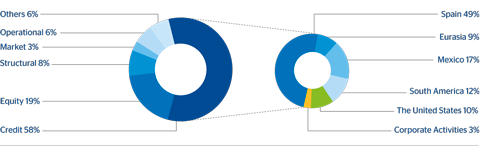

Attributable economic risk capital (ERC) consumption reached €36,062m as of December 31, 2012, an increase of 29.4% over 2011 figures, using comparable data(1). The main risk continues to be credit risk on portfolios originated in the Group branch networks from its own customer base. This accounted for 58.3% of the total with a year-on-year increase of 15.8%, due mainly to the incorporation of Unnim, the increased credit risk on the trading floors of the Assets and Liabilities Committee (ALCO) and the recalibration of parameters carried out in Spain. The ERC for equity reaches a relative weight of 19.4%, up 126.5%, as the calculation of the goodwill generated by stakes in the credit institutions making up the Group has been included in its estimate. Structural interest-rate and exchange-rate ERC is up 58.7%, due to the impact of the inclusion of the goodwill on the foreign-exchange risk. The relative weight of ERC from market operations increases after posting a 78.4% increase due to the incorporation of the elements of Basel 2.5 (stress VaR and IRC).

3 BBVA Group’s economic risk capital Distribution by type of risk

(Data in attributable terms 31-12-2012)

In the breakdown by area, Spain registers an ERC increase of 14.7% due to the incorporation of Unnim, the recalibration of the models included in mid-year, the increased credit risk on the trading floors of the ALCO and the increased market risk resulting from the application of Basel 2.5. Eurasia grows 8.5% over the previous year due to the trend in the credit risk parameters in Turkey and the increase in the value of the stake in China Citic Bank (CNCB), which increases equity risk. In Mexico, ERC is up 13.8%, due mainly, as regards credit risk, to the recalibration of the parameters and lending growth. As for market risk, ERC in Mexico is up due to the application of the Basel 2.5 criteria. United States reduces its relative weight in global ERC, which is down 10.2% year-on-year due to the improved credit risk profile in the area. ERC in South America grows 12.5%, basically as a result of the general and strong lending growth in all the countries and the appreciation of the currencies in the region.

4 BBVA Group’s economic risk capital. Distribution by business area

(Data in attributable terms 31-12-2012)

In conclusion, the Group’s recurrent risk-adjusted return (RAR), i.e., that generated from customer business and excluding one-offs, stood at 18.9%, remaining at high levels in all business areas.

(1) The growth rates presented are calculated against the close as of the same time in December 2011 (€27,874m),which includes the annual effects of the updates carried out at the end of the year (Mexico, South America and

The United States) in the credit risk parameters and the revision of other risk models, as compared to the official figure

for 2012 (€36,062m).