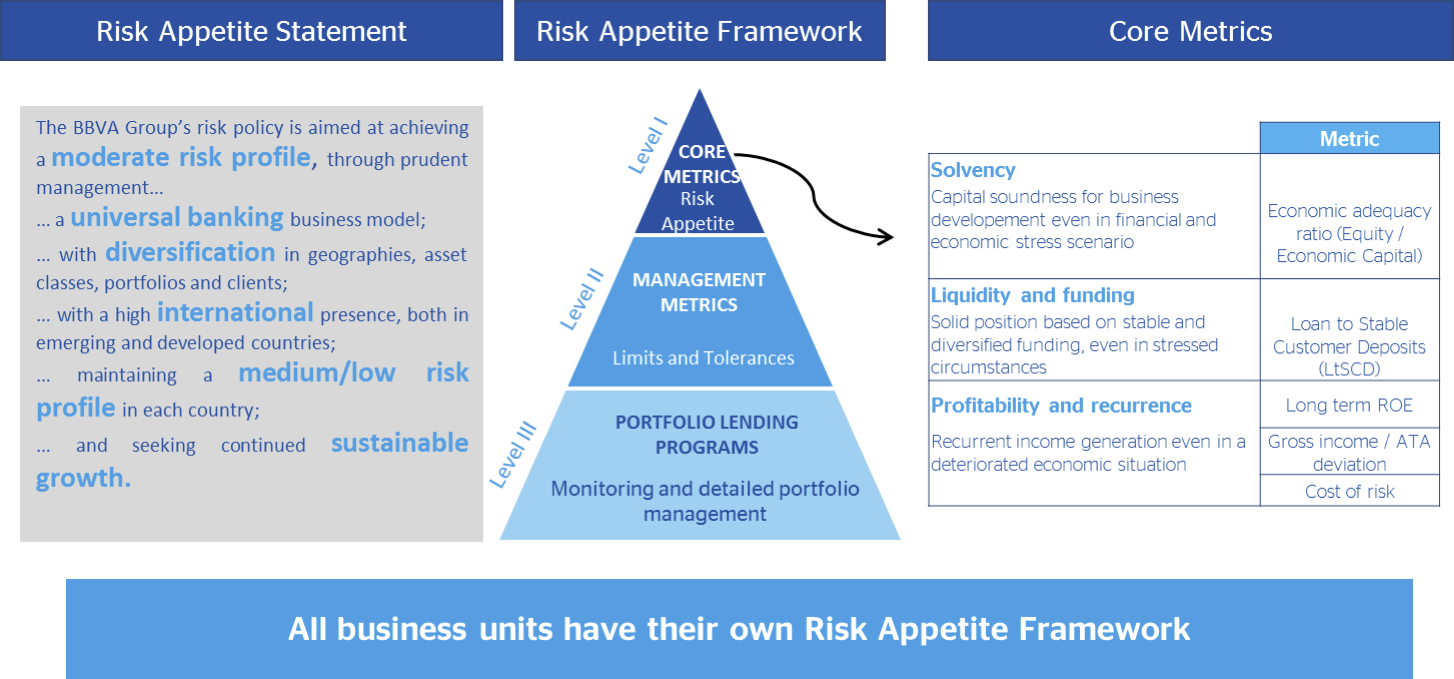

7.1.2 Risk appetite

The Group's risk appetite, approved by the Board of Directors, determines the risks (and their level) that the Group is willing to assume to achieve its business targets. These are expressed in terms of capital, financial structure, profitability, recurrent earnings, cost of risk or other metrics. The definition of the risk appetite has the following goals:

- To express the Group's strategy and the maximum levels of risk it is willing to assume, at both Group and geographical and/or business area level.

- To establish a set of guidelines for action and a management framework for the medium and long term that prevent actions from being taken (at both Group and geographical and/or business area level) which could compromise the future viability of the Group.

- To establish a framework for relations with the geographical and/or business areas that, while preserving their decision-making autonomy, ensures they act consistently, avoiding uneven behavior.

- To establish a common language throughout the organization and develop a compliance-oriented risk culture.

- Alignment with the new regulatory requirements, facilitating communication with regulators, investors and other stakeholders, thanks to an integrated and stable risk management framework.

Risk appetite is expressed through the following elements:

- Risk appetite statement: sets out the general principles of the Group's risk strategy and the target risk profile.

- BBVA's risk policy aims to maintain the risk profile set out in the Group's risk appetite statement, which is reflected in a series of metrics (fundamental metrics and limits).

- Fundamental metrics: they reflect, in quantitative terms, the principles and the target risk profile set out in the risk appetite statement.

- Limits: they establish the risk appetite at geographical and/or business area, legal entity and risk type level, or any other level deemed appropriate, enabling its integration into management.

The corporate risk area works with the various geographical and/or business areas to define their risk appetite, which will be coordinated with and integrated into the Group's risk appetite to ensure that its profile fits as defined.

The BBVA Group assumes a certain degree of risk to be able to provide financial services and products to its customers and obtain attractive returns for its shareholders. The organization must understand, manage and control the risks it assumes.

The aim of the organization is not to eliminate all risks faced, but to assume a prudent level of risks that allows it to generate returns while maintaining acceptable capital and fund levels and generating recurrent earnings.

The risk appetite defined by the Group expresses the levels and types of risk that the Bank is willing to assume to be able to implement its strategic plan with no relevant deviations, even in situations of stress. The risk appetite is integrated in the management and determines the basic lines of activity of the Group, because it sets the framework within the budget is developed.

Fundamental metrics

Those metrics that characterize the Group's objective behavior (as defined in the statement), enabling the expression of the risk culture at all levels in a structured and understandable manner. They summarize the Group's goals, and are therefore useful for communication to the stakeholders.

The fundamental metrics are strategic in nature. They are disseminated throughout the Group, understandable and easy to calculate, and objectifiable at business and/or geographical area level, so they can be subject to future projections.

Limits

Limits are metrics that determine the Group’s strategic positioning for the different types of risk: credit, ALM (Asset Liability Management), liquidity, markets, operational. They differ from the fundamental metrics in the following respects:

- They are levers, not the result. They are a management tool related to a strategic positioning that must be geared toward ensuring compliance with the fundamental metrics, even in an adverse scenario.

- Risk metrics: a higher level of specialization, they do not necessarily have to be disseminated across the Group.

- Independent of the cycle: they can include metrics with little correlation with the economic cycle, thus allowing comparability that is isolated from the specific macroeconomic situation.

Thus, they are levers for remaining within the thresholds defined in the fundamental metrics and are used for day-to-day risk management. They include tolerance limits, sub-limits and alerts established at the level of business and/or geographical areas, portfolios and products. During 2015, the Risk Appetite metrics evolved in line with the set profile.

7.1.3 Decisions and processes

The transfer of risk appetite to ordinary management is supported by three basic aspects:

- A standardized set of regulations

- Risk planning

- Integrated management of risks over their life cycle

Standardized regulatory framework

The corporate GRM area is responsible for proposing the definition and development of the corporate policies, specific rules, procedures and schemes of delegation based on which risk decisions should be taken within the Group.

This process aims for the following objectives:

- Hierarchy and structure: well-structured information through a clear and simple hierarchy creating relations between documents that depend on each other.

- Simplicity: an appropriate and sufficient number of documents.

- Standardization: a standardized name and content of document.

- Accessibility: ability to search for, and easy access to, documentation through the corporate risk management library.

The approval of corporate policies for all types of risks corresponds to the corporate bodies of the Bank, while the corporate risk area endorses the remaining regulations.

Risk units of geographical and / or business areas continue to adapt to local requirements the regulatory framework for the purpose of having a decision process that is appropriate at local level and aligned with the Group policies. If such adaptation is necessary, the local risk area must inform the corporate GRM area, which must ensure the consistency of the set of regulations at the level of the entire Group, and thus must give its approval prior to any modifications proposed by the local risk areas.

Risk planning

Risk planning ensures that the risk appetite is integrated into management, through a cascade process for establishing limits, in which the function of the corporate area risk units and the geographical and/or business areas is to guarantee the alignment of this process against the Group's risk appetite.

It has tools in place that allow the risk appetite defined at aggregate level to be assigned and monitored by business areas, legal entities, types of risk, concentrations and any other level considered necessary.

The risk planning process is present within the rest of the Group's planning framework so as to ensure consistency among all of them.

Daily risk management

All risks must be managed integrally during their life cycle, and be treated differently depending on the type.

The risk management cycle is composed of 5 elements:

- Planning: with the aim of ensuring that the Group's activities are consistent with the target risk profile and guaranteeing solvency in the development of the strategy.

- Assessment: a process focused on identifying all the risks inherent to the activities carried out by the Group.

- Formalization: includes the risk origination, approval and formalization stages.

- Monitoring and reporting: continuous and structured monitoring of risks and preparation of reports for internal and/or external (market, investors, etc.) consumption.

- Active portfolio management: focused on identifying business opportunities in existing portfolios and new markets, businesses and products.

7.1.4 Assessment, monitoring and reporting

Assessment, monitoring and reporting is a cross-cutting element that should ensure that the Model has a dynamic and proactive vision to enable compliance with the risk appetite approved by the corporate bodies, even in adverse scenarios. The materialization of this process covers all the categories of material risks and has the following objectives:

- Assess compliance with the risk appetite at the present time, through monitoring of the fundamental management metrics and limits.

- Assess compliance with the risk appetite in the future, through the projection of the risk appetite variables, in both a baseline scenario determined by the budget and a risk scenario determined by the stress tests.

- Identify and assess the risk factors and scenarios that could compromise compliance with the risk appetite, through the development of a risk repository and an analysis of the impact of those risks.

- Act to mitigate the impact in the Group of the identified risk factors and scenarios, ensuring this impact remains within the target risk profile.

- Supervise the key variables that are not a direct part of the risk appetite, but that condition its compliance. These can be either external or internal.

The following phases need to be developed for undertaking this process:

- Identification of risk factors, aimed at generating a map with the most relevant risk factors that can compromise the Group's performance in relation to the thresholds defined in the risk appetite.

- Impact evaluation. This involves evaluating the impact that the materialization of one (or more) of the risk factors identified in the previous phase could have on the risk appetite metrics, through the occurrence of a given scenario.

- Response to undesired situations and realignment measures. Exceeding the parameters will trigger an analysis of the realignment measures to enable dynamic management of the situation, even before it occurs.

- Monitoring. The aim is to avoid losses before they occur by monitoring the Group's current risk profile and the identified risk factors.

- Reporting. This aims to provide information on the assumed risk profile by offering accurate, complete and reliable data to the corporate bodies and to senior management, with the frequency and completeness appropriate to the nature, significance and complexity of the risks.

7.1.5 Infrastructure

The infrastructure is an element that must ensure that the Group has the human and technological resources needed for effective management and supervision of risks in order to carry out the functions set out in the Group's risk Model and the achievement of their objectives.

With respect to human resources, the Group's risk function will have an adequate workforce, in terms of number, skills and experience.

With regards to technology, the Group ensures the integrity of management information systems and the provision of the infrastructure needed for supporting risk management, including tools appropriate to the needs arising from the different types of risks for their admission, management, assessment and monitoring.

The principles that govern the Group risk technology are:

- Standardization: the criteria are consistent across the Group, thus ensuring that risk handling is standardized at geographical and/or business area level.

- Integration in management: the tools incorporate the corporate risk policies and are applied in the Group's day-to-day management.

- Automation of the main processes making up the risk management cycle.

- Appropriateness: provision of adequate information at the right time.

Through the “Risk Analytics” function, the Group has a corporate framework in place for developing the measurement techniques and models. It covers all the types of risks and the different purposes and uses a standard language for all the activities and geographical/business areas and decentralized execution to make the most of the Group's global reach. The aim is to continually evolve the existing risk models and generate others that cover the new areas of the businesses that develop them, so as to reinforce the anticipation and proactiveness that characterize the Group's risk function.

Also the risk units of geographical and / or business areas shall ensure that they have sufficient means from the point of view of resources, structures and tools to develop a risk management in line with the corporate model.

7.1.6 Risk culture

BBVA considers risk culture to be an essential element for consolidating and integrating the other components of the Model. The culture transfers the implications that are involved in the Group's activities and businesses to all the levels of the organization. The risk culture is organized through a number of levers, including the following:

- Communication: promotes the dissemination of the Model, and in particular the principles that must govern risk management in the Group, in a consistent and integrated manner across the organization, through the most appropriate channels.

GRM has a number of communication channels to facilitate the transmission of information and knowledge among the various teams in the function and the Group, adapting the frequency, formats and recipients based on the proposed goal, in order to strengthen the basic principles of the risk function. The risk culture and the management model thus emanate from the Group's corporate bodies and senior management and are transmitted throughout the organization.

- Training: its main aim is to disseminate and establish the model of risk management across the organization, ensuring standards in the skills and knowledge of the different persons involved in the risk management processes.

Well defined and implemented training ensures continuous improvement of the skills and knowledge of the Group's professionals, and in particular of the GRM area, and is based on four aspects that aim to develop each of the needs of the GRM group by increasing its knowledge and skills in different fields such as: finance and risks, tools and technology, management and skills, and languages.

- Motivation: the aim in this area is for the incentives of the risk function teams to support the strategy for managing those teams and the function's values and culture at all levels. Includes compensation and all those elements related to motivation – working environment, etc. which contribute to the achievement Model objectives.

7.2 Risk events

As mentioned earlier, BBVA has processes in place for identifying risks and analyzing scenarios that enable the Group to manage risks in a dynamic and proactive way.

The risk identification processes are forward looking to ensure the identification of emerging risks and take into account the concerns of both the business areas, which are close to the reality of the different geographical areas, and the corporate areas and senior management.

Risks are captured and measured consistently using the methodologies deemed appropriate in each case. Their measurement includes the design and application of scenario analyses and stress testing and considers the controls to which the risks are subjected.

As part of this process, a forward projection of the risk appetite variables in stress scenarios is conducted in order to identify possible deviations from the established thresholds. If any such deviations are detected, appropriate measures are taken to keep the variables within the target risk profile.

To this extent, there are a number of emerging risks that could affect the Group’s business trends. These risks are described in the following main blocks:

- Macroeconomic and geopolitical risks

- The increased economic slowdown in China's economy and its impact on other emerging economies through energy prices and raw materials, along with possible difficulties in the European economic recovery meant key points for the Group.

- In addition, financial institutions are exposed to the risks of political and social instability in the countries in which they operate, which can have significant effects on their economies and even regionally.

In this regard the Group's geographical diversification is a key to achieving a high level of recurring revenues, despite environmental conditions and economic cycles of the economies in which it operates.

- Regulatory, legal, tax and reputational risks

- Financial institutions are exposed to a complex and ever-changing regulatory and legal environment defined by governments and regulators. This can affect their ability to grow and the capacity of certain businesses to develop, and result in stricter liquidity and capital requirements with lower profitability ratios. The Group constantly monitors changes in the regulatory framework that allow for anticipation and adaptation to them in a timely manner, adopt best practices and more efficient and rigorous criteria in its implementation.

- The financial sector is under ever closer scrutiny by regulators, governments and society itself. Negative news or inappropriate behavior can significantly damage the Group's reputation and affect its ability to develop a sustainable business. The attitudes and behaviors of the group and its members are governed by the principles of integrity, honesty, long-term vision and best practices through, inter alia, internal control Model, the Code of Conduct, tax strategy and Responsible Business Strategy of the Group.

- The financial sector is exposed to increasing litigation, so the financial institutions are having to face a large number of proceedings whose economic consequences are difficult to determine. The Group manages and monitors these proceedings to defend its interests, where necessary allocating the corresponding provisions to cover them, following the expert criteria of internal lawyers and external attorneys responsible for the legal handling of the procedures, in accordance with applicable legislation.

- Business and operational risks

- New technologies and forms of customer relationships: Developments in the digital world and in information technologies pose significant challenges for financial institutions, entailing threats (new competitors, disintermediation…) but also opportunities (new framework of relations with customers, greater ability to adapt to their needs, new products and distribution channels...). Digital transformation is a priority for the Group as it aims to lead digital banking of the future as one of its objectives.

- Technological risks and security breaches: The Group is exposed to new threats such as cyber-attacks, theft of internal and customer databases, fraud in payment systems, etc. that require major investments in security from both the technological and human point of view. The Group gives great importance to the active operational and technological risk management and control. One example was the early adoption of advanced models for management of these risks (AMA - Advanced Measurement Approach).

7.3 Credit risk

Credit risk arises from the probability that one party to a financial instrument will fail to meet its contractual obligations for reasons of insolvency or inability to pay and cause a financial loss for the other party.

It is the most important risk for the Group and includes counterparty risk, issuer risk, settlement risk and country risk management.

The principles underpinning credit risk management in BBVA are as follows:

- Availability of basic information for the study and proposal of risk, and supporting documentation for approval, which sets out the conditions required by the internal relevant body.

- Sufficient generation of funds and asset solvency of the customer to assume principal and interest repayments of loans owed.

- Establishment of adequate and sufficient guarantees that allow effective recovery of the operation, this being considered a secondary and exceptional method of recovery when the first has failed.

Credit risk management in the Group has an integrated structure for all its functions, allowing decisions to be taken objectively and independently throughout the life cycle of the risk.

- At Group level: frameworks for action and standard rules of conduct are defined for handling risk, specifically, the circuits, procedures, structure and supervision.

- At the business area level: they are responsible for adapting the Group's criteria to the local realities of each geographical area and for direct management of risk according to the decision-making circuit:

- Retail risks: in general, the decisions are formalized according to the scoring tools, within the general framework for action of each business area with regard to risks. The changes in weighting and variables of these tools must be validated by the corporate GRM area.

- Wholesale risks: in general, the decisions are formalized by each business area within its general framework for action with regard to risks, which incorporates the delegation rule and the Group's corporate policies.

7.3.1 Credit risk exposure

In accordance with IFRS 7, “Financial Instruments: Disclosures” the BBVA Group’s maximum credit risk exposure (see definition below) by headings in the balance sheets as of December 31, 2015, 2014 and 2013 is provided below. It does not consider the availability of collateral or other credit enhancements to guarantee compliance with payment obligations. The details are broken down by financial instruments and counterparties.

Download Excel

Download Excel

| Maximum Credit Risk Exposure | Millions of euros | |||

|---|---|---|---|---|

| Notes | 2015 | 2014 | 2013 | |

| Financial assets held for trading |

|

37,424 | 39,028 | 34,473 |

| Debt securities | 10 | 32,826 | 33,883 | 29,601 |

| Government |

|

29,454 | 28,212 | 24,696 |

| Credit institutions |

|

1,766 | 3,048 | 2,734 |

| Other sectors |

|

1,606 | 2,623 | 2,172 |

| Equity instruments |

|

4,534 | 5,017 | 4,766 |

| Customer lending |

|

65 | 128 | 107 |

| Other financial assets designated at fair value through profit or loss |

|

2,311 | 2,761 | 2,413 |

| Loans and advances to credit institutions |

|

62 | - | - |

| Debt securities | 11 | 173 | 737 | 663 |

| Government |

|

132 | 141 | 142 |

| Credit institutions |

|

29 | 16 | 16 |

| Other sectors |

|

11 | 580 | 506 |

| Equity instruments |

|

2,075 | 2,024 | 1,750 |

| Available-for-sale financial assets |

|

113,710 | 95,049 | 77,972 |

| Debt securities | 12 | 108,448 | 87,679 | 71,861 |

| Government |

|

81,579 | 63,764 | 48,728 |

| Credit institutions |

|

8,069 | 7,377 | 10,431 |

| Other sectors |

|

18,800 | 16,538 | 12,702 |

| Equity instruments |

|

5,262 | 7,370 | 6,111 |

| Loans and receivables |

|

476,396 | 386,653 | 365,941 |

| Loans and advances to credit institutions | 13.1 | 33,014 | 27,089 | 22,902 |

| Loans and advances to customers | 13.2 | 432,856 | 352,900 | 338,558 |

| Government |

|

38,611 | 37,113 | 32,601 |

| Agriculture |

|

4,315 | 4,348 | 5,008 |

| Industry |

|

56,913 | 37,580 | 28,829 |

| Real estate and construction |

|

38,964 | 33,152 | 40,699 |

| Trade and finance |

|

43,576 | 43,880 | 47,417 |

| Loans to individuals |

|

194,288 | 158,586 | 150,678 |

| Other |

|

56,188 | 38,242 | 33,325 |

| Debt securities | 13.3 | 10,526 | 6,663 | 4,481 |

| Government |

|

3,275 | 5,608 | 3,175 |

| Credit institutions |

|

125 | 81 | 297 |

| Other sectors |

|

7,126 | 975 | 1,009 |

| Derivatives (trading and hedging) |

|

49,350 | 47,248 | 41,294 |

| Total Financial Assets Risk |

|

679,193 | 570,739 | 522,093 |

| Financial guarantees (Bank guarantees, letter of credits,..) |

|

49,876 | 33,741 | 33,543 |

| Drawable by third parties |

|

123,620 | 96,714 | 87,542 |

| Government |

|

2,570 | 1,359 | 4,354 |

| Credit institutions |

|

921 | 1,057 | 1,583 |

| Other sectors |

|

120,129 | 94,299 | 81,605 |

| Other contingent commitments |

|

12,113 | 9,537 | 6,628 |

| Total Contingent Risks and Commitments | 32 | 185,609 | 139,993 | 127,712 |

| Total Maximum Credit Exposure |

|

864,802 | 710,732 | 649,805 |

The maximum credit exposure presented in the table above is determined by type of financial asset as explained below:

- In the case of financial assets recognized in the consolidated balance sheets, exposure to credit risk is considered equal to its carrying amount (not including impairment losses), with the sole exception of trading and hedging derivatives.

- The maximum credit risk exposure on financial guarantees granted is the maximum that the Group would be liable for if these guarantees were called in, and that is their carrying amount.

- Our calculation of risk exposure for derivatives is based on the sum of two factors: the derivatives fair value and their potential risk (or "add-on").

- The first factor, market value, reflects the difference between original commitments and market values on the reporting date (mark-to-market). As indicated in Note 2.2.1, derivatives are accounted for as of each reporting date at fair value in accordance with IAS 39.

- The second factor, potential risk (‘add-on’), is an estimate of the maximum increase to be expected on risk exposure over a derivative market value (at a given statistical confidence level) as a result of future changes in the fair value over the remaining term of the derivatives.

The consideration of the potential risk ("add-on") relates the risk exposure to the exposure level at the time of a customer’s default. The exposure level will depend on the customer’s credit quality and the type of transaction with such customer. Given the fact that default is an uncertain event which might occur any time during the life of a contract, the BBVA Group has to consider not only the credit exposure of the derivatives on the reporting date, but also the potential changes in exposure during the life of the contract. This is especially important for derivatives, whose valuation changes substantially throughout their terms, depending on the fluctuation of market prices.

7.3.2 Mitigation of credit risk, collateralized credit risk and other credit enhancements

In most cases, maximum credit risk exposure is reduced by collateral, credit enhancements and other actions which mitigate the Group’s exposure. The BBVA Group applies a credit risk hedging and mitigation policy deriving from a banking approach focused on relationship banking. The existence of guarantees could be a necessary but not sufficient instrument for accepting risks, as the assumption of risks by the Group requires prior evaluation of the debtor’s capacity for repayment, or that the debtor can generate sufficient resources to allow the amortization of the risk incurred under the agreed terms.

The policy of accepting risks is therefore organized into three different levels in the BBVA Group:

- Analysis of the financial risk of the operation, based on the debtor’s capacity for repayment or generation of funds;

- The constitution of guarantees that are adequate, or at any rate generally accepted, for the risk assumed, in any of the generally accepted forms: monetary, secured, personal or hedge guarantees; and finally,

- Assessment of the repayment risk (asset liquidity) of the guarantees received.

The procedures for the management and valuation of collaterals are set out in the Corporate Policies (retail and wholesale), which establish the basic principles for credit risk management, including the management of collaterals assigned in transactions with customers.

The methods used to value the collateral are in line with the best market practices and imply the use of appraisal of real-estate collateral, the market price in market securities, the trading price of shares in mutual funds, etc. All the collaterals assigned must be properly drawn up and entered in the corresponding register. They must also have the approval of the Group’s legal units.

The following is a description of the main types of collateral for each financial instrument class:

- Financial instruments held for trading: The guarantees or credit enhancements obtained directly from the issuer or counterparty are implicit in the clauses of the instrument.

- Trading and hedging derivatives: In derivatives, credit risk is minimized through contractual netting agreements, where positive- and negative-value derivatives with the same counterparty are offset for their net balance. There may likewise be other kinds of guarantees, depending on counterparty solvency and the nature of the transaction.

- Other financial assets designated at fair value through profit or loss and Available-for-sale financial assets: The guarantees or credit enhancements obtained directly from the issuer or counterparty are inherent to the structure of the instrument.

- Loans and receivables:

- Loans and advances to credit institutions: These usually only have the counterparty’s personal guarantee.

- Loans and advances to customers: Most of these loans and advances are backed by personal guarantees extended by the own customer. There may also be collateral to secure loans and advances to customers (such as mortgages, cash collaterals, pledged securities and other collateral), or to obtain other credit enhancements (bonds, hedging, etc.).

- Debt securities: The guarantees or credit enhancements obtained directly from the issuer or counterparty are inherent to the structure of the instrument.

Collateralized loans granted by the Group as of December 31, 2015, 2014 and 2013 excluding balances deemed impaired, is broken down in the table below:

Download Excel

| Collateralized Credit Risk |

|

Millions of euros | ||

|---|---|---|---|---|

| Notes | 2015 | 2014 | 2013 | |

| Mortgage loans | 13.2 | 144,203 | 124,097 | 125,564 |

| Operating assets mortgage loans |

|

6,813 | 4,062 | 3,778 |

| Home mortgages |

|

120,164 | 109,031 | 108,745 |

| Rest of mortgages |

|

17,226 | 11,005 | 13,041 |

| Secured loans, except mortgage | 13.2 | 57,041 | 28,419 | 23,660 |

| Cash guarantees |

|

479 | 468 | 300 |

| Secured loan (pledged securities) |

|

734 | 518 | 570 |

| Rest of secured loans (*) |

|

55,828 | 27,433 | 22,790 |

| Total |

|

201,244 | 152,517 | 149,224 |

- Financial guarantees, other contingent risks and drawable by third parties: These have the counterparty’s personal guarantee.

7.3.3 Financial instrument netting

Financial assets and liabilities may be netted, i.e. they are presented for a net amount on the consolidated balance sheet only when the Group's entities satisfy with the provisions of IAS 32-Paragraph 42, so they have both the legal right to net recognized amounts, and the intention of settling the net amount or of realizing the asset and simultaneously paying the liability.

In addition, the Group has presented as gross amounts assets and liabilities on the consolidated balance sheet for which there are master netting arrangements in place, but for which there is no intention of settling net. The most common types of events that trigger the netting of reciprocal obligations are bankruptcy of the entity, surpassing certain level of indebtedness threshold, failure to pay, restructuring and dissolution of the entity.

In the current market context, derivatives are contracted under different framework contracts being the most widespread developed by the International Swaps and Derivatives Association (“ISDA”) and, for the Spanish market, the Framework Agreement on Financial Transactions (“CMOF”). Almost all portfolio derivative transactions have been concluded under these framework contracts, including in them the netting clauses mentioned in the preceding paragraph as "Master Netting Agreement", greatly reducing the credit exposure on these instruments. Additionally, in contracts signed with professional counterparts, the collateral agreement annexes called Credit Support Annex (“CSA”) are included, thereby minimizing exposure to a potential default of the counterparty.

Moreover, in transactions involving assets purchased or sold under a purchase agreement there has greatly increased the volume transacted through clearing houses that articulate mechanisms to reduce counterparty risk, as well as through the signature of various master agreements for bilateral transactions, the most widely used being the Global Master Repurchase Agreement (GMRA), published by International Capital Market Association (“ICMA”), to which the clauses related to the collateral exchange are usually added within the text of the master agreement itself.

A summary of the effect of the compensation (via netting and collateral) for derivatives and securities operations is presented below as of December 31, 2015:

Download Excel

|

|

Millions of euros | ||||||

|---|---|---|---|---|---|---|---|

|

|

|

|

|

Gross Amounts Not Offset in the Condensed Consolidated Balance Sheets (D) |

|

||

| December 2015 | Notes | Gross Amounts Recognized (A) | Gross Amounts Offset in the Condensed Consolidated Balance Sheets (B) | Net Amount Presented in the Condensed Consolidated Balance Sheets (C=A-B) | Financial Instruments | Cash Collateral Received/ Pledged | Net Amount (E=C-D) |

| Derivative financial assets | 10, 14 | 52,244 | 7,805 | 44,439 | 30,350 | 5,493 | 8,597 |

| Reverse repurchase, securities borrowing and similar agreements | 34 | 21,531 | 4,596 | 16,935 | 17,313 | 24 | (402) |

| Total Assets |

|

73,775 | 12,401 | 61,374 | 47,663 | 5,517 | 8,195 |

|

|

|

|

|

|

|

|

|

| Derivative financial liabilities | 10, 14 | 53,298 | 8,423 | 44,876 | 30,350 | 9,830 | 4,696 |

| Repurchase, securities lending and similar agreements | 34 | 72,998 | 4,596 | 68,402 | 68,783 | 114 | (495) |

| Total Liabillities |

|

126,296 | 13,019 | 113,278 | 99,133 | 9,944 | 4,201 |

7.3.4 Risk concentration

Policies for preventing excessive risk concentration

In order to prevent the build-up of excessive concentrations of credit risk at the individual, country and sector levels, BBVA Group maintains maximum permitted risk concentration indices updated at individual and portfolio sector levels tied to the various observable variables within the field of credit risk management. The limit on the Group’s exposure or financial commitment to a specific customer therefore depends on the customer’s credit rating, the nature of the risks involved, and the Group’s presence in a given market, based on the following guidelines:

- The aim is, as much as possible, to reconcile the customer's credit needs (commercial/financial, short-term/long-term, etc.) with the interests of the Group.

- Any legal limits that may exist concerning risk concentration are taken into account (relationship between risks with a customer and the capital of the entity that assumes them), the markets, the macroeconomic situation, etc.

Risk concentrations by geography

Below is a breakdown of the balances of financial instruments registered in the accompanying consolidated balance sheets by their concentration in geographical areas and according to the residence of the customer or counterparty. It does not take into account valuation adjustments, impairment losses or loan-loss provisions:

Download Excel

| Risks by Geographical Areas December 2015 |

Millions of euros | |||||||

|---|---|---|---|---|---|---|---|---|

| Spain | Europe, Excluding Spain | Mexico | USA | Turkey | South America | Rest | Total | |

| Financial assets - |

|

|

|

|

|

|

|

|

| Financial assets held for trading | 17,726 | 30,701 | 16,866 | 7,095 | 220 | 3,977 | 1,743 | 78,327 |

| Loans and advances to customers | - | - | - | 65 | - | - | - | 65 |

| Debt securities | 8,037 | 5,491 | 13,032 | 4,072 | 48 | 1,975 | 169 | 32,825 |

| Equity instruments (*) | 2,038 | 1,546 | 411 | 231 | 32 | 137 | 139 | 4,534 |

| Derivatives | 7,651 | 23,663 | 3,422 | 2,727 | 140 | 1,865 | 1,434 | 40,902 |

| Other financial assets designated at fair value through profit or loss | 243 | 168 | 1,885 | 3 | 9 | 2 | - | 2,311 |

| Loans and advances to credit institutions | 53 | - | - | - | 9 | - | - | 62 |

| Debt securities | 106 | 55 | 9 | 3 | - | - | - | 173 |

| Equity instruments (*) | 84 | 113 | 1,876 | - | - | 2 | - | 2,075 |

| Available-for-sale portfolio | 48,506 | 16,572 | 12,580 | 13,517 | 12,824 | 5,593 | 3,323 | 112,914 |

| Debt securities | 45,567 | 15,956 | 12,539 | 13,484 | 12,738 | 5,168 | 2,346 | 107,797 |

| Equity instruments (*) | 2,939 | 425 | 41 | 617 | 33 | 86 | 977 | 5,116 |

| Loans and receivables | 207,135 | 35,655 | 57,281 | 62,664 | 55,652 | 50,286 | 5,620 | 474,293 |

| Loans and advances to credit institutions | 3,732 | 15,114 | 5,108 | 4,065 | 1,930 | 1,950 | 1,047 | 32,947 |

| Loans and advances to customers | 194,536 | 20,500 | 52,173 | 57,553 | 53,461 | 48,032 | 4,553 | 430,808 |

| Debt securities | 8,866 | 40 | - | 1,046 | 261 | 304 | 20 | 10,538 |

| Held-to-maturity investments | - | - | - | - | - | - | - | - |

| Hedging derivatives and macrohedging adjustments | 1,173 | 1,397 | 702 | 61 | 214 | 36 | 1 | 3,583 |

| Total Risk in Financial Assets | 274,783 | 84,492 | 89,313 | 83,340 | 68,918 | 59,894 | 10,686 | 671,427 |

| Contingent risks and liabilities |

|

|

|

|

|

|

|

|

| Contingent risks | 15,500 | 10,544 | 1,270 | 3,995 | 11,193 | 5,517 | 1,856 | 49,876 |

| Contingent liabilities | 34,861 | 23,537 | 22,569 | 33,070 | 14,135 | 6,486 | 1,075 | 135,733 |

| Total Contingent Risk | 50,361 | 34,081 | 23,839 | 37,065 | 25,328 | 12,003 | 2,931 | 185,609 |

| Total Risks in Financial Instruments | 325,145 | 118,573 | 113,152 | 120,405 | 94,246 | 71,897 | 13,617 | 857,036 |

Download Excel

| Risks by Geographical Areas December 2014 |

Millions of euros | ||||||

|---|---|---|---|---|---|---|---|

| Spain | Europe, Excluding Spain | Mexico | USA | South America | Rest | Total | |

| Financial assets - |

|

|

|

|

|

|

|

| Financial assets held for trading | 17,461 | 36,039 | 17,091 | 6,126 | 4,337 | 2,206 | 83,258 |

| Loans and advances to customers | - | - | - | 128 | - | - | 128 |

| Debt securities | 7,816 | 6,512 | 13,747 | 2,654 | 2,656 | 499 | 33,883 |

| Equity instruments (*) | 2,541 | 1,334 | 342 | 457 | 171 | 172 | 5,017 |

| Derivatives | 7,103 | 28,193 | 3,003 | 2,886 | 1,510 | 1,535 | 44,229 |

| Other financial assets designated at fair value through profit or loss |

189 | 152 | 1,836 | 581 | 3 | - | 2,761 |

| Loans and advances to credit institutions | - | - | - | - | - | - | - |

| Debt securities | 94 | 62 | - | 581 | - | - | 737 |

| Equity instruments (*) | 95 | 90 | 1,836 | - | 3 | - | 2,024 |

| Available-for-sale portfolio | 45,465 | 13,673 | 13,169 | 10,780 | 6,079 | 4,958 | 94,125 |

| Debt securities | 42,267 | 13,348 | 13,119 | 10,222 | 5,973 | 1,929 | 86,858 |

| Equity instruments (*) | 3,198 | 326 | 50 | 558 | 106 | 3,029 | 7,267 |

| Loans and receivables | 185,924 | 31,597 | 52,157 | 52,080 | 57,911 | 4,792 | 384,460 |

| Loans and advances to credit institutions | 4,172 | 13,313 | 2,497 | 3,521 | 2,180 | 1,291 | 26,975 |

| Loans and advances to customers | 178,735 | 18,274 | 49,660 | 47,635 | 53,018 | 3,501 | 350,822 |

| Debt securities | 3,017 | 9 | - | 924 | 2,713 | - | 6,663 |

| Held-to-maturity investments | - | - | - | - | - | - | - |

| Hedging derivatives and macrohedging adjustments | 708 | 1,699 | 182 | 66 | 14 | 2 | 2,672 |

| Total Risk in Financial Assets | 249,747 | 83,160 | 84,435 | 69,633 | 68,344 | 11,958 | 567,276 |

| Contingent risks and liabilities |

|

|

|

|

|

|

|

| Contingent risks | 13,500 | 8,454 | 1,220 | 3,161 | 5,756 | 1,650 | 33,741 |

| Contingent liabilities | 25,577 | 22,973 | 19,751 | 29,519 | 7,343 | 1,087 | 106,251 |

| Total Contingent Risk | 39,077 | 31,427 | 20,971 | 32,680 | 13,099 | 2,738 | 139,993 |

| Total Risks in Financial Instruments | 288,824 | 114,587 | 105,406 | 102,313 | 81,443 | 14,696 | 707,268 |

Download Excel

| Risks by Geographical Areas December 2013 |

Millions of euros | ||||||

|---|---|---|---|---|---|---|---|

| Spain | Europe, Excluding Spain | Mexico | USA | South America | Rest | Total | |

| Financial assets - |

|

|

|

|

|

|

|

| Financial assets held for trading | 14,882 | 33,091 | 15,707 | 2,677 | 3,412 | 2,345 | 72,114 |

| Loans and advances to customers | - | - | - | 107 | - | - | 107 |

| Debt securities | 6,320 | 5,838 | 13,410 | 424 | 2,608 | 1,002 | 29,602 |

| Equity instruments (*) | 2,752 | 953 | 632 | 118 | 148 | 163 | 4,766 |

| Derivatives | 5,810 | 26,300 | 1,665 | 2,028 | 656 | 1,180 | 37,639 |

| Other financial assets designated at fair value through profit or loss | 211 | 106 | 1,591 | 503 | 2 | - | 2,413 |

| Loans and advances to credit institutions | - | - | - | - | - | - | - |

| Debt securities | 107 | 54 | 5 | 497 | - | - | 663 |

| Equity instruments (*) | 104 | 52 | 1,586 | 6 | 2 | - | 1,750 |

| Available-for-sale portfolio | 42,074 | 8,587 | 10,380 | 7,729 | 5,626 | 3,011 | 77,407 |

| Debt securities | 38,732 | 8,453 | 10,329 | 7,247 | 5,535 | 1,143 | 71,439 |

| Equity instruments (*) | 3,342 | 134 | 51 | 482 | 91 | 1,868 | 5,968 |

| Loans and receivables | 194,383 | 26,712 | 44,414 | 39,650 | 53,886 | 4,984 | 364,031 |

| Loans and advances to credit institutions | 5,224 | 9,171 | 2,366 | 2,707 | 1,909 | 1,415 | 22,792 |

| Loans and advances to customers | 187,400 | 17,519 | 42,048 | 36,047 | 50,173 | 3,569 | 336,759 |

| Debt securities | 1,759 | 22 | - | 896 | 1,804 | - | 4,481 |

| Held-to-maturity investments | - | - | - | - | - | - | - |

| Hedging derivatives and macrohedging adjustments | 434 | 2,113 | 8 | 60 | 10 | 4 | 2,629 |

| Total Risk in Financial Assets | 251,984 | 70,609 | 72,100 | 50,618 | 62,935 | 10,344 | 518,591 |

| Contingent risks and liabilities |

|

|

|

|

|

|

|

| Contingent risks | 15,172 | 9,038 | 767 | 2,344 | 5,292 | 929 | 33,542 |

| Contingent liabilities | 28,096 | 17,675 | 16,109 | 24,485 | 7,002 | 803 | 94,170 |

| Total Contingent Risk | 43,268 | 26,713 | 16,876 | 26,829 | 12,294 | 1,732 | 127,712 |

| Total Risks in Financial Instruments | 295,252 | 97,322 | 88,976 | 77,447 | 75,229 | 12,076 | 646,303 |

The breakdown of the main figures in the most significant foreign currencies in the accompanying consolidated balance sheets is set forth in Appendix VII.

Sovereign risk concentration

Sovereign risk management

The risk associated with the transactions involving sovereign risk is identified, measured, controlled and tracked by a centralized unit integrated in the BBVA Group’s Risk Area. Its basic functions involve the preparation of reports in the countries where sovereign risk exists (called “financial programs”), tracking such risks, assigning ratings to these countries and, in general, supporting the Group in terms of reporting requirements for any transactions involving sovereign risk. The risk policies established in the financial programs are approved by the relevant risk committees.

The country risk unit tracks the evolution of the risks associated with the various countries to which the Group are exposed (including sovereign risk) on an ongoing basis in order to adapt its risk and mitigation policies to any macroeconomic and political changes that may occur. Moreover, it regularly updates its internal ratings and forecasts for these countries. The internal rating assignment methodology is based on the assessment of quantitative and qualitative parameters which are in line with those used by certain multilateral organizations such as the International Monetary Fund (IMF) and the World Bank (WB), rating agencies and export credit organizations.

Sovereign risk exposure

The table below provides a breakdown of exposure to financial assets (excluding derivatives and equity instruments), as of December 31, 2015, 2014 and 2013 by type of counterparty and the country of residence of such counterparty. The below figures do not take into account valuation adjustments, impairment losses or loan-loss provisions:

Download Excel

|

|

Millions of euros | ||||

|---|---|---|---|---|---|

|

|

December 2015 | ||||

| Risk Exposure by Countries | Sovereign Risk (*) |

Financial Institutions | Other Sectors | Total | % |

| Spain | 74,020 | 7,323 | 177,348 | 258,690 | 42.8% |

| Turkey | 12,037 | 3,374 | 54,161 | 69,572 | 11.5% |

| Italy | 10,694 | 724 | 1,858 | 13,276 | 2.2% |

| France | 1,029 | 5,796 | 3,025 | 9,850 | 1.6% |

| Portugal | 704 | 19 | 4,711 | 5,433 | 0.9% |

| Germany | 560 | 1,473 | 1,588 | 3,621 | 0.6% |

| United Kingdom | 4 | 7,466 | 6,547 | 14,017 | 2.3% |

| Ireland | 1 | 96 | 934 | 1,031 | 0.2% |

| Greece | - | 0 | 57 | 57 | 0.0% |

| Rest of Europe | 1,278 | 2,668 | 8,769 | 12,715 | 2.1% |

| Subtotal Europe | 100,327 | 28,938 | 258,998 | 388,262 | 64.2% |

| Mexico | 22,192 | 5,676 | 46,438 | 74,306 | 12.3% |

| The United States | 11,378 | 3,834 | 61,738 | 76,950 | 12.7% |

| Venezuela | 152 | 146 | 845 | 1,144 | 0.2% |

| Rest of countries | 3,711 | 4,470 | 55,717 | 63,897 | 10.6% |

| Total Rest of Countries | 37,433 | 14,126 | 164,738 | 216,297 | 35.8% |

| Total Exposure to Financial Instruments | 137,760 | 43,064 | 423,735 | 604,559 | 100.0% |

Download Excel

|

|

Millions of euros | ||||

|---|---|---|---|---|---|

|

|

December 2014 | ||||

| Risk Exposure by Countries | Sovereign Risk (*) |

Financial Institutions | Other Sectors | Total | % |

| Spain | 68,584 | 9,040 | 157,337 | 234,961 | 46.5% |

| Italy | 9,823 | 713 | 2,131 | 12,667 | 2.5% |

| France | 1,078 | 5,351 | 2,453 | 8,883 | 1.8% |

| United Kingdom | 119 | 2,923 | 4,669 | 7,711 | 1.5% |

| Portugal | 605 | 43 | 4,927 | 5,574 | 1.1% |

| Germany | 590 | 1,129 | 1,565 | 3,284 | 0.6% |

| Ireland | 167 | 148 | 565 | 880 | 0.2% |

| Turkey | 21 | 214 | 246 | 482 | 0.1% |

| Greece | - | - | 64 | 64 | 0.0% |

| Rest of Europe | 1,182 | 6,011 | 4,800 | 11,993 | 2.4% |

| Subtotal Europa | 82,170 | 25,573 | 178,757 | 286,499 | 56.7% |

| Mexico | 31,164 | 2,757 | 42,864 | 76,785 | 15.2% |

| The United States | 11,241 | 3,941 | 52,849 | 68,031 | 13.5% |

| Rest of countries | 7,676 | 4,669 | 62,052 | 74,398 | 14.7% |

| Total Rest of Countries | 50,081 | 11,367 | 157,765 | 219,213 | 43.3% |

| Total Exposure to Financial Instruments | 132,251 | 36,939 | 336,522 | 505,713 | 100.0% |

Download Excel

|

|

Millions of euros | ||||

|---|---|---|---|---|---|

|

|

December 2013 | ||||

| Risk Exposure by Countries | Sovereign Risk (*) |

Financial Institutions | Other Sectors | Total | % |

| Spain | 59,114 | 11,870 | 166,677 | 237,661 | 51.1% |

| United Kingdom | 3 | 5,405 | 4,377 | 9,785 | 2.1% |

| Italy | 3,888 | 422 | 2,617 | 6,927 | 1.5% |

| France | 942 | 2,640 | 2,316 | 5,898 | 1.3% |

| Portugal | 385 | 238 | 5,179 | 5,802 | 1.2% |

| Germany | 1,081 | 1,338 | 1,206 | 3,625 | 0.8% |

| Ireland | - | 221 | 487 | 708 | 0.2% |

| Turkey | 10 | 65 | 163 | 238 | 0.1% |

| Greece | - | - | 72 | 72 | 0.0% |

| Rest of Europe | 2,608 | 2,552 | 4,239 | 9,399 | 2.0% |

| Subtotal Europa | 68,031 | 24,751 | 187,333 | 280,115 | 60.2% |

| Mexico | 26,629 | 2,810 | 38,312 | 67,751 | 14.6% |

| The United States | 5,224 | 3,203 | 41,872 | 50,299 | 10.8% |

| Rest of countries | 7,790 | 5,480 | 53,649 | 66,919 | 14.4% |

| Total Rest of Countries | 39,643 | 11,493 | 133,833 | 184,969 | 39.8% |

| Total Exposure to Financial Instruments | 107,674 | 36,244 | 321,166 | 465,084 | 100.0% |

The exposure to sovereign risk set out in the above tables includes positions held in government debt securities in countries where the Group operates. They are used for ALCO’s management of the interest-rate risk on the balance sheets of the Group’s entities in these countries, as well as for hedging of pension and insurance commitments by insurance entities within the BBVA Group.

For additional information on sovereign risk in Europe see Appendix XII

Valuation and impairment methods

The valuation methods used to assess the instruments that are subject to sovereign risks are the same ones used for other instruments included in the relevant portfolios and are detailed in Note 8. Specifically, the fair value of sovereign debt securities of European countries has been considered equivalent to their listed price in active markets (Level 1 as defined in Note 8).

Risk related to the developer and Real-Estate sector in Spain

One of the main Group activities of the Group in Spain is focused on developer and mortgage loans. The policies and strategies established by the Group to deal with risks related to the developer and real-estate sector are explained below:

Policies and strategies established by the Group to deal with risks related to the developer and real-estate sector

BBVA has teams specializing in the management of the Real-Estate Sector risk, given its economic importance and specific technical component. This specialization is not only in the Risk-Acceptance teams, but throughout the handling, commercial, problem risks and legal, etc. It also includes the research department of the BBVA Group (BBVA Research), which helps determine the medium/long-term vision needed to manage this portfolio. Specialization has been increased and the management teams in the areas of recovery and the Real Estate Unit itself have been reinforced.

The policies established to address the risks related to the developer and real-estate sector, aim to accomplish, among others, the following objectives: to avoid concentration in terms of customers, products and regions; to estimate the risk profile for the portfolio; and to anticipate possible worsening of the portfolio.

Specific policies for analysis and admission of new developer risk transactions

In the analysis of new operations, the assessment of the commercial operation in terms of the economic and financial viability of the project has been one of the constant points that have helped ensure the success and transformation of construction land operations for customers’ developments.

With regard the participation of the Risk Acceptance teams, they have a direct link and participate in the committees of areas such as Recoveries and the Real Estate Unit. This guarantees coordination and exchange of information in all the processes.

The following strategies have been implemented with customers in the developer sector: avoidance of large corporate transactions, which had already reduced their share in the years of greatest market growth; non active participation in the second-home market; commitment to public housing financing; and participation in land operations with a high level of urban development security, giving priority to land open to urban development.

Risk monitoring policies

The base information for analyzing the real estate portfolios is updated monthly. The tools used include the so-called “watch-list”, which is updated monthly with the progress of each client under watch, and the different strategic plans for management of special groups. There are plans that involve an intensification of the review of the portfolio for financing land, while, in the case of ongoing promotions, they are classified based on the rate of progress of the projects.

These actions have enabled BBVA to identify possible impairment situations, by always keeping an eye on BBVA’s position with each customer (whether or not as first creditor). In this regard, key aspects include management of the risk policy to be followed with each customer, contract review, deadline extension, improved collateral, rate review (repricing) and asset purchase.

Proper management of the relationship with each customer requires knowledge of various aspects such as the identification of the source of payment difficulties, an analysis of the company’s future viability, the updating of the information on the debtor and the guarantors (their current situation and business course, economic-financial information, debt analysis and generation of funds), and the updating of the appraisal of the assets offered as collateral.

BBVA has a classification of debtors in accordance with legislation in force in each country, usually categorizing each one’s level of difficulty for each risk.

Based on the information above, a decision is made whether to use the refinancing tool, whose objective is to adjust the structure of the maturity of the debt to the generation of funds and the customer’s payment capacity.

As for the policies relating to risk refinancing with the developer and real-estate sector, they are the same as the general policies used for all of the Group’s risks (see Note 7.3.9). In the developer and real estate sector, they are based on clear solvency and viability criteria for projects, with demanding terms for additional guarantees and legal compliance, given a refinancing tool that standardizes criteria and variables when considering any refinancing operation.

In the case of refinancing, the tools used for enhancing the Bank’s position are: the search for new intervening parties with proven solvency and initial payment to reduce the principal debt or outstanding interest; the improvement of the debt bond in order to facilitate the procedure in the event of default; the provision of new or additional collateral; and making refinancing viable with new conditions (period, rate and repayments), adapted to a credible and sufficiently verified business plan.

Policies applied in the management of real estate assets in Spain

The policy applied for managing these assets depends on the type of real-estate asset, as detailed below.

In the case of completed homes, the final aim is the sale of these homes to private individuals, thus diluting the risk and beginning a new business cycle. Here, the strategy has been to help subrogation (the default rate in this channel of business is notably lower than in any other channel of residential mortgages) and to support customers’ sales directly, using BBVA’s own channel (BBVA Services and our branches), creating incentives for sale and including sale orders for BBVA. In exceptional case we have even accepted partial haircuts, with the aim of making the sale easier.

In the case of ongoing construction work, the strategy has been to help and promote the completion of the works in order to transfer the investment to completed homes. The whole developer Works in Progress portfolio has been reviewed and classified into different stages with the aim of using different tools to support the strategy. This includes the use of developer accounts-payable financing as a form of payment control, the use of project monitoring supported by the Real Estate Unit itself, and the management of direct suppliers for the works as a complement to the developer’s own management.

With respect to land, the fact that the vast majority of the risk is urban land simplifies the management. Urban management and liquidity control to tackle urban planning costs are also subject to special monitoring.

For quantitative information about the risk related to the developer and Real-Estate sector in Spain see Appendix XIII.

7.3.5 Credit quality of financial assets that are neither past due nor impaired

The BBVA Group has tools (“scoring” and “rating”) that enable it to rank the credit quality of its operations and customers based on an assessment and its correspondence with the probability of default (“PD”) scales. To analyze the performance of PD, the Group has a series of tracking tools and historical databases that collect the pertinent internally generated information, which can basically be grouped together into scoring and rating models.

Scoring

Scoring is a decision-making model that contributes to both the arrangement and management of retail loans: consumer loans, mortgages, credit cards for individuals, etc. Scoring is the tool used to decide to originate a loan, what amount should be originated and what strategies can help establish the price, because it is an algorithm that sorts transactions by their credit quality. This algorithm enables the BBVA Group to assign a score to each transaction requested by a customer, on the basis of a series of objective characteristics that have statistically been shown to discriminate between the quality and risk of this type of transactions. The advantage of scoring lies in its simplicity and homogeneity: all that is needed is a series of objective data for each customer, and this data is analyzed automatically using an algorithm.

There are three types of scoring, based on the information used and on its purpose:

- Reactive scoring: measures the risk of a transaction requested by an individual using variables relating to the requested transaction and to the customer’s socio-economic data available at the time of the request. The new transaction is approved or rejected depending on the score.

- Behavioral scoring: scores transactions for a given product in an outstanding risk portfolio of the entity, enabling the credit rating to be tracked and the customer’s needs to be anticipated. It uses transaction and customer variables available internally. Specifically, variables that refer to the behavior of both the product and the customer.

- Proactive scoring: gives a score at customer level using variables related to the individual’s general behavior with the entity, and to his/her payment behavior in all the contracted products. The purpose is to track the customer’s credit quality and it is used to pre-grant new transactions.

Rating

Rating tools, as opposed to scoring tools, do not assess transactions but focus on the rating of customers instead: companies, corporations, SMEs, public authorities, etc. A rating tool is an instrument that, based on a detailed financial study, helps determine a customer’s ability to meet his/her financial obligations. The final rating is usually a combination of various factors: on one hand, quantitative factors, and on the other hand, qualitative factors. It is a middle road between an individual analysis and a statistical analysis.

The main difference between ratings and scorings is that the latter are used to assess retail products, while ratings use a wholesale banking customer approach. Moreover, scorings only include objective variables, while ratings add qualitative information. And although both are based on statistical studies, adding a business view, rating tools give more weight to the business criterion compared to scoring tools.

For portfolios where the number of defaults is very low (sovereign risk, corporates, financial entities, etc.) the internal information is supplemented by “benchmarking” of the external rating agencies (Moody’s, Standard & Poor’s and Fitch). To this end, each year the PDs compiled by the rating agencies at each level of risk rating are compared, and the measurements compiled by the various agencies are mapped against those of the BBVA master rating scale.

Once the probability of default of a transaction or customer has been calculated, a "business cycle adjustment" is carried out. This is a means of establishing a measure of risk that goes beyond the time of its calculation. The aim is to capture representative information of the behavior of portfolios over a complete economic cycle. This probability is linked to the Master Rating Scale prepared by the BBVA Group to enable uniform classification of the Group’s various asset risk portfolios.

The table below shows the abridged scale used to classify the BBVA Group’s outstanding risk as of December 31, 2015:

Download Excel

|

|

|

Probability of default (basic points) |

||

|---|---|---|---|---|

| External rating Standard&Poor's List |

Internal rating Reduced List (22 groups) |

Average | Minimum from >= | Maximum |

| AAA | AAA | 1 | - | 2 |

| AA+ | AA+ | 2 | 2 | 3 |

| AA | AA | 3 | 3 | 4 |

| AA- | AA- | 4 | 4 | 5 |

| A+ | A+ | 5 | 5 | 6 |

| A | A | 8 | 6 | 9 |

| A- | A- | 10 | 9 | 11 |

| BBB+ | BBB+ | 14 | 11 | 17 |

| BBB | BBB | 20 | 17 | 24 |

| BBB- | BBB- | 31 | 24 | 39 |

| BB+ | BB+ | 51 | 39 | 67 |

| BB | BB | 88 | 67 | 116 |

| BB- | BB- | 150 | 116 | 194 |

| B+ | B+ | 255 | 194 | 335 |

| B | B | 441 | 335 | 581 |

| B- | B- | 785 | 581 | 1,061 |

| CCC+ | CCC+ | 1,191 | 1,061 | 1,336 |

| CCC | CCC | 1,500 | 1,336 | 1,684 |

| CCC- | CCC- | 1,890 | 1,684 | 2,121 |

| CC+ | CC+ | 2,381 | 2,121 | 2,673 |

| CC | CC | 3,000 | 2,673 | 3,367 |

| CC- | CC- | 3,780 | 3,367 | 4,243 |

These different levels and their probability of default were calculated by using as a reference the rating scales and default rates provided by the external agencies Standard & Poor’s and Moody’s. These calculations establish the levels of probability of default for the BBVA Group’s Master Rating Scale. Although this scale is common to the entire Group, the calibrations (mapping scores to PD sections/Master Rating Scale levels) are carried out at tool level for each country in which the Group has tools available.

The table below outlines the distribution of exposure, including derivatives, by internal ratings, to corporates, financial entities and institutions (excluding sovereign risk), of the main BBVA Group entities (excluding Catalunya Banc) as of December 31, 2015 and 2014:

Download Excel

|

|

December 2015 | December 2014 | ||

|---|---|---|---|---|

| Credit Risk Distribution by Internal Rating |

Amount (Millions of Euros) |

% | Amount (Millions of Euros) |

% |

| AAA/AA+/AA/AA- | 27,387 | 10.97% | 30,306 | 11.49% |

| A+/A/A- | 59,194 | 23.71% | 70,850 | 26.86% |

| BBB+ | 40,059 | 16.04% | 37,515 | 14.22% |

| BBB | 22,517 | 9.02% | 24,213 | 9.18% |

| BBB- | 31,996 | 12.81% | 33,129 | 12.56% |

| BB+ | 19,425 | 7.78% | 22,595 | 8.57% |

| BB | 12,785 | 5.12% | 11,136 | 4.22% |

| BB- | 6,326 | 2.53% | 6,364 | 2.41% |

| B+ | 6,050 | 2.42% | 7,475 | 2.83% |

| B | 4,080 | 1.63% | 4,966 | 1.88% |

| B- | 3,047 | 1.22% | 3,876 | 1.47% |

| CCC/CC | 16,827 | 6.74% | 11,362 | 4.31% |

| Total | 249,693 | 100.00% | 263,786 | 100.00% |

7.3.6 Past due but not impaired Risks

The table below provides details by counterpart and by product of past due risks as of December 31, 2015, 2014 and 2013 but not considered to be impaired, listed by their first past-due date:

Download Excel

|

|

Millions of euros | ||

|---|---|---|---|

| Financial Assets Past Due but Not Impaired by counterpart December 2015 | Less than 1 Month Past-Due |

1 to 2 Months Past-Due |

2 to 3 Months Past-Due |

| Loans and advances | 3,445 | 825 | 404 |

| Central banks | - | - | - |

| General Governments | 154 | 278 | 2 |

| Credit institutions and other financial corporations | 7 | 1 | 14 |

| Non-financial corporations | 838 | 148 | 48 |

| Households | 2,446 | 399 | 340 |

| Debt securities | - | - | - |

| Total | 3,445 | 825 | 404 |

Download Excel

| Financial Assets Past Due but Not Impaired by counterpart December 2014 | Millions of euros | ||

|---|---|---|---|

| Less than 1 Month Past-Due |

1 to 2 Months Past-Due |

2 to 3 Months Past-Due |

|

| Loans and advances | 3,286 | 794 | 657 |

| Central banks | - | - | - |

| General Governments | 33 | 1 | 53 |

| Credit institutions and other financial corporations | 6 | - | 17 |

| Non-financial corporations | 849 | 347 | 136 |

| Households | 2,398 | 446 | 451 |

| Debt securities | - | - | - |

| Total | 3,286 | 794 | 657 |

Download Excel

| Financial Assets Past Due but Not Impaired by counterpart December 2013 | Millions of euros | ||

|---|---|---|---|

| Less than 1 Month Past-Due |

1 to 2 Months Past-Due |

2 to 3 Months Past-Due |

|

| Loans and advances | 3,005 | 336 | 220 |