The credit risk assessment in OTC financial instruments is made by means of a Monte Carlo simulation, which calculates not only the current exposure of the counterparties, but also their possible future exposure to fluctuations in market variables.

The model combines different credit risk factors to produce distributions of future credit losses and thus allows a calculation of the portfolio effect; in other words, it incorporates the term effect (the exposure of the various transactions presents potential maximum values at different points in time) and the correlation effect (the relation between exposures, risk factors, etc. are normally different to 1). It also uses credit risk mitigation techniques such as legal netting and collateral agreements.

The equivalent maximum credit risk exposure to counterparties in the Group as of December 31, 2010 stood at €44,762m, a 4.5% increase on year-end 2009. The equivalent maximum credit risk exposure in BBVA, S.A. is estimated at €39,103m. The overall reduction in terms of exposure due to netting and collateral agreements was €27,443m.

The net market value of the instruments mentioned in the BBVA, S.A. portfolio on December 31, 2010 was €1,674m and the gross positive market value of the contracts was €38,661m.

The second accompanying table shows the distribution by maturity of the equivalent maximum exposure amounts in OTC financial instruments.

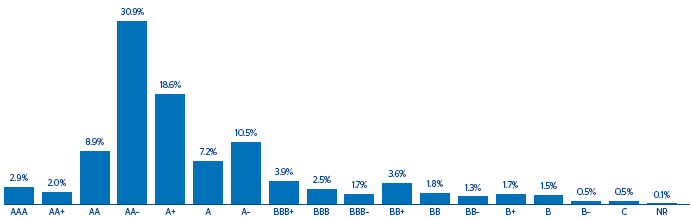

The counterparty risk assumed in this activity involved entities with a high credit rating (equal to or above A– in 81% of cases). Exposure is concentrated in financial entities (82%), and the remaining 18% in corporations and customers is suitably diversified.

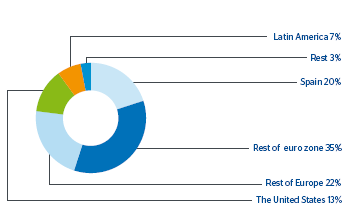

By geographical area, the highest exposure of BBVA, S.A. was in Europe (77%) and North America (13%), which together accounted for 91% of the total.